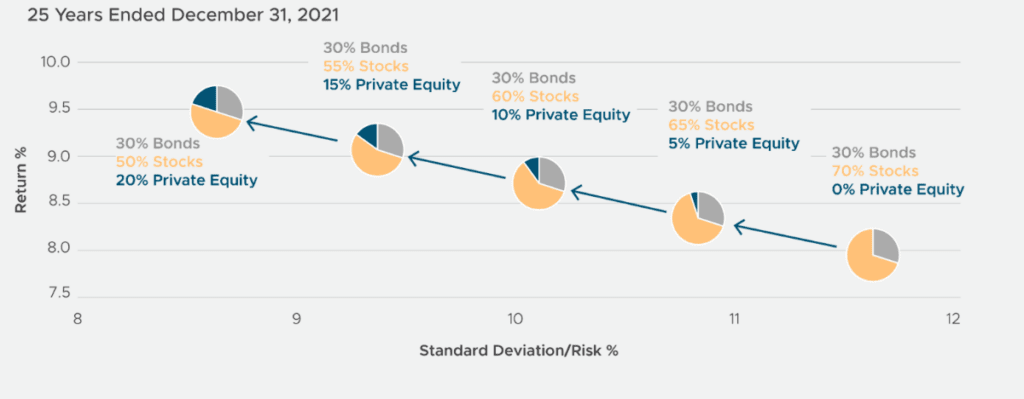

Portfolios with higher allocations to private investments outperform

Private market investing may offer benefits like an enhanced risk-return profile and further diversification for certain investors. Private markets represent a huge part of the overall market, as currently 87% of U.S. companies with greater than $100 million in revenue are private.(1) Noted in the chart, portfolios with increased private equity allocations have outperformed their lesser weighted counterparts over the last 25 years with better performance for lower risk. This can be attributed to several factors, including U.S. growth companies staying private for longer, the illiquidity premium that rewards investors for locking up their capital for long stretches, and the potential for structured investments to protect the downside and/or enhance the investor’s upside, among other reasons. In addition, as private market investments are not marked to market every day, they historically deliver a smoother performance across longer periods of time than public equities, especially during times of high volatility or during recessions.(1)

Portfolio Returns (25-years ended December 2021)

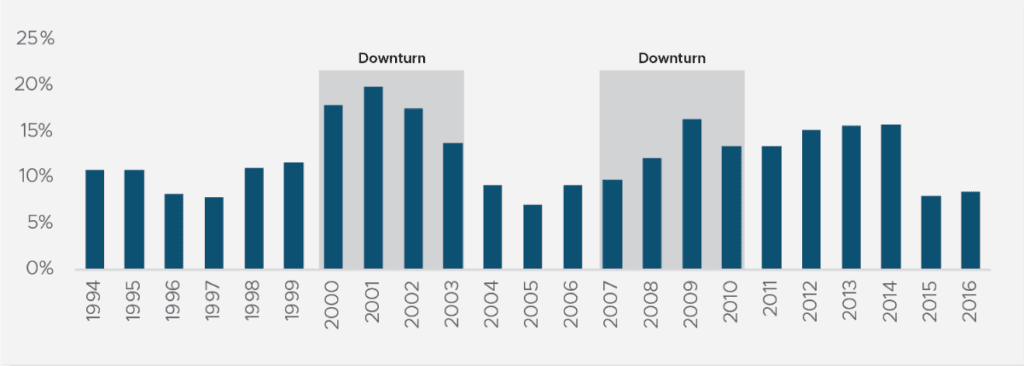

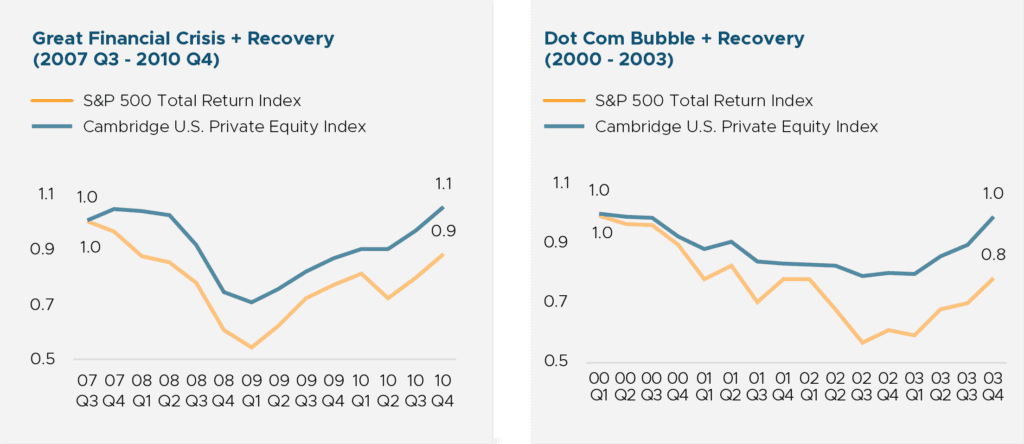

Why invest in private investments during times of high volatility and distress?

Historically, some of private equity’s strongest vintages have occured during downturns. Through periods of economic uncertainty, private fund managers’ focus on long-term value creation could be a major advantage and investor terms can be significantly more advantageous. One of the most overlooked factors in how private fund managers create value is their ability to control the optimal time to enter and exit. Experienced fund managers exit portfolio companies when they can command an attractive return, avoiding the “panic selling” that can happen in the public markets. Furthermore, diversification parameters set by fund managers with operational prowess can potentially lower the risk of catastrophic loss to an investor, providing lower volatility, but preserving the potential for higher returns. As shown, during the Dot-Com Bubble and the Great Financial Crisis, private equity provided a higher trough and a quicker recovery.

Some of PE’s Strongest Vintages Began Investing During Downturns

Sophisticated investors are increasing their allocations to private markets

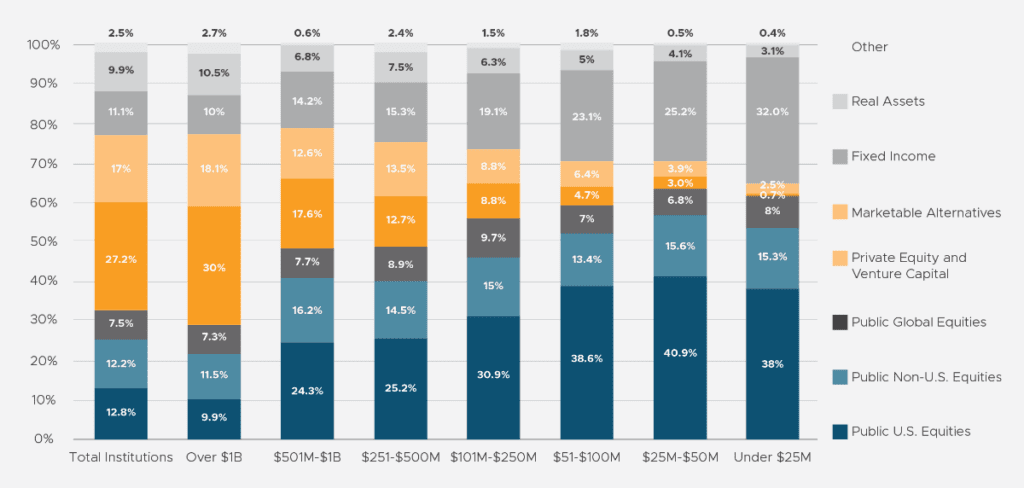

Funding in private markets revolves around institutional investors, such as pensions, endowments, insurance companies, and increasingly, family offices. Typically, the larger the institution, the higher allocation to private markets. In 2021, private markets fundraising reached a new high, eclipsing $1 trillion for the 4th time in the last 5 years, per McKinsey & Company. Single and multi-family offices now have from ~40-60% allocation in private markets.(2) Relative to the current debt markets specifically, rising interest rates have enabled private credit funds to generate significant yield on senior secured credit facilities, providing investors with the potential for stable, lower credit-risk income.

Asset Allocations for Endowment Cohorts, FY2021

Cresset is democratizing access to private markets

Traditionally, institutional-quality private market investments have been hard to access and require high investment minimums. At Cresset, we have democratized access to institutional-quality private investments that have historically been available only to institutional investors and the wealthiest of families. Cresset believes that alpha is found in the significant, long-term value creation of private investments across all asset classes. As such, Cresset has investment vehicles in private equity, private credit, venture capital, and real estate. Investors may even access some of these investments through an evergreen fund structure, offering potential private market returns with enhanced liquidity features. Cresset was founded by entrepreneurs Eric Becker and Avy Stein, who spent decades as private equity investors, during which they started, nurtured, and backed more than 150 businesses and raised more than $8 billion in funding. Few firms today have the depth and breadth of funds and direct investing capabilities that Cresset offers. We have invested significantly in building out a private investments infrastructure that enables our client families to invest like the largest single-family offices and endowments.

Disclosures

Cresset refers to Cresset Capital Management, LLC and all of its subsidiaries and affiliates. Cresset Asset Management, LLC provides investment advisory, family office, and other services to individuals, families, and institutional clients. Cresset Partners, LLC provides investment advisory services strictly to investment vehicles investing in private equity, real estate and other investment opportunities. Cresset Asset Management, LLC and Cresset Partners, LLC are SEC registered investment advisers.

The information contained in this presentation is not intended to provide professional, investment, legal or tax advice and should not be relied upon in that regard. The contents of this presentation are for general information only and are not provided with regard to your specific investment objectives, financial situation, tax exposure or particular needs. The contents hereof are not a recommendation of, or solicitation for, the subscription, purchase, or sale of any security. Nothing contained herein should be used as the basis for making any specific investment, business, or commercial decision. You should read the final confidential offering circular, limited liability company agreement and/or other supplemental and controlling documents before making an investment decision regarding any particular security carefully before investing in any security.

Investments, including interests in real estate and private equity funds, are subject to investment, tax, regulatory, market, macro-economic and other risks, including loss of the principal amount invested. Past performance as well as any projection or forecast used or discussed in this presentation are not indicative of future or likely performance of any investment product. Statements may be forward looking and are not intended as specific investment advice or guarantees of future performance. Such forward-looking statements necessarily involve known and unknown risks and uncertainties, which may cause actual performance and financial results in future periods to differ materially from any projections of future performance or result expressed or implied by such statements.

The contents of this presentation are subject to change and may be modified, deleted, or replaced at any time in Sponsor’s sole discretion. In particular, Sponsor assumes no responsibility for, nor make any representations, endorsements, or warranties whatsoever in relation to the timeliness, accuracy and completeness of any content contained in the presentation. While care has been taken in preparing the contents of this presentation, such contents are provided to you “as is” and “as available” without warranty of any kind either express or implied. In particular, no warranty regarding suitability, accuracy, or fitness for a particular purpose is given in conjunction with such contents. Sponsor shall not be liable for any loss, damage, costs, charges and/or expenses incurred as a result of or in connection with this presentation or any reliance on the contents of this presentation.

The provision of any services or products provided by Sponsor and/or its affiliates shall be expressly subject to the particular terms and conditions as contained in a separate written agreement between you and Sponsor and/or its affiliate as applicable. Sponsor will not provide any individualized advice or consulting unless agreed to by a separate written agreement.

The Cambridge Associates Private Equity Index is created from quarterly data as supplied by managers that may be unaudited. The indices are not transparent and cannot be independently verified and may be recalculated by Cambridge each time a new fund is added. The historical performance of the index is not fixed, cannot be replicated and will differ over time from the data presented in this communication. The funds included in the private capital data shown report their performance voluntarily and therefore the data may reflect a bias towards funds with track records of success. The underlying funds may report audited or unaudited data. The data is not transparent and cannot be independently verified.

Sources

(1) Private Equity Offers Resilience in a Downturn, by Nick Veronis and Tatiana Esipovich Link to Document

(2) Increasing Allocation to Private Markets, Investcorp (J#une 2021) Link to Document

Chart 1 – Source: Neuberger Berman FactSet as of December 31, 2021. Bonds represented by the Barclays U.S. Aggregate Index, stocks represented by the S&P 500, private equity represented by the Cambridge Associates Private Equity Index. Past performance is not indicative of future results. Indices are not available for direct investment. Please refer to the endnotes for certain important information on indices and risks of private equity investing.

Chart 2 – Source: Private Equity Offers Resilience in a Downturn, by Nick Veronis and Tatiana Esipovich Link to Document

Chart 3 (both Dot Com and Great Financial Crisis) – Gridline, Factset and Pitchbook

Chart 4 – 2021 NACUBO-TIAA Study of Endowments