Key Observations:

- Private credit has scaled rapidly, now representing ~6% of U.S. GDP and expected to double within five years

- Recent stress reflects liquidity mismatch, not broad credit deterioration

- Bank exposure to non-bank financial institutions creates potential (but not immediate) contagion channels

- Retail access has introduced misaligned expectations around illiquidity and taxes

- AI-driven disruption may pressure certain sectors, but recovery rates remain historically strong

- The market is shifting from yield-driven growth to structure- and asset-quality-driven selectivity

Over two decades, private credit transformed from a niche corner of corporate finance into a pillar of lending that now rivals traditional bank channels in scale and influence. From just 1% of U.S. nominal GDP in 2008, the asset class has grown to represent 6% today; a market now valued at approximately $1.8 trillion. It’s expected to double within five years.

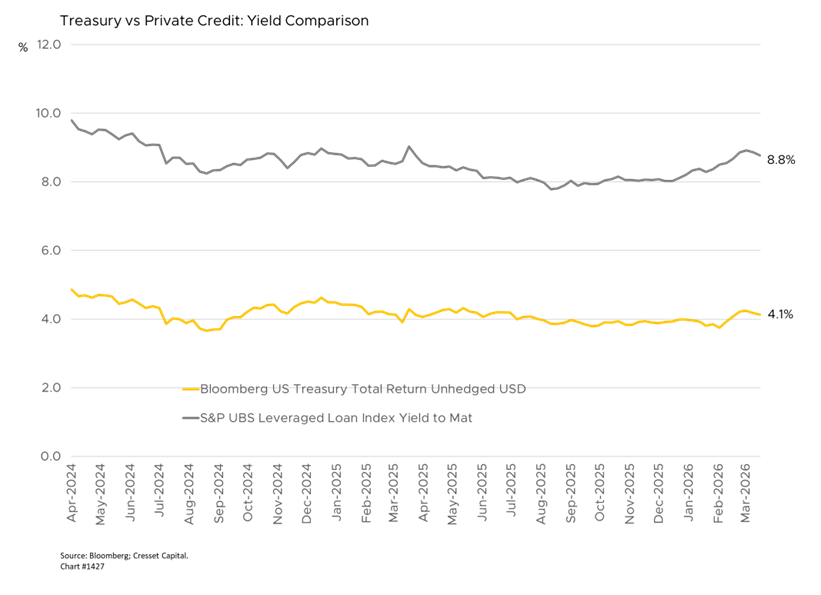

As banks pulled back from leveraged lending after the global financial crisis, private credit stepped in, offering borrowers certainty of execution, flexibility, and speed that syndicated markets could not always provide. For investors, the asset class delivered attractive spreads as loan yields have stabilized around 5% while delivering a track record of stable credit performance through multiple economic cycles.

The Democratization of Private Credit

For most of the last decade, direct lending was the exclusive domain of institutional investors who were largely indifferent to taxes and were comfortable locking up capital for years. In that environment, scale mattered more than structure and yields in the high single digits to low double digits easily compensated for a multi-year lockup.

Thanks to a burgeoning private wealth capital base, private credit is no longer the exclusive province of pensions and endowments. Over the past several years, profit-seeking sponsors redirected distribution toward wealth management platforms, particularly brokerages, where liquidity preferences, tax sensitivity, and demand for transparency differ materially from institutions. Interval funds, non-traded business development companies, and other semi-liquid vehicles put the strategy within reach of retail investors.

A Structural Mismatch Emerges

Unfortunately, that expansion created a structural tension. While family offices and sophisticated investors often have fewer liquidity needs, many individual investors accessing private credit through mass-market channels, particularly with low minimums, were unfamiliar with illiquidity. Distributing to the retail channel created a mismatch between investor expectations and fund mechanics.

Traditional direct lending generates ordinary income, often fully taxable at marginal rates, making after-tax outcomes meaningfully less compelling than headline yields suggest. Sophisticated investors and families have the wherewithal to employ tax-exempt portfolios, like retirement accounts, private foundations, or private placement life insurance to invest in direct lending strategies. The after-tax benefit of direct lending strategies in taxable portfolios is attractive, but not as compelling as the strategy held in tax-exempt portfolios.

Interpreting Recent Market Stress

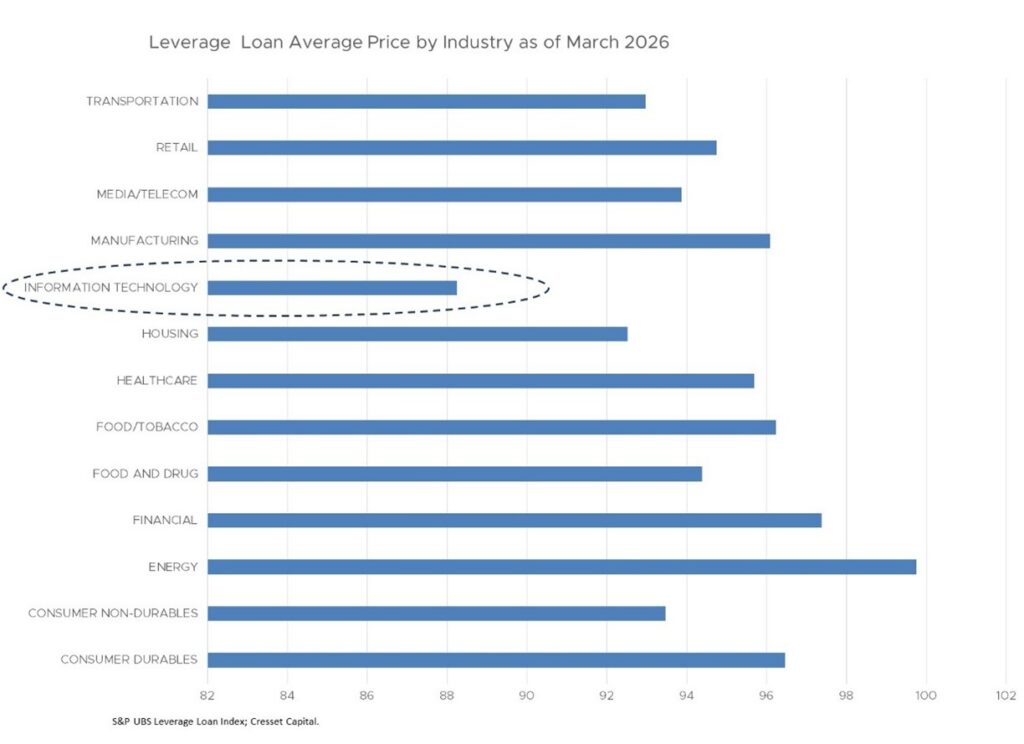

The current stress in private credit is real, but it is largely misunderstood. Catalyzed by fears that artificial intelligence (AI) innovation could dislocate traditional software companies, recent redemption surges and fund gates have prompted comparisons to systemic financial events. Those comparisons misread the evidence. While prices of technology loans have retreated, loans to virtually every other industry have remained stable. What we are witnessing is a liquidity mismatch, not a credit contagion.

Private credit is, by its nature, illiquid. Loans to middle-market companies do not trade on exchanges and cannot be liquidated on demand at fair value. Yet many vehicles created to distribute this asset class offer periodic redemption windows. When market volatility shakes investor confidence, those windows become pressure points.

Systemic Risk in Context

The systemic risk argument deserves a closer look. Private credit is not currently in crisis, but conditions for a credit cycle do exist given the market’s size, leverage, sector concentration, and opacity. U.S. and European banks collectively hold approximately $1.3 trillion in loans and $1.1 trillion in undrawn commitments to non-bank financial institutions, creating real channels of contagion if stress were to intensify.

AI-driven disruption could increase default rates, potentially doubling Fitch’s current private credit default rate of 5.2%. However, it should be noted that historical recovery rates, the value lenders recover, have historically been between 70% and 80%, depending on the industry sector and loan covenants. The opaque nature of private portfolios makes these risks difficult to price and harder to monitor in real time.

Why This Is Not a Classic Crisis

Notwithstanding recent headlines, the private credit investor base is dominated by pension funds, insurance companies, and sovereign wealth funds, or institutions with long investment horizons and limited immediate liquidity needs. These are not depositors subject to bank-run dynamics. They are institutional allocators operating within contractual lockup structures. The redemption pressure we are seeing is uncomfortable, but it is occurring within vehicles designed to absorb it.

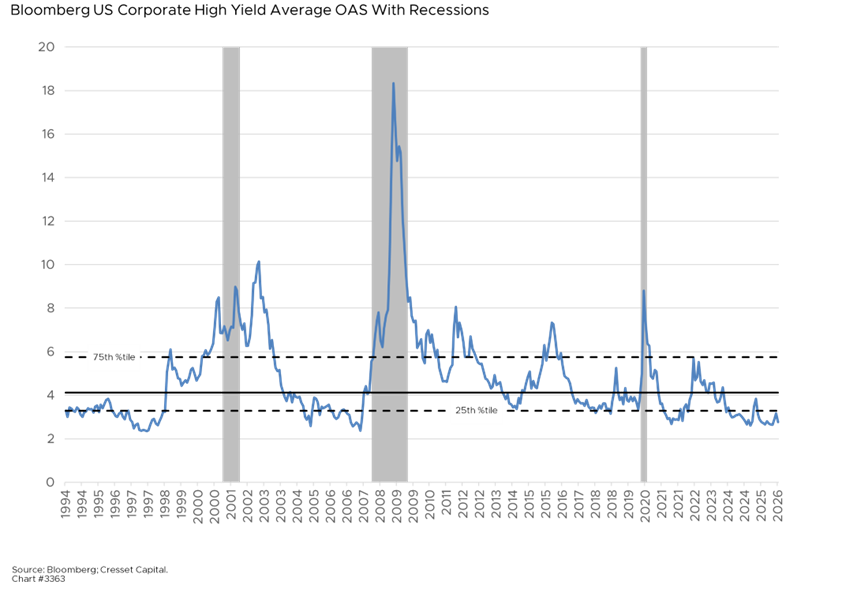

The underlying credit fundamentals are stable. The performance across private loans and lower middle market holdings remains stable, with consistent revenue and earnings before interest, taxes, depreciation, and amortization (EBITDA) trends, as well as limited non-accrual exposure. Public market credit conditions underscore that view. The yield premium lenders require to extend loans to below investment grade borrowers remains in the bottom quartile of its historical range.

The Shift Toward Selectivity

The more consequential shift in private credit is not about redemption queues; it is about selectivity. Specifically, the criteria sophisticated investors are now applying to a broader and more complex opportunity set.

Asset-backed segments of private credit are attracting increased attention, not because they are new, but because they offer greater clarity while delivering tax advantages. Investments tied to contracted or tangible assets, like equipment leasing, infrastructure cash flows, and royalty streams, create a more direct link between ownership and income. They also introduce an additional layer of protection through the value of the underlying collateral.

For taxable investors, structure matters as much as income. Certain asset-backed strategies incorporate features such as accelerated depreciation, and recent tax policy changes, including the restoration of full bonus depreciation, are reinforcing their appeal by improving after-tax outcomes relative to traditional direct lending strategies.

Bottom Line

The redemption pressures, fund gates, and valuation anxiety defining early 2026 trace back to a structural mismatch between illiquid assets and semi-liquid vehicle design, not necessarily deteriorating credit quality or systemic contagion. The market is completing a necessary transition from specialist strategy to mainstream asset class, a process that invariably involves friction and investor education.

The sponsors leading new fund launches are not fleeing the asset class. Spreads in the 5% range continue to offer meaningful compensation over public credit alternatives. Middle-market borrowers still need flexible capital, and banks remain structurally constrained from supplying capital at scale.

What looks like pressure in private credit today is, in many cases, the result of investors applying more disciplined standards to a broader and more complex opportunity set. Capital is still available, but it is no longer indifferent. In a market that grew under a different set of assumptions, selectivity is paramount.