Key Observations

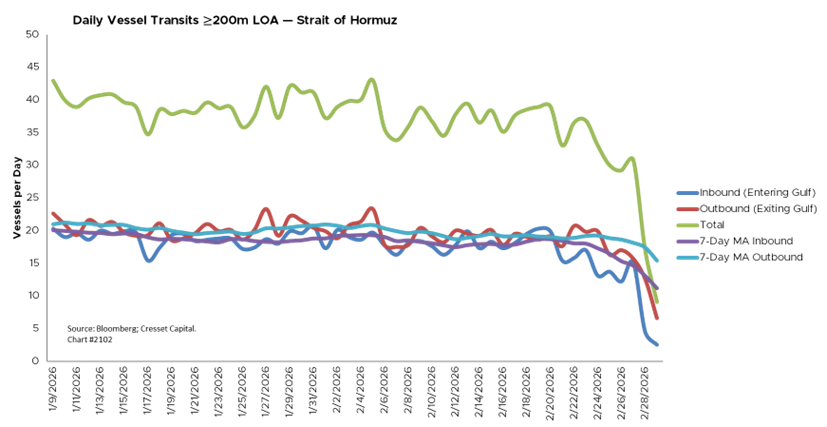

- The Strait of Hormuz remains the single most important variable; disruption would trigger a broad repricing across energy, inflation, and rates.

- Oil is the immediate transmission channel, with sustained elevation feeding directly into inflation expectations.

- The Federal Reserve faces a renewed policy dilemma: contain energy-driven inflation or cushion a softening economy.

- Safe-haven assets (gold, Treasuries, USD, Swiss franc) are likely near-term beneficiaries of risk aversion.

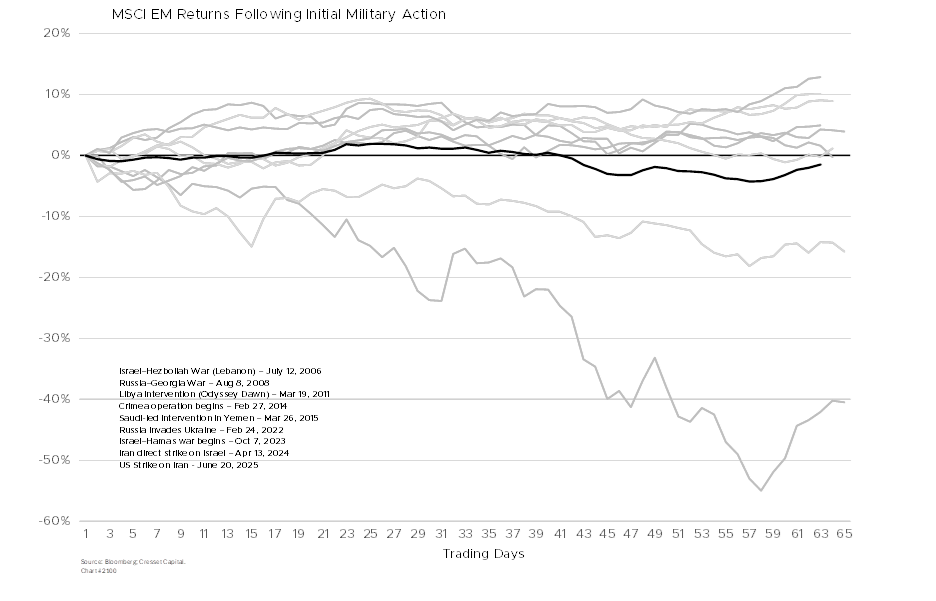

- Cyclicals and energy-importing emerging markets face pressure.

- China and broader Asia are particularly vulnerable given their dependence on Middle Eastern crude flows.

The coordinated U.S. and Israeli strikes on Iranian strategic targets, including the killing of Supreme Leader Ali Khamenei, represent a qualitative escalation of geopolitical risk over the weekend. The conflict represents a structural rebalance with direct implications for energy supply, inflation, monetary policy, and global capital flows.

Energy: The Primary Transmission Channel

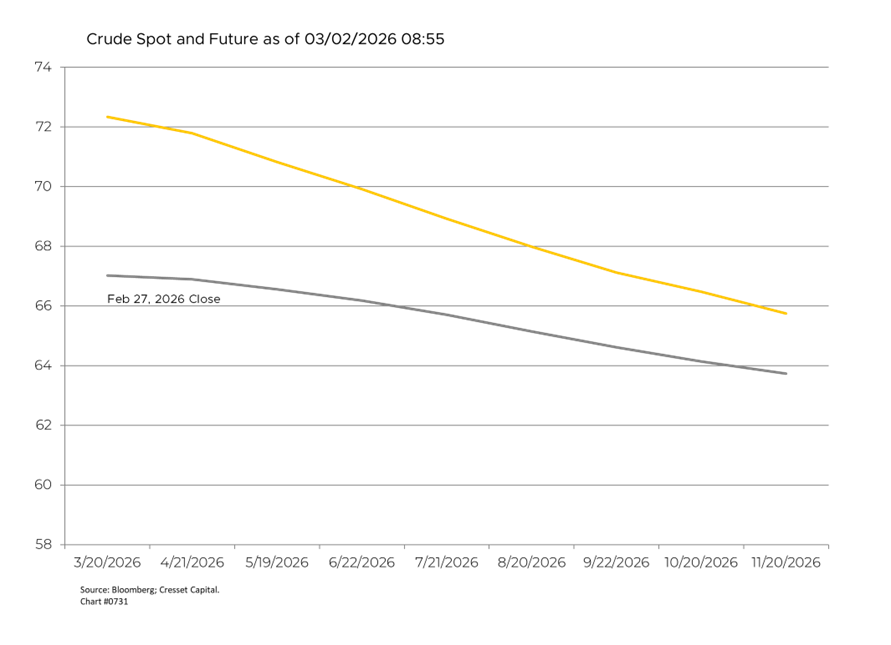

Oil is the immediate transmission mechanism. Prices have already spiked on supply disruption fears, and analysts are warning of a range spanning between $75 to $100+ per barrel depending on conflict trajectory, with extreme escalation scenarios projecting $108–$140 if the Strait of Hormuz is indefinitely closed or blockaded. The Strait is a logistical chokepoint that handles roughly 20% of global oil and liquefied natural gas (LNG) flows.

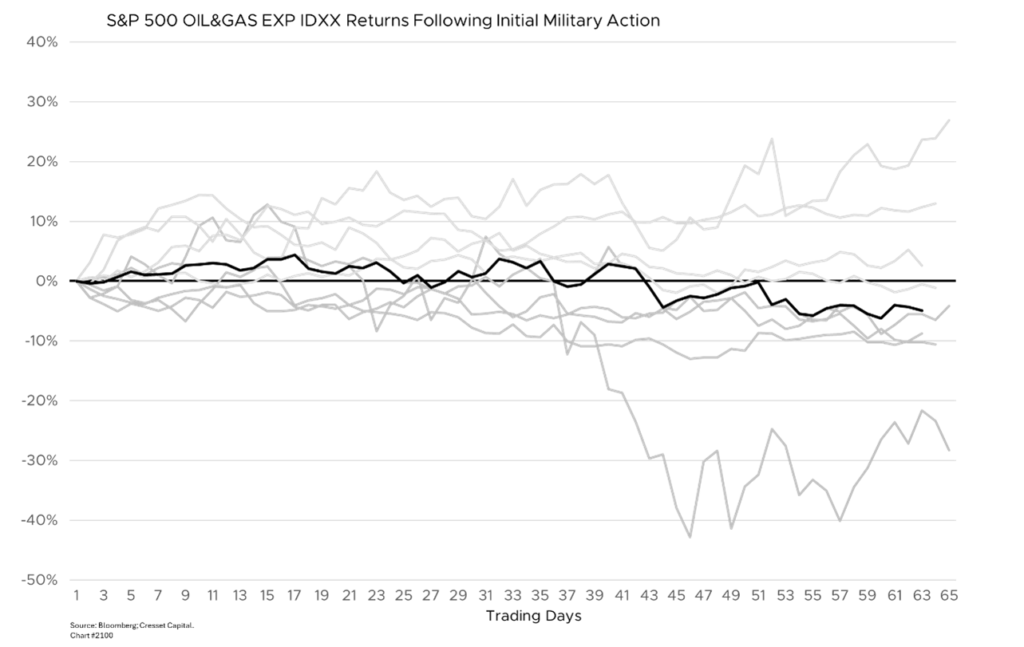

Oil exploration and production companies benefit from sustained price strength, followed by gas producers and oilfield services. Meanwhile, midstream infrastructure and shipping companies face elevated risk and rising insurance costs, offsetting revenue increases. Iran-backed Houthi rebels have already signaled a resumption of Red Sea shipping attacks, adding another layer of supply chain disruption that directly affects freight rates and LNG spot pricing. History suggests that energy prices tend to peak two weeks after the initial headline and slowly recede.

Inflation Pressures and the Federal Reserve’s Policy Crossroads

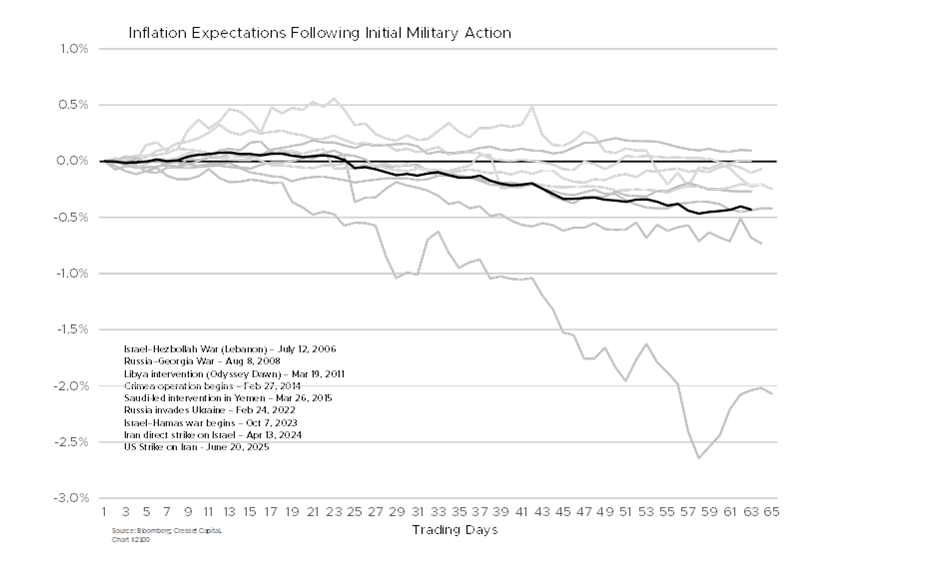

Sustained energy price elevation is a direct inflationary input through transportation, manufacturing, and energy costs. Unlike the 1970s and 1980s, energy shortages are no longer a vulnerability for the U.S., since we produce more than 13 million barrels per day. Nonetheless, high pump prices complicate the Fed’s job. Monetary policymakers have been navigating a K-shaped economy already under pressure from softening labor conditions and deteriorating lower-income consumer fundamentals. A persistent war-risk premium in oil forces a difficult choice: hold rates longer to contain inflation and risk deepening economic fragility, or cut as planned and risk a second inflationary wave. Treasury Inflation-Protected Security (TIPS) spreads, breakeven inflation rates, and Fed communication will be critical signal sources in the coming weeks. History suggests inflation expectations, like high oil prices, tend to dissipate over time.

Risk Sentiment, Safe Havens, and Portfolio Positioning

Historical precedent is clear: geopolitical shocks of this magnitude drive near-term flight to quality. Gold, U.S. Treasuries, the Swiss franc, and the U.S. dollar are the natural beneficiaries. Cyclical, higher-beta sectors, like real estate, banking, and industrials, face headwinds from wider risk spreads and risk-off positioning. Emerging market assets are also vulnerable, especially energy-importing economies where rising import bills compound current account pressures and drive capital outflows. Defense and cybersecurity equities should also see sustained tailwinds, as this conflict almost certainly accelerates defense budget reallocations globally.

China, which imports roughly 38% of its oil from the Persian Gulf, is particularly vulnerable to supply disruptions from a Strait of Hormuz blockage. Over 60% of China’s petroleum was imported in 2022, with approximately 56% of those shipments originating from the Middle East. Moreover, 80% of crude oil moving through the Strait of Hormuz is destined for Asia.

Bottom Line: What Investors Should Be Watching

The Strait of Hormuz remains the single most important variable; any disruption would likely trigger a systemic repricing across energy markets, inflation expectations, and interest rate outlooks. Beyond that, investors should closely monitor decisions from the Organization of the Petroleum Exporting Countries (OPEC+) regarding spare capacity, as well as any potential strategic petroleum reserve releases.

Watch communications from the Federal Reserve and the European Central Bank (ECB) for shifts in inflation language, and monitor the CBOE Volatility Index (VIX) and credit spreads as real-time indicators of market stress. The scope of Houthi and other proxy retaliation will be critical in determining whether this remains a contained bilateral conflict or escalates into a broader regional war. In this environment, position sizing and risk discipline matter more than aggressive rotation. The geopolitical risk premium is now a macro variable, and patience is paramount. History suggests time is on our side.