Key Observations

- Tax-aware private credit is designed to maximize after-tax returns, not just yield

- Equipment leasing enhances tax efficiency through accelerated depreciation

- The OBBBA strengthens incentives with 100 percent bonus depreciation and expensing provisions

- Partnership structures allow tax benefits and losses to flow through to investors

- Tangible asset backing provides additional downside protection

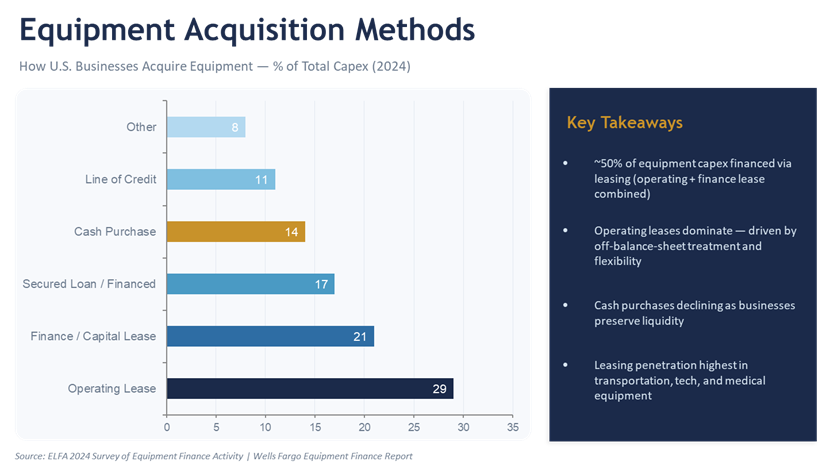

- Demand for leasing remains strong, with about half of equipment acquisitions financed this way

Tax-aware private credit strategies have emerged as compelling investment vehicles that combine attractive risk-adjusted returns with meaningful tax efficiency, particularly through structures involving equipment leasing and other tangible asset investments. These strategies leverage specific provisions in the tax code to deliver enhanced after-tax returns to investors while providing essential financing to middle-market companies.

What Sets Tax-Aware Private Credit Apart

Tax-aware private credit differs fundamentally from traditional private credit, an area of the market generating headlines nowadays, in their structural approach to generating investor returns. Traditional private credit strategies, originally created for institutional, tax-exempt investors, like endowments and pension funds, focus primarily on generating current income through interest payments from direct lending, mezzanine financing, or other credit instruments.

These investments typically generate ordinary income that is fully taxable at the investor’s marginal rate. Recently, private credit offerings have migrated from the institutional world to the private client sector, offering attractive yields to those willing to invest from their qualified accounts, like IRAs. Tax-aware strategies, meanwhile, are explicitly designed to maximize after-tax performance through specific tax benefits that flow through to investors.

The Value of Tangible Asset Exposure

Unlike direct lending, tax-aware private credit incorporates investments in tangible assets such as equipment leasing, renewable energy projects, and other structures that generate significant tax benefits alongside current income. Structured as a partnership, investors can receive tax benefits on a flow-through basis, leveraging the disparity between business and individual tax rates and utilizing expedited loss-recapture rules. Why now?

Policy Tailwinds Strengthen the Case

The recent passage of the One Big Beautiful Bill Act (OBBBA) has created an attractive tailwind for equipment leasing portfolios, enhancing their already attractive tax profile with new fiscal incentives that are expected to stimulate business investment throughout 2026 and beyond. The legislation renews or extends favorable expense provisions, including 100 percent bonus depreciation and immediate expensing of research and development costs, which directly incentivize businesses to invest in equipment through leasing or purchases.

The structural differences mean tax-aware private credit can deliver substantially higher after-tax returns than traditional private credit, particularly for high-net-worth individuals and institutional investors in elevated tax brackets seeking yield with enhanced tax efficiency.

How Equipment Leasing Drives Value

Equipment leasing represents a particularly attractive subset of tax-aware private credit, benefiting from accelerated depreciation provisions that create immediate tax deductions. Recent legislation has restored full bonus depreciation for capital costs, enabling businesses to deduct the full value of new spending from their taxable income in the same year an investment is made, which represents a lucrative benefit for investors in equipment and technology assets.

The partnership structure enables investors to receive regular distributions from the underlying credit investments while simultaneously benefiting from tax losses generated through depreciation and other deductions. These tax losses can be distributed to investors and used against their unrelated business income, with tangible investments eligible for immediate expensing.

Why Businesses Are Turning to Leasing

Leasing has emerged as one of the most compelling financing structures available to businesses, and for good reason. Rather than tying up large amounts of capital in depreciating assets, companies can preserve cash and redeploy it toward higher-return opportunities, whether that means hiring talent, funding R&D, or expanding into new markets. As of 2024, about half of all equipment acquisitions are leased.

The investment advantages of tax-aware private credit extend beyond pure tax efficiency. These strategies typically offer attractive current yields, lower correlation to public markets, and the potential for capital preservation through senior secured lending positions. The equipment leasing component provides additional downside protection through the residual value of the underlying assets, creating a tangible collateral base that traditional corporate credit may lack.

A Compelling Opportunity in a Changing Environment

The combination of current income generation, tax loss pass-throughs, accelerated depreciation benefits, and asset-backed security creates a compelling value proposition for investors seeking tax-efficient yield in an environment where traditional fixed-income investments offer limited after-tax returns. Moreover, equipment asset-backed securities could benefit from fiscal incentives and credit strength, positioning the sector as a preferred securitized asset class in a potentially softening economy.

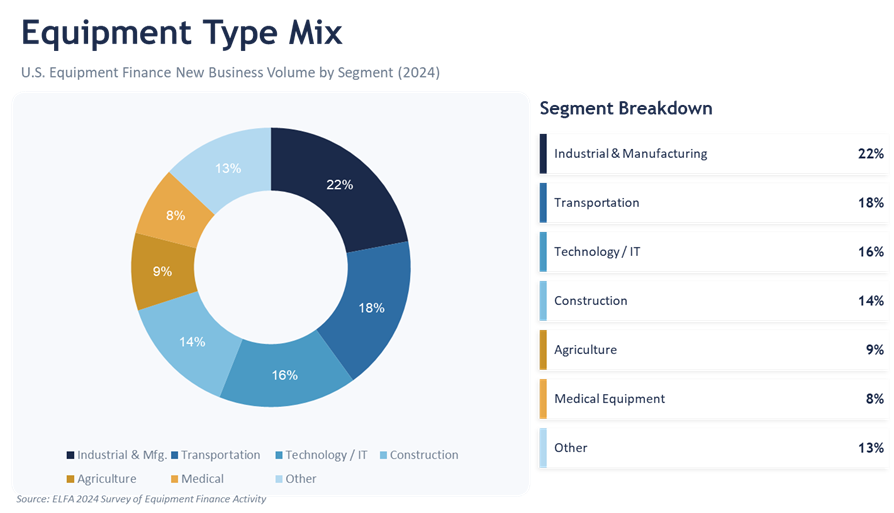

For equipment leasing portfolios specifically, these provisions create a virtuous cycle: enhanced depreciation benefits increase the tax efficiency of leasing structures, while improved business confidence and capital spending incentives drive greater demand for leased equipment across manufacturing, technology, and infrastructure sectors. As regulatory frameworks continue to support investment in productive assets through favorable tax treatment, both tax-aware private credit and equipment leasing strategies — now bolstered by the OBBBA — are positioned to remain attractive components of diversified investment portfolios seeking tax-efficient yield and capital appreciation.

Bottom Line

Tax-aware private credit, anchored by equipment leasing, represents a compelling risk-adjusted opportunity for high-net-worth investors. The strategy delivers current income, meaningful tax efficiency, and tangible asset backing in a single structure, addressing three of the most persistent challenges facing taxable investors. The OBBBA reinforces the case by restoring 100 percent bonus depreciation and extending immediate expensing provisions amplifying the after-tax advantage these strategies carry over traditional private credit. The equipment collateral underlying these portfolios also provides a layer of downside protection that unsecured corporate lending lacks, making the structure relatively defensive and tax efficient.