Key Observations

- AI-driven productivity gains are accelerating workforce reductions across technology and financial sectors.

- Higher-income households, which drive a large share of discretionary spending, are increasingly exposed to job and wage pressure.

- Corporate earnings may benefit in the near term, but demand-side risks are building beneath the surface.

- The scale and speed of AI adoption could compress the traditional adjustment period for labor markets.

- Policy and regulatory responses tend to lag, but history suggests they can emerge quickly once displacement broadens.

- Portfolio construction may need to balance near-term equity strength with hedges against potential demand weakness.

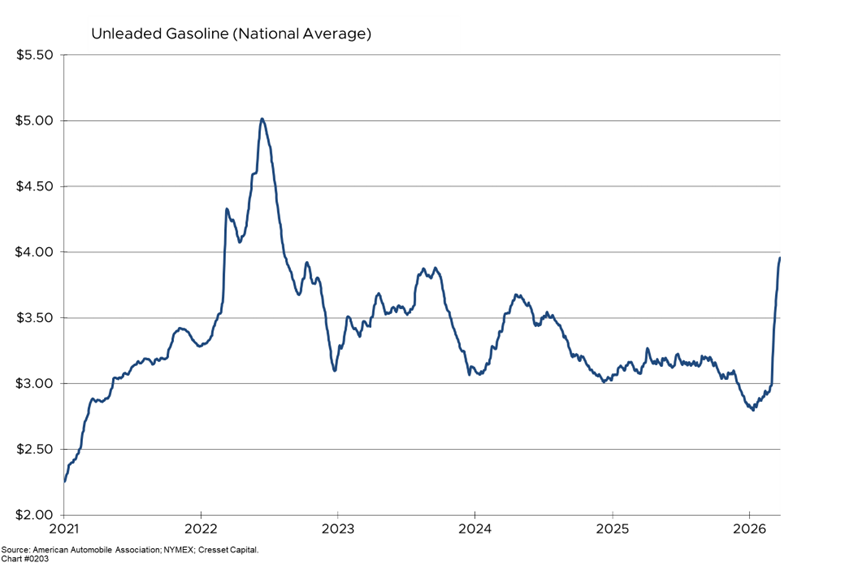

American households are under duress. Pump prices are surging, interest rates are rising, and employers, citing artificial intelligence (AI) productivity gains, are slashing their workforces. Mortgages rates are approaching 6.5%, their highest level since September, while pump prices —at $3.95 per gallon —are at their highest level since 2022.

Just as Americans are reassessing their household budgets, a new wave of AI-related workforce reductions is sweeping through corporate America, raising important questions about productivity, inequality, and the social contract between employers and workers. In recent weeks, major technology companies and financial institutions have announced tens of thousands of job cuts explicitly attributed to AI-driven efficiency gains, marking a potential inflection point in how automation reshapes the labor market.

AI Triggers Corporate Workforce Shifts

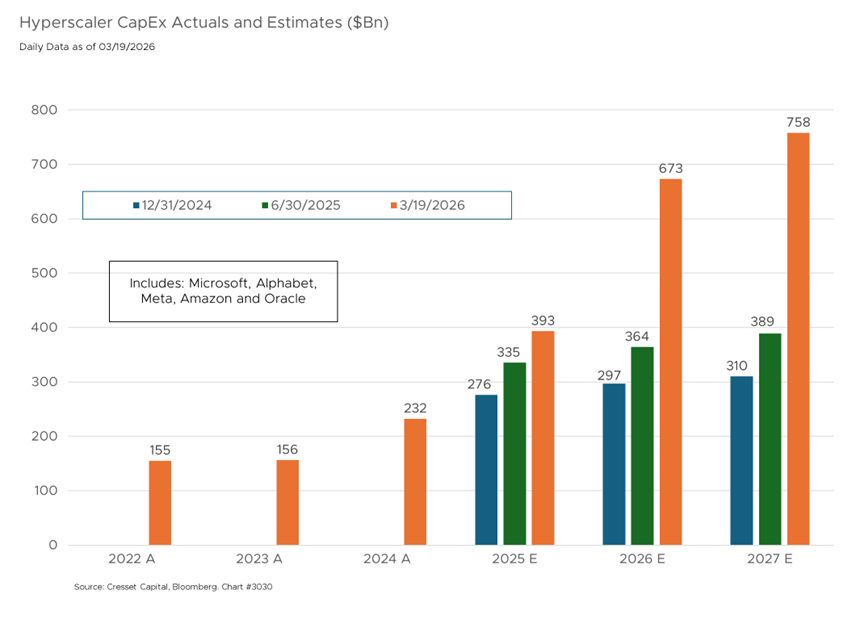

Meta Platforms recently announced planned layoffs that could affect 20% or more of its workforce of approximately 79,000 employees as it seeks to offset massive AI infrastructure spending while simultaneously claiming productivity benefits from the technology. Collectively, the largest hyperscalers are expected to spend $673 billion in infrastructure buildout this year. Block Inc. cut nearly half its staff in late February, with co-founder Jack Dorsey declaring that intelligence tools have changed what it means to build and run a company. Oracle is planning thousands of job reductions aimed at categories the company expects to optimize through AI. Even traditional financial institutions are joining this trend, as HSBC is reportedly weighing cuts of approximately 10% of its workforce, and Nordea Bank is putting as many as 1,500 jobs at risk, citing AI-driven process efficiencies.

The economic implications of this phenomenon extend far beyond the immediate pain of displacement. On one hand, genuine productivity gains from AI could theoretically boost corporate profitability, potentially flowing through to shareholders and enabling further reinvestment in innovation. Analysts have noted that Meta’s reported layoffs could deliver an earnings boost of up to 5% this year, suggesting real efficiency improvements. If AI truly allows companies to produce more output with fewer inputs, this represents the kind of technological progress that has historically fueled higher living standards.

Lessons from Past Technological Shifts

In his book, “Rise and Fall of American Growth,” Robert Gordon cites that the great inventions of 1870 to 1970 —electricity, the internal combustion engine, indoor plumbing, and mass communications —were uniquely transformative, precisely because they touched every dimension of daily life and work simultaneously. In that context, he showed that prior waves of labor displacement were eventually absorbed. Workers pushed off the farm by mechanization migrated into manufacturing. Workers displaced by manufacturing found roles in services. Timing, however, is another matter. AI and robotics carry displacement potential that is qualitatively different from prior waves. Past automation largely replaced physical or routine labor. The concern with AI is that it reaches into cognitive, analytical, and creative work, which has historically been the refuge for workers displaced from manual tasks.

The historical analogy to prior technological transitions, however, is less comforting than it might appear. The mechanization of agriculture and the automation of manufacturing raised aggregate living standards, but the adjustment periods were measured in decades, not quarters. Workers displaced from Midwestern factory floors in the 1980s and 1990s rarely migrated seamlessly into software engineering. The velocity of the current AI transition, compressed by the rapid commoditization of large language models and automation tooling, suggests that the adjustment period this time could be both faster and more disruptive. Policymakers and investors alike should resist the temptation to assume history will repeat itself.

A Labor Market Under Pressure

A recent survey by Resume Builder found that more than half of U.S. companies are reducing or plan to reduce employee compensation to free up capital for AI investments, with 26% planning layoffs, specifically to fund AI efforts by year-end. This raises the troubling prospect that AI’s benefits will likely accrue to capital owners while workers face not only job losses but also wage suppression and reduced benefits. The concentration of these cuts in high-paying technology and financial services sectors could hollow out precisely the middle-class jobs that have provided economic mobility for skilled workers.

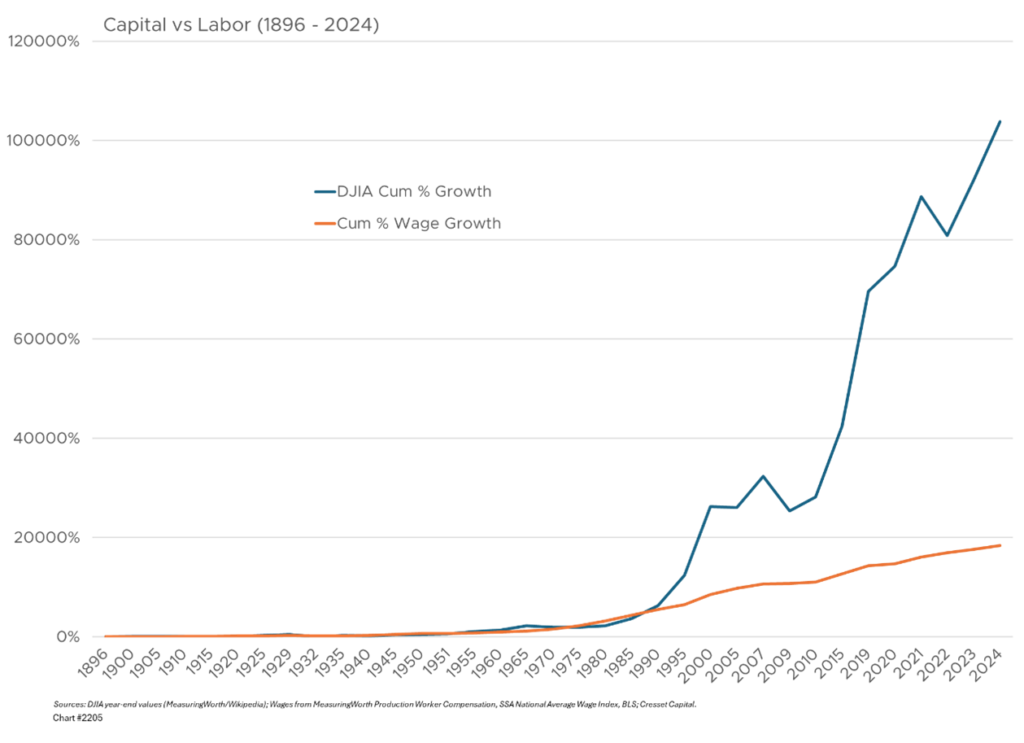

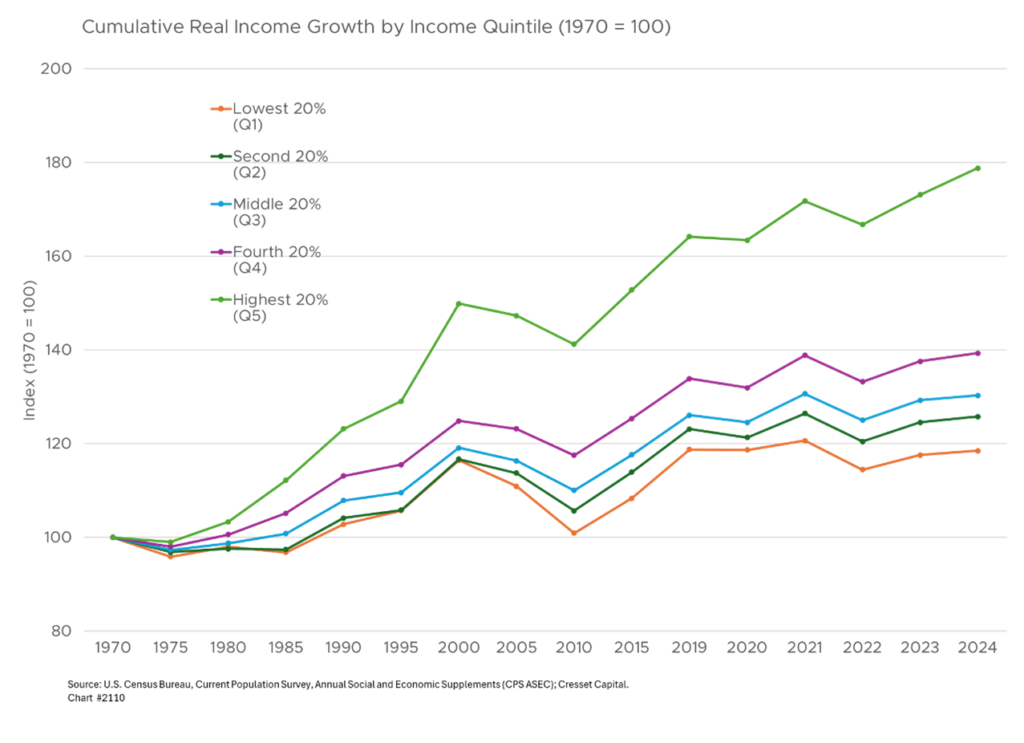

This dynamic matters enormously for the macroeconomic backdrop. The top quintile of U.S. households, many employed in the technology and professional services sectors, who are now experiencing targeted headcount reductions, account for a disproportionate share of discretionary consumption. If AI-driven displacement spreads broadly enough to compress spending among this cohort, the consumer economy could face a meaningful demand headwind. Corporate earnings growth powered by labor cost reduction is not the same as earnings growth powered by expanding revenue, and investors should make that distinction carefully when underwriting current equity valuations. History suggests that most productivity gains have gravitated toward capital owners.

Policy Risk and Political Response

The political implications surrounding AI-driven displacement deserve serious attention. U.S. policymakers have historically enacted regulatory responses when labor displacement exceeds the capacity of safety nets to absorb it. The automation of agriculture through the 1920s, combined with the financial collapse of 1929, displaced workers at a scale that utterly overwhelmed existing charity and local relief systems. The policy response was sweeping, culminating in the New Deal. Today’s deregulatory posture may limit near-term federal intervention, but state-level action, union organizing, and electoral pressure could shift the landscape quickly. Investors underwriting long-duration bets on uninterrupted AI-driven cost extraction should assign non-trivial probability to a regulatory regime that is materially more restrictive in three-to-five years than it is today.

There is also the question of consumer demand sustainability. The companies driving the most aggressive AI-related workforce reductions are, in many cases, the same companies that depend on broad consumer purchasing power for their own revenue growth. A technology sector that systematically hollows out the middle-class wage base risks weakening the very demand environment that sustains its own product adoption. This feedback loop is not hypothetical. It is the same structural tension that has characterized every major wave of labor-replacing capital investment, and it has never resolved itself cleanly or quickly.

What This Means for Investors

For investors, the AI-driven labor market disruption playing out in real time has a set of implications that cut in multiple directions simultaneously, and clarity requires separating the short-term earnings story from the medium-term macro risk.

In the near term, expect margin expansion for large-cap technology and financial services companies. Genuine productivity gains from AI deployment are flowing through income statements, and companies that are disciplined about translating headcount reduction into durable free cash flow growth deserve credit for it. The earnings impact should not be dismissed as purely financial engineering.

Risks Beyond the Near Term

The medium-term investment landscape, however, carries several underappreciated risks. First, the concentration of AI capex spending among a small number of hyperscalers creates systemic exposure to any demand disappointment on the revenue side. If efficiency gains compress the labor income of the workers who are also the consumers of these platforms, the revenue base that justifies the infrastructure buildout may prove more fragile than consensus assumes. Second, the political and regulatory risk premium embedded in AI-focused equities is likely too low. History suggests that labor displacement at scale could prompt a legislative response, and the timeline for that response has a way of arriving faster than equity markets price it.

Third, and perhaps most importantly for portfolio construction, the K-shaped economic distribution that has defined the post-pandemic recovery is entering a new and more acute phase. As AI-driven displacement spreads from lower-wage service roles into higher-wage knowledge work, the bifurcation of consumer spending power could become a more visible drag on aggregate demand. Companies exposed to discretionary spending could be at risk.

Bottom Line

AI is a genuine and powerful driver of corporate efficiency, and we expect the associated productivity gains will be astonishing. While we are not shifting our asset allocation targets, we underscore the importance of owning equities. If history is a guide, AI productivity gains will gravitate toward corporate profits and new business formations, as companies in virtually all industries are able to deliver top line growth more efficiently.