Key Observations

- Artificial intelligence (AI) infrastructure is driving one of the largest corporate debt cycles in modern history.

- Investment-grade issuance remains heavily oversubscribed despite record supply.

- Private credit is increasingly underwriting AI growth based on projected revenue streams rather than hard assets.

- Credit spreads are historically tight, masking rising leverage risk.

- A widening gap between AI capex and realized revenue creates monetization uncertainty.

- Off-balance-sheet and structured financing add opacity and potential systemic risk.

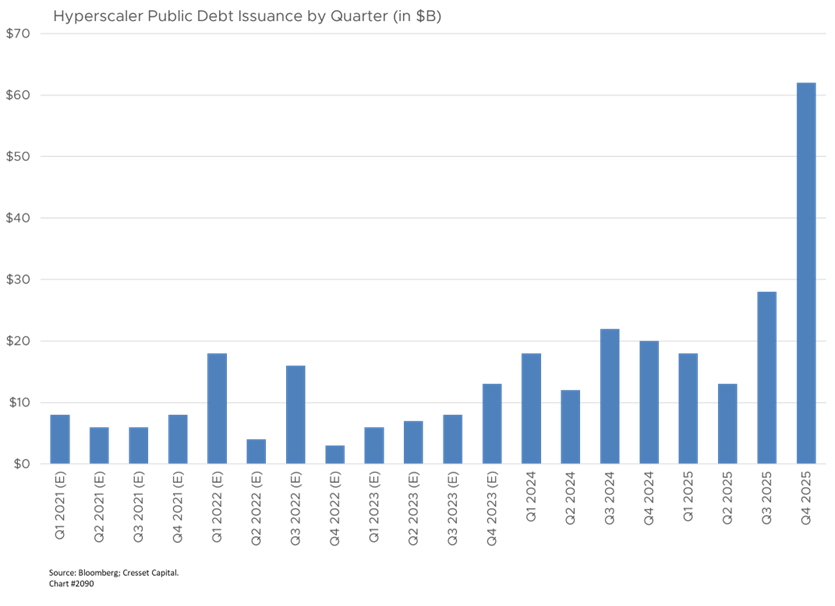

The buildout of artificial intelligence (AI) infrastructure is generating one of the most significant debt issuance cycles in modern capital markets history. Technology-sector bond issuance surpassed $200 billion in 2025, with year-to-date supply already exceeding $67 billion through early 2026. AI-related investment-grade debt alone accounted for roughly $200 billion in 2025, a figure analysts project will double this year. JPMorgan estimates that companies competing in the AI arms race may need to raise as much as $1.5 trillion in investment-grade bonds over the next five years, with cumulative global AI-related capital investment potentially reaching $3.5 trillion between 2026 and 2029. This shift in how corporate America is financing its future has not been seen in the United States since the railroads.

Mega Deals and Market Appetite Signal Intensity

The scale of individual deals underscores just how capital-intensive this buildout has become. Alphabet raised approximately $32 billion across global bond offerings in less than 24 hours to finance AI infrastructure, including a rare 100-year sterling bond that yielded 6.05% and was nearly ten times oversubscribed. Oracle issued $18 billion in bonds in September 2025, nearly five times oversubscribed, to fund its AI data center expansion. Meta took a different approach, utilizing off-balance sheet structures, including a $27.3 billion transaction, to fund data center investments without immediately impacting its credit ratings. Meanwhile, convertible bond markets are seeing record activity: total U.S. convertible volume reached $120 billion in 2025, with AI-linked companies raising $13.6 billion through mid-February 2026 alone, a whopping 556% increase over the same period a year prior.

Private Credit Joins the AI Financing Boom

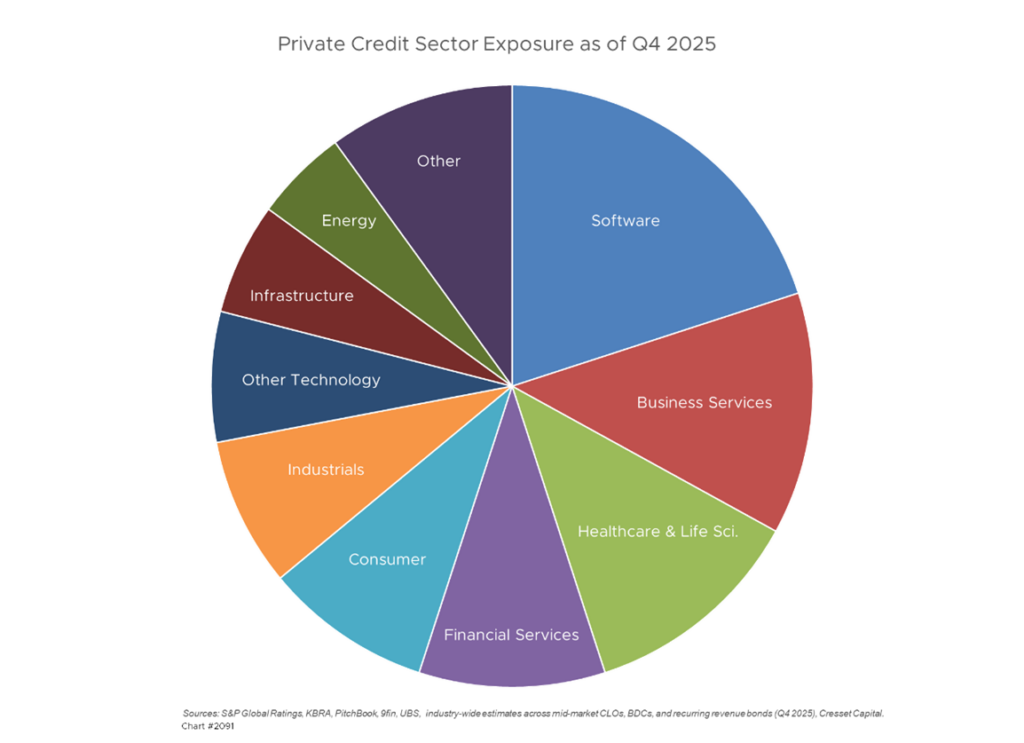

The AI financing wave has extended well beyond investment-grade bond markets into private credit. Software companies, historically light on hard assets, are increasingly accessing private lending markets to fund AI-related development, cloud infrastructure, and competitive positioning. Lenders are showing an appetite for these deals, attracted by floating-rate structures and the perceived growth premium embedded in AI-adjacent software businesses.

This represents a meaningful evolution in private credit underwriting, as deals are being written against future recurring revenue streams and AI monetization potential rather than traditional asset collateral. The result is growing exposure within private credit portfolios to technology-sector concentration risk, often with less price transparency than public markets afford. Investors in private credit vehicles should scrutinize the degree to which AI infrastructure lending has crept into their allocations.

Tight Spreads, Rising Leverage

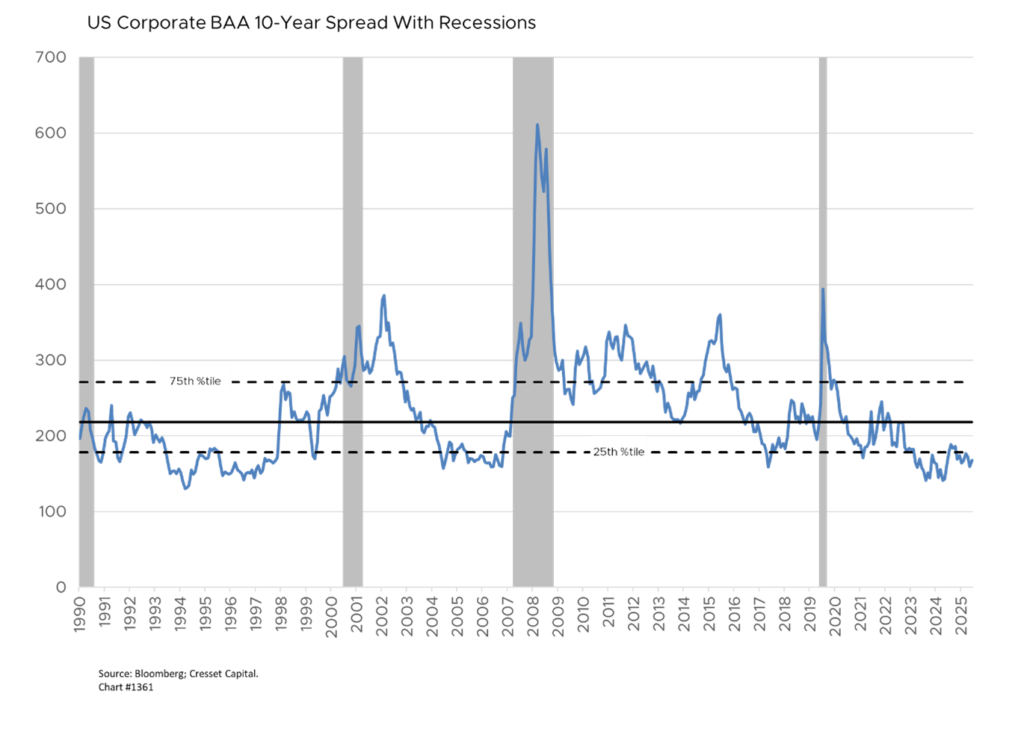

Despite the volume of new supply, credit markets have remained remarkably receptive. Corporate bond spreads are at their tightest levels since 1997, with the extra yield demanded for highly rated corporates hitting a 27-year low in late January 2026. High-yield investors also demonstrated strong appetite also, with technology bond inflows of $1.8 billion in January alone. Yet this demand-supply dynamic masks a more complex underlying risk picture. Rising debt-funded capital expenditures, absent a proportionate and timely earnings uplift, will eventually pressure leverage ratios and erode interest coverage metrics.

The critical question investors must ask is how quickly AI capex translates into monetization, and the current data suggests the gap between spending $400 billion annually across major hyperscalers, and realized AI revenue — about $100 billion — remains wide. The market can likely absorb near-term supply without material spread widening for issuers with strong balance sheets, but that comfort narrows considerably for weaker credits.

Macro Risks Beneath the Momentum

There are two macro-level risks that deserve investor attention. First, the sheer volume of corporate bond issuance is reshaping the U.S. credit market, inadvertently reducing demand for Treasuries as yield-seeking capital flows into higher-quality corporate paper. This dynamic bears watching for its potential impact on Treasury market demand. Second, the growing reliance on special purpose vehicles, off-balance-sheet structures, and private credit channels to finance AI ambitions is introducing greater opacity. If AI investment returns disappoint, a risk that the current revenue gap makes plausible, excess leverage concentrated in these structures could transform a sectoral correction into a broader systemic stress event.

Bottom Line

The AI debt wave presents both an opportunity and a risk. Investment-grade AI issuers with durable competitive moats, strong free cash flow generation, and clear paths to AI monetization remain attractive in the current spread environment. However, investors should resist the temptation to treat all AI-related credit equally. The spread between well-capitalized leaders and leveraged aspirants is likely to widen as the monetization timeline comes into sharper focus. A careful review of AI and software sector concentration is warranted, particularly with the structural shift in how software companies are financing growth. Quality, in both equities and credit, are paramount in this sector.