Key Observations

- Rising energy prices tied to the Iran conflict are amplifying inflation and recession risks

- Economic data signals a slowing backdrop: weak GDP growth, higher unemployment, and persistent price pressures

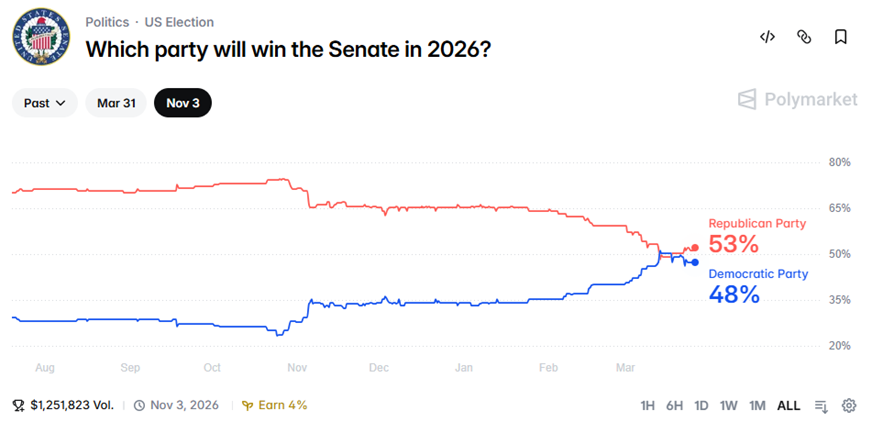

- Republican electoral vulnerability is increasing, though a full Senate flip remains uncertain

- Policy outcomes, especially taxes and spending, carry meaningful implications for markets

- Market volatility is likely to persist through November amid elevated political uncertainty

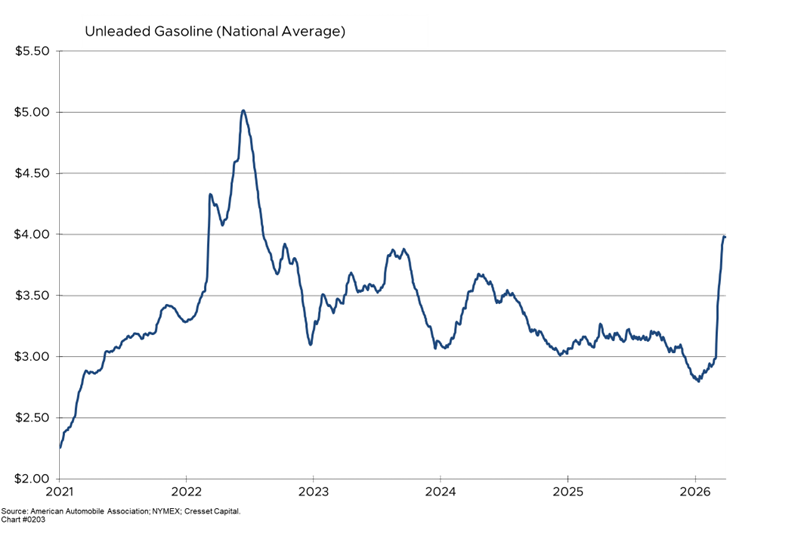

The 2026 midterm elections are unfolding against a backdrop of economic uncertainty and political turbulence, creating a tenuous landscape for the Republican Party. President Donald Trump’s decision to engage in military action against Iran has emerged as the dominant factor reshaping today’s electoral environment, triggering a cascade of economic consequences that threaten to upend his party’s congressional majorities. The conflict has driven energy prices much higher, straining household budgets and rekindling inflation fears just as voters prepare to render their judgment in November.

Economic Stress Signals Are Mounting

The economic data paints a picture of mounting stress on American households. Inflation stands at 2.4% year-over-year as of February, unemployment has ticked up to 4.4%, and GDP growth slowed to just a 0.7% annualized rate in Q4. Meanwhile, pump prices have surged, and mounting airport security delays only added to a potent sense of economic malaise.

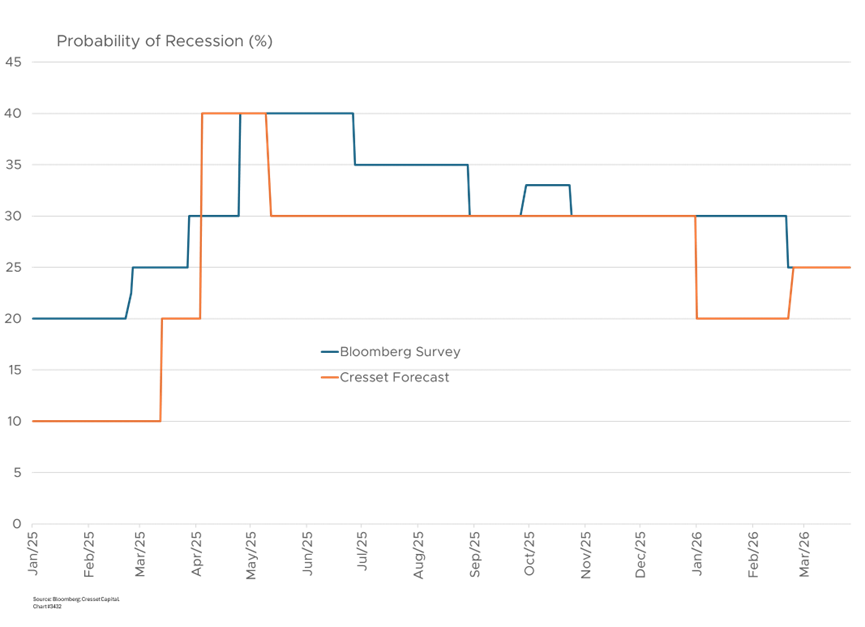

Cresset recently raised its recession probability to 25%, although another few weeks of constrained traffic through the Strait of Hormuz would prompt us to consider the probabilities for higher recession risk in the U.S. Meanwhile, Moody’s Analytics now puts the odds at nearly 50%, reflecting growing concern that the Iran conflict could tip the economy into contraction by mid-year.

Political Pressure Builds Beyond the Polls

The political headwinds facing Republicans extend well beyond polling data. Last weekend, millions of Americans took to the streets for the third consecutive “No Kings” demonstrations, with organizers claiming eight million participants across thousands of rallies, and nearly half of the events occurring in red or battleground states.

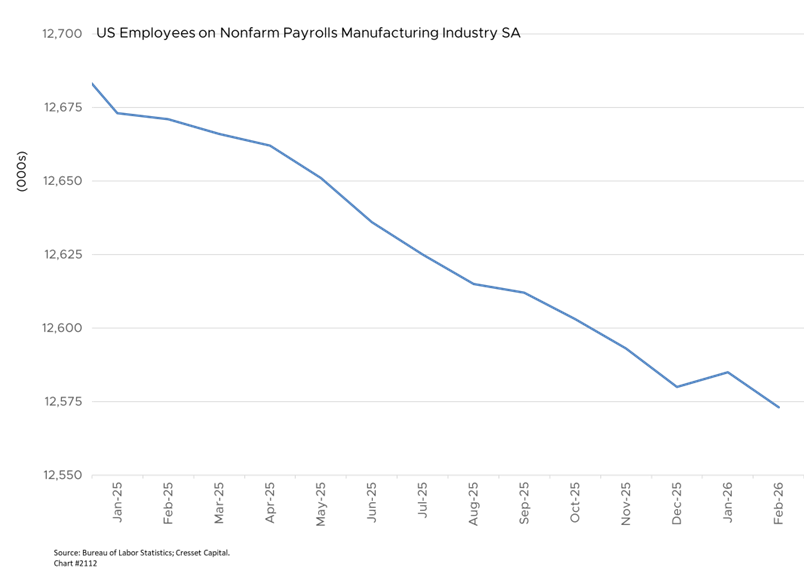

One year after Trump’s “Liberation Day” tariff announcement, factory employment has fallen by nearly 100,000 jobs, inflation has climbed to 3.1% on the Fed’s preferred gauge, and manufacturing output remains below Biden-era levels. The Iran conflict has compounded the damage. Rising energy costs threaten to reverse the modest manufacturing improvement of recent months, and businesses remain reluctant to commit capital in an environment described as “uncertain and unpredictable.”

A Shifting Electoral Map with Surprising Signals

The combination of war fatigue, cost-of-living frustration, and tariff-driven economic disruption is creating an opposition narrative that cuts across demographic lines. Underscoring the trend, a recent Democratic victory in a Florida state House district that includes Trump’s Mar-a-Lago residence, and which favored him by 11 points in 2024, shocked party insiders.

Senate Republicans, once confident about maintaining or expanding their majority, are now openly anxious, with some expressing relief they’re not on the ballot this cycle. Some Republican strategists worry the Iran war could cost them their Senate majority, a chance we believe is small. Yet even traditionally loyal constituencies are wavering. Farmers are facing crushing fertilizer and fuel costs, while Latino voters, many of whom helped deliver Trump’s 2024 victory, appear to be reconsidering their allegiance as economic and immigration concerns intensify.

Democratic Momentum Meets Structural Constraints

Notwithstanding the difficult environment for Republicans, Democrats still face a tough map as they look to win the four seats to claim a majority in the Senate, and will have to win some long-shot races to get there. Republicans are defending nearly two-thirds of the Senate seats on the ballot in 2026. Prediction markets suggesting that Democrats have a nearly equal chance of retaking the Senate after the midterm elections are overstating the likelihood.

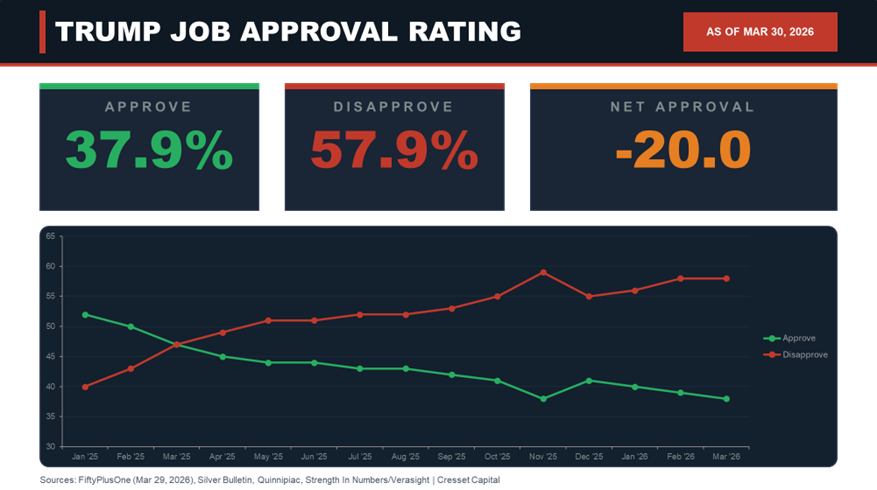

A Democratic takeover of the Senate is now within reach, challenging the conventional wisdom that Democrats would win back the House but fall short in the Senate. The current political environment, driven by President Trump’s low approval ratings and opposition to the Iran war, has created momentum that Democrats are seeking to capitalize on across multiple competitive races.

Policy Stakes Rise for Markets

Even if Democrats capture the House, it could make voting for Republican-led energy reform politically unattractive for Democratic Senators, according to Bloomberg Research. The prospect of a second reconciliation bill like the One Big Beautiful Bill Act (OBBBA) would struggle to become law under such circumstances, though smaller targeted bills focused on areas like cryptocurrency regulation might still garner bipartisan support.

Democratic control of the Senate, however, would reopen the debate over rolling back the 2025 tax cuts, potentially reversing the corporate rate reduction from 21% back toward 28% and reinstating higher individual rates on top earners. The prospect of a meaningful increase in the effective corporate tax rate would, all else equal, compress S&P 500 earnings by an estimated 4% to 8%, depending on sector exposure and the legislative calendar. Equity markets, already navigating slowing growth and elevated geopolitical risk, could face earnings pressure even if the gridlock itself were viewed as stabilizing.

Fixed Income: Balanced Risks, Subtle Shifts

Fixed income markets would experience a more nuanced response. The initial reaction in Treasuries could be counterintuitive. A Democratic Congress that blocks further deficit expansion and resists additional unfunded tax cuts might provide modest relief to the long end of the yield curve, where concerns about fiscal sustainability are keeping term premium elevated. However, Democratic spending priorities, including expanded social programs, green energy subsidies, and healthcare entitlements, carry their own fiscal costs that could ultimately offset any near-term deficit discipline. The net effect on the 10-year Treasury yield is likely modest, but the composition of the deficit would shift meaningfully, with revenue measures replacing borrowed financing at the margin. Credit markets — particularly investment-grade and high-yield corporates — would closely track equity sentiment, with the greatest spread widening in sectors facing the most regulatory exposure.

Bottom Line

The 2026 midterm elections are shaping up to favor meaningful Democratic gains. The combination of a slowing economy, elevated inflation, war fatigue, and historically poor midterm performance for the party in power creates a powerful structural tailwind for Democrats. Whether they achieve a narrow House majority, a Senate flip, or a full sweep will determine the magnitude of the market reaction, but the direction of travel with seven months to go is increasingly clear.

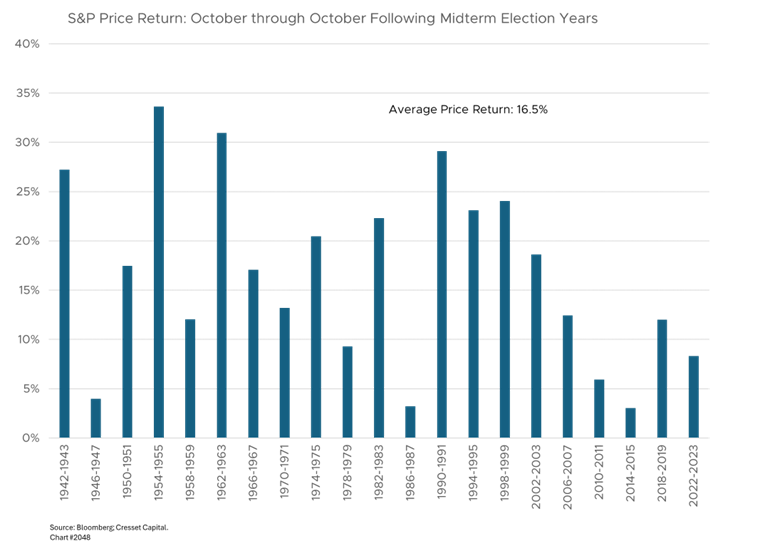

History is an imperfect guide, but in every midterm cycle since World War II, the S&P 500 has posted positive returns in the twelve months following the election, averaging roughly 16.5% regardless of which party prevailed. The real risk is not political change per se, but the policy uncertainty that precedes it. That uncertainty is elevated now and will remain so through November. Diversified, tax-efficient portfolios allocated to quality equities and bonds are expected to help weather the transition and capture the recovery that has historically followed once the electoral fog lifts.