Key Observations

- Enrollment declines and pricing pressure are eroding higher education’s core revenue model

- Costs continue to rise faster than revenues, compressing margins across most institutions

- Structural rigidity — particularly tenure — limits universities’ ability to adapt

- The sector is bifurcating between well-capitalized institutions and vulnerable regional schools

- Policy risk is rising, with funding changes impacting both elite and lower-income-serving institutions

- For investors, the environment calls for selectivity, not broad avoidance

It’s graduation season. Across the country, commencement speakers are donning academic robes and offering the class of 2026 their wisdom, urging graduates to follow their passion, embrace failure, and change the world. If I were fortunate enough to receive such an invitation, I would take a different approach. I would look beyond the graduates and direct my remarks to the administration. It’s the people running these institutions, not the students graduating from them, who most need guidance right now.

There are nearly 2,000 private, nonprofit colleges and universities in the United States, serving over five million students. We expect half of them will disappear over the next five years. Hampshire College is a case in point. The college announced last week it will permanently close at the end of the year after the fall semester, citing insurmountable financial pressures. The Massachusetts liberal arts school, established in 1971, becomes the sixth U.S. university closure this year.

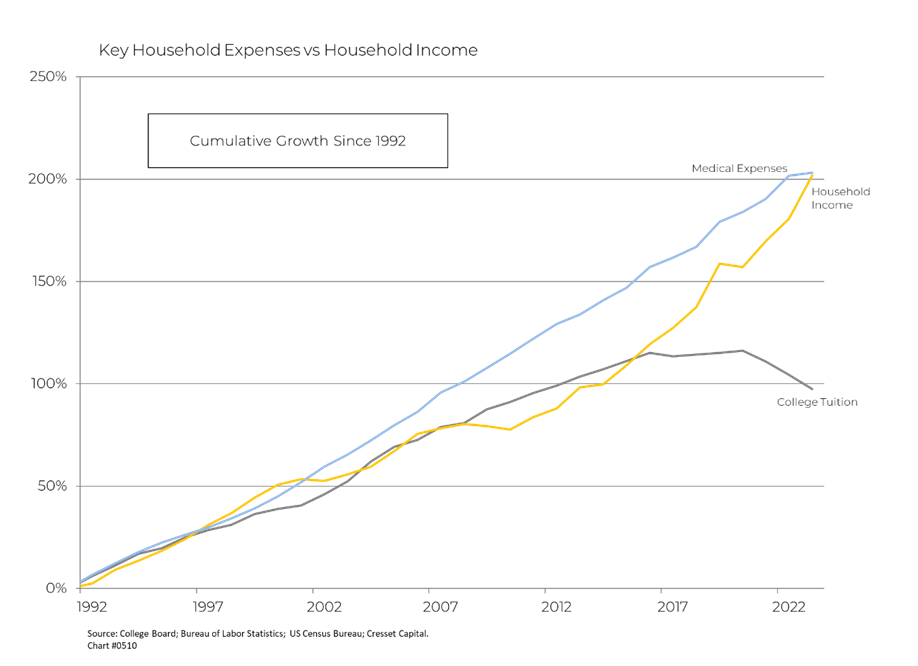

College and university administrations face an unprecedented convergence of crises threatening their financial viability and operational models. The fundamental challenge centers on a dramatic erosion of public confidence: according to recent polling, 63% of Americans now believe a four-year college degree isn’t worth the cost, a stunning reversal from 2013 when 53% viewed it as worthwhile. This sentiment spans political affiliations, age groups, and even extends to college graduates themselves, with more than half now questioning the value proposition. College tuition, which exhibited remarkable pricing power for decades, has stagnated and recently reversed.

Policy Shock: Washington Enters the Equation

The Trump administration has intensified pressure through multiple channels. Federal research funding freezes have impacted elite institutions, including Harvard with $2 billion frozen, as well as Northwestern and Columbia. Meanwhile, the National Institutes of Health (NIH) faces potential budget cuts that could eliminate over $100 million annually for some research universities.

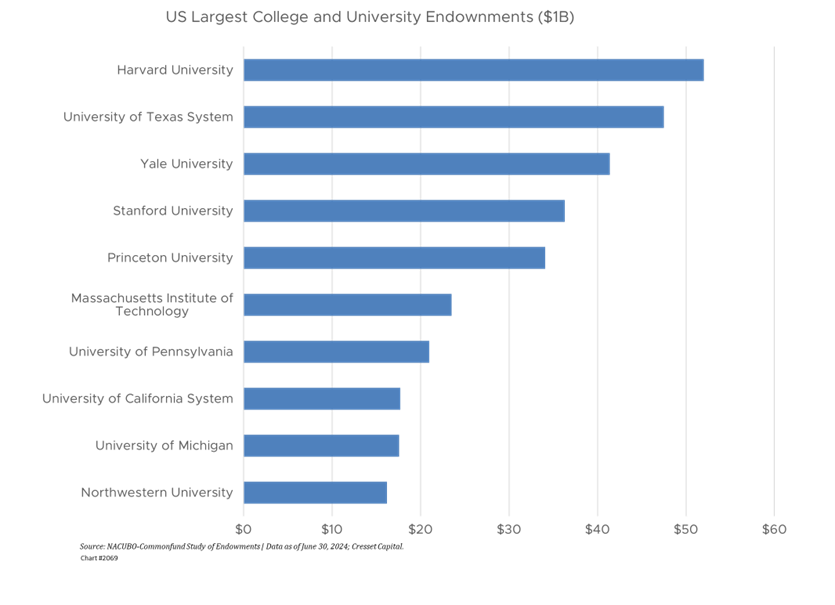

Perhaps most consequentially, the One Big Beautiful Bill Act (OBBBA) raised endowment excise taxes from 1.4% to tiered rates of 4% and 8%, with Harvard, Stanford, Yale, Princeton, and MIT facing the highest bracket, collectively owing an estimated $1 billion over five years.

The Revenue Squeeze

Administrations confront a multifaceted revenue crisis. Despite double-digit investment returns for many endowments, recent gains cannot offset the quadrupled tax burden. Many endowments leaned into illiquid private assets and cannot meaningfully adjust portfolios to reduce tax exposure, leaving spending cuts, or secondary sales, among the most viable responses.

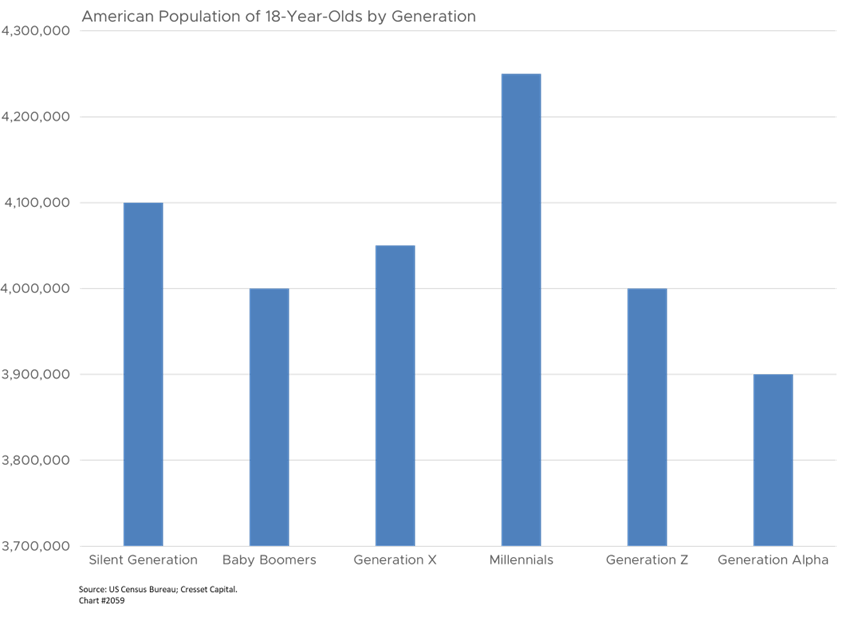

Simultaneously, the student pipeline is contracting. The “demographic cliff,” a sharp decline in high school graduates, particularly threatens small private institutions which draw from local populations. New international student enrollment fell 17% in 2025, as visa restrictions and policy uncertainty deter foreign applicants. With international students typically paying full tuition, this represents a critical revenue source evaporating.

Federal student loan reforms compound these pressures. The new borrowing limits —$100,000 for master’s degrees, $200,000 for professional degrees, and elimination of the Grad PLUS program — force many prospective students toward private loans with stricter terms. The sole remaining income-driven repayment plan is less generous, making debt burdens more daunting and potentially suppressing enrollment further.

The Tenure Trap: When Job Security Becomes Rigidity

The tenure system, once designed to protect academic freedom and attract brilliant minds to university careers, has become a structural impediment preventing colleges and universities from adapting to rapidly changing educational and economic demands. This institutional rigidity compounds the financial and strategic challenges facing higher education at precisely the moment when agility is most critical.

Fixed Cost Structure in a Variable Revenue Environment

Tenured faculty represent an enormous, fixed cost, typically 60-70% of instructional budgets, that universities cannot easily reduce or shift when enrollment declines or revenue streams contract. Unlike corporations facing market disruptions, universities cannot restructure their workforce through layoffs or departmental closures without protracted grievance procedures and potential litigation. When Northwestern, Columbia, and Duke implemented recent cost-cutting measures, they targeted administrative staff and non-tenured positions while tenured faculty remained largely insulated.

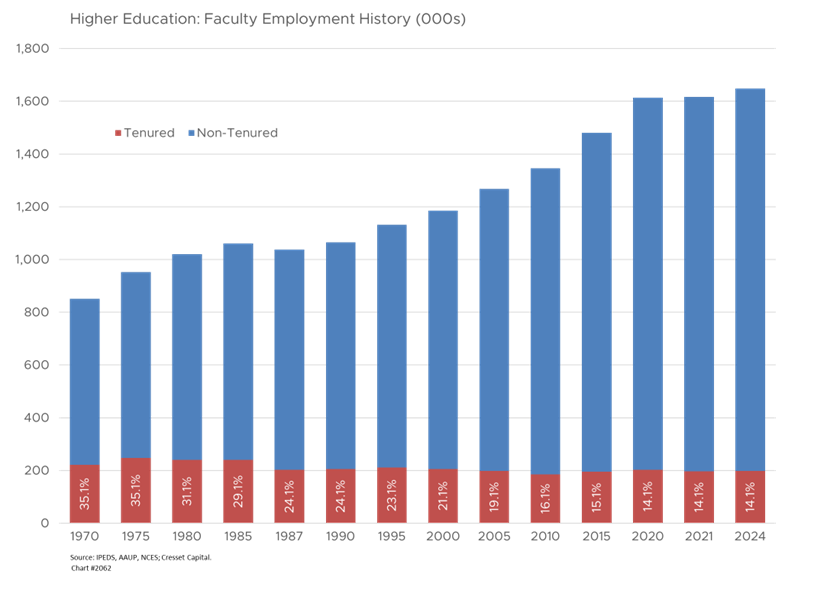

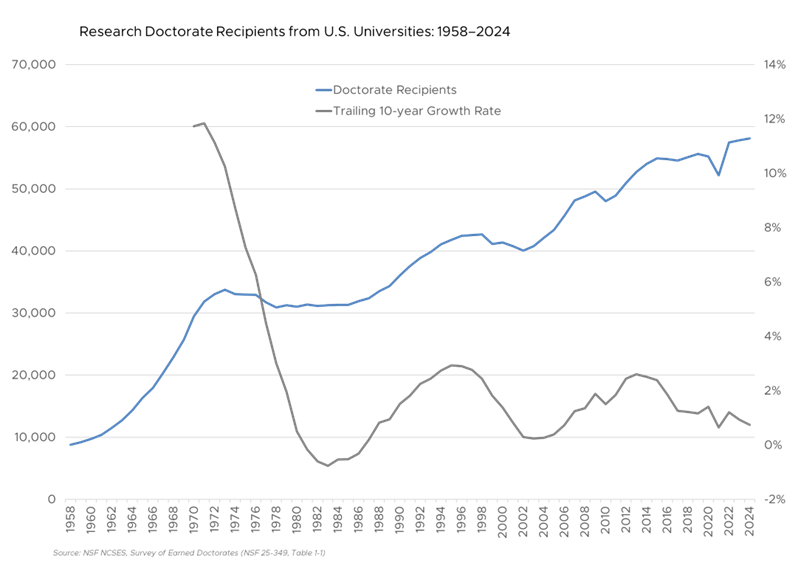

This creates perverse incentives during financial stress. Rather than eliminating undersubscribed programs in declining fields — like certain humanities disciplines — administrators cut support staff, reduce course offerings, increase class sizes, and slash PhD enrollments. These are all measures that degrade educational quality while preserving tenured positions in potentially obsolete specializations. Recognizing the operational inflexibility, universities have reduced the share of tenured positions by half over the last 50 years. Accordingly, the tenure-track pipeline is beginning to shrink, as research doctorate production (excluding medical and legal fields) declines.

Curriculum Inertia and Market Misalignment

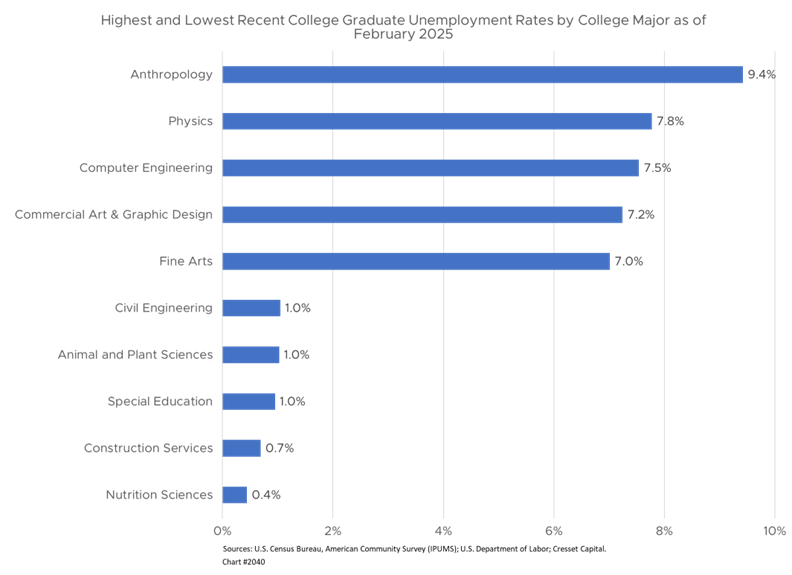

The tenure system allows faculty to maintain courses and research agendas that can drift from labor market demands. As a result, universities continue graduating students in fields with weak employment prospects, in part because tenured faculty cannot be easily redeployed or replaced.

Palantir CEO Alex Karp has argued that college often fails to prepare students for the working world — an outcome that reflects a professoriate partly insulated from market feedback. Employers increasingly prioritize graduates who can adapt quickly, yet tenure structures reward professors who replicate their own training from decades earlier. The result is curricular ossification just as artificial intelligence (AI) and rapid technological change demand greater dynamism.

Resistance to Alternative Educational Models

Tenured faculty have institutional incentives to resist innovations threatening their position. The growth of online education, competency-based learning, vocational integration, and industry partnerships all potentially reduce demand for traditional residential instruction by tenured professors. Faculty senates — dominated by tenured members — often block or slow administrative attempts to expand these alternatives. Rather than repurposing tenured faculty toward emerging educational needs, universities are forced to build entirely separate structures because tenured professors cannot be compelled to teach outside their specializations or adapt their pedagogical approaches.

Some institutions are experimenting with post-tenure review, performance-based compensation within tenure, and administrative reorganizations that reduce departmental autonomy. But these reforms face fierce resistance and legal challenges. Until universities can meaningfully adjust their tenured workforce in response to enrollment shifts, technological change, and evolving labor market demands, they will struggle to demonstrate value proposition improvements necessary to restore public confidence.

The Cost of Cutting Costs

Faced with these constraints, administrations have turned to sweeping austerity measures. Over 12,000 university job cuts were announced in the past year, with Columbia eliminating 180 positions and Duke offering employee buyouts. Elite institutions are reducing PhD enrollments; Princeton’s economics department dropped from 23 to 20 students, directly reducing teaching capacity for undergraduates.

Meanwhile, capital projects face suspension or cancellation. Research facilities sit unbuilt. Harvard committed $250 million of its own funds to backstop frozen federal research dollars, a Band-Aid solution that is unsustainable long-term. Yale’s provost identified the excise tax as “the most significant challenge” facing the university, noting it forces “substantial reduction in funds available to support students, faculty, staff, and local partnerships.”

The quality degradation is measurable. Larger class sizes, fewer teaching assistants, reduced course offerings, and postponed facility improvements all diminish the educational product precisely when value perception is collapsing. This creates a vicious cycle: as quality declines, public skepticism about worth intensifies, justifying further funding pressures.

An Existential Question: What Is College Worth?

Colleges are under pressure to demonstrate measurable value. Proposals to condition maximum tuition on graduate outcomes threaten institutions with poor performance metrics. Recent studies suggest that many freshmen lack rudimentary math skills, despite having graduated high school in advanced courses. This exposes systemic credibility problems extending beyond universities to K-12 partners.

The rise of AI presents an existential challenge for traditional education models. If entry-level white-collar jobs disappear to automation, what value do liberal arts degrees provide? Meanwhile, skilled trades offer immediate employment at competitive wages without debt burdens, making vocational alternatives increasingly attractive.

Some institutions are exploring mergers to achieve scale, while others expand online and certificate programs to tap non-traditional learners. But the central issue remains unresolved: the four-year residential model, historically the sector’s profit engine, is under pressure from weakening demand and limited pricing power.

A Sector Under Pressure, Not in Collapse

The municipal education sector faces meaningful headwinds, with both Moody’s Investors Service and S&P Global Ratings maintaining negative outlooks. However, the investment implications require selection, while not a blanket sell signal, but rather a call for heightened selectivity.

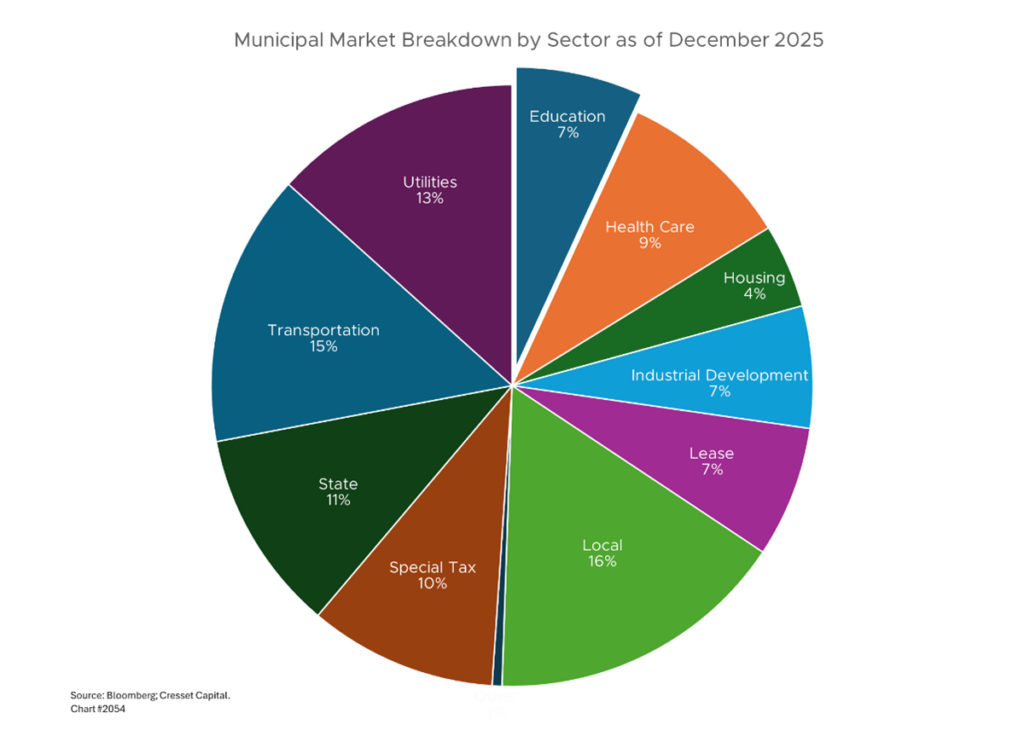

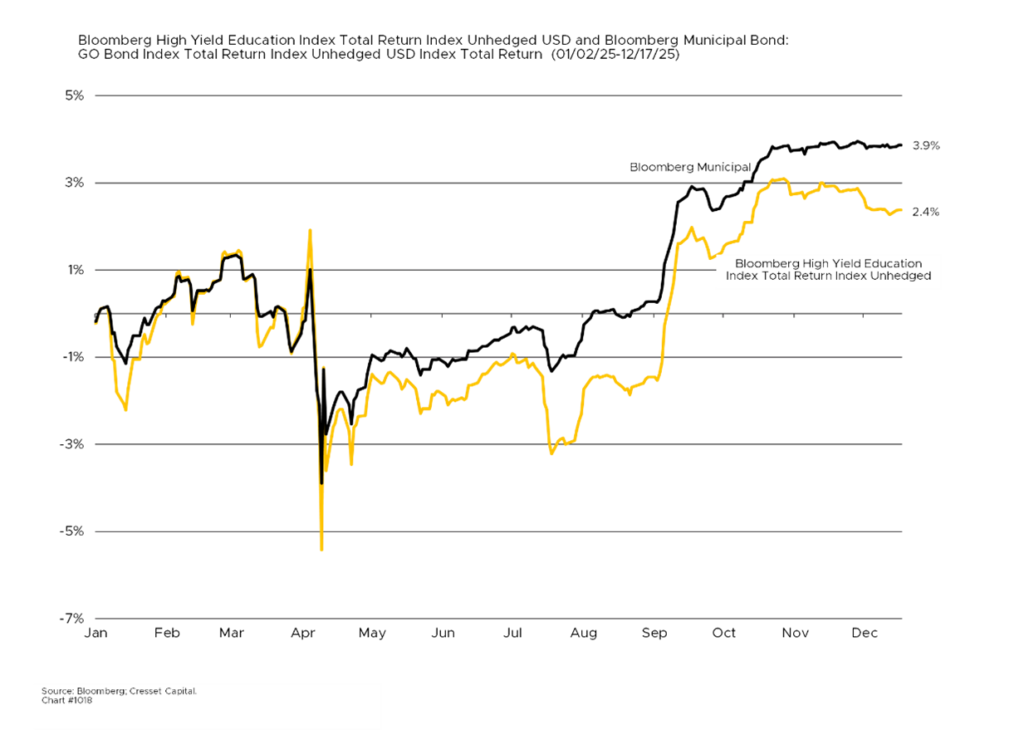

The higher education crisis presents significant risks for municipal bond investors. College and university debt comprises about seven percent of the education bonds market, which already underperformed broader municipal indices this year. Several factors heighten credit concerns:

Sector-Wide Weakness: Last year, Moody’s lowered its outlook for U.S. higher education to negative, citing “a more difficult operating environment” from federal policy changes. High-yield educational bonds have particularly lagged, with BBB and below-investment-grade spreads widening as fundamentals deteriorate.

Bifurcated Performance: Well-rated public universities with diversified funding sources and strong regional demand should weather challenges better than lower-rated private institutions dependent on tuition revenue and vulnerable to demographic pressures. This quality bifurcation will likely intensify, with credit spreads widening between strong and weak issuers.

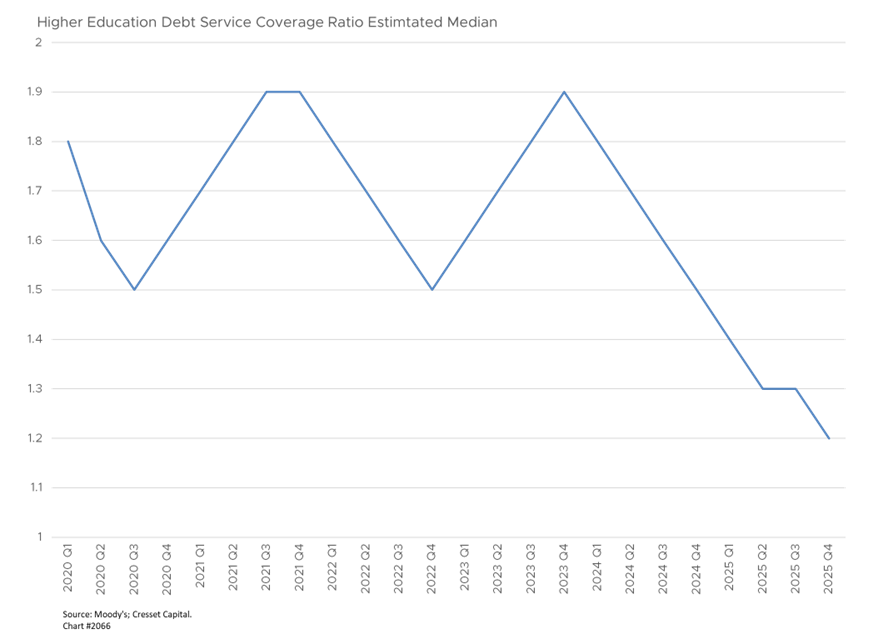

Revenue Vulnerability: With enrollment declining, federal funding uncertain, and tuition pricing constrained by public skepticism, many institutions face structural revenue challenges that neither their endowment returns nor spending cuts can fully offset. Debt service coverage ratios are deteriorating for the entire sector with intense pressure on the weaker credits.

Political Risk Premium: The Trump administration’s weaponization of federal funding and threats to tax-exempt status introduce unprecedented political risk into higher education credits. While wholesale elimination of tax exemption remains unlikely, “adjustments on the margins” could negatively impact valuations.

Universities with particularly rigid tenure policies, powerful faculty representation, and large proportions of tenured faculty in declining disciplines represent heightened credit risk. These structural inflexibilities limit management’s capacity to address revenue shortfalls through cost optimization, making financial recovery more dependent on external revenue growth that current trends suggest may not materialize.

Margins Under Pressure

Moody’s forecasts 3.5% revenue growth against 4.4% expense growth, putting pressure on margins across most institutions. The demographic cliff, a shrinking population of high school graduates, will intensify competition for students, particularly affecting regional institutions with weaker brands. This fundamental imbalance suggests investors should demand wider spreads for lower-rated education credits than historical norms would suggest.

A bifurcated market is developing between those colleges and universities with large endowments and smaller, regional schools that rely on state and local allotments. Those schools face credit risks due to reduced state appropriations and tuition revenue, which can limit their operating budgets and ability to meet debt service obligations. Lower-rated issuers carry higher credit risk and a greater likelihood of default; in periods of financial stress, both bond values and payment reliability can deteriorate significantly.

American public schools issued about $82 billion in municipal bonds in 2025, a nearly 42% jump from 2024 and the most since at least 2013, as dipping enrollment and elevated inflation strain districts’ budgets. Governmental policies and funding are subject to change, and potential federal actions such as regulatory changes or reduced funding for financial aid programs could negatively impact an institution’s finances and its ability to pay debt service.

Policy Risk Cuts Both Ways

Federal policy represents perhaps the most significant variable. Caps on Grad PLUS and Parent PLUS loans will pressure institutions heavily dependent on graduate programs, while research-intensive universities face uncertainty around NIH funding and indirect cost reimbursements. Meanwhile, the expanded endowment tax, while affecting only the wealthiest institutions, signals a policy environment that views elite universities as revenue sources rather than protected entities.

Critically, these policy risks disproportionately affect institutions at opposite ends of the credit spectrum. Elite private universities face endowment taxes and research funding uncertainty, while lower-rated institutions serving low-income students lose TRIO program funding. The middle tier, strong regional publics and well-positioned private universities, may face relatively less direct policy pressure.

Strong investment returns through 2025 have bolstered balance sheets across the sector, with total cash and investments providing roughly 3x coverage of operating expenses for private universities. This accumulated wealth offers meaningful cushion, even as operating margins compress. For investors, this suggests that temporary operating weakness may not immediately translate into credit deterioration for well-capitalized institutions.

Quality Still Matters Most

Higher education institutions rated A or higher generally possess the resources, brand strength, and fundraising capabilities to navigate current challenges. Their large balance sheets and robust demand profiles create resilience that lower-rated peers lack.

As the newly minted graduates flip their tassels from right to left, I would conclude my remarks by telling the administration that even those schools that are fortunate enough to enjoy large endowments and selective enrollments can’t afford to rest on their laurels. All schools must adapt to the emerging reality.

Bottom Line

Given higher education’s relatively small share of the municipal bond market, our cautious view of the sector does not alter our broader outlook. However, within the sector, we favor quality over yield. The spread pickup for moving down the credit spectrum doesn’t adequately compensate for the elevated risks facing smaller, less selective institutions, particularly those in remote locations.

Moreover, public universities with strong state support may offer better risk-adjusted returns than similarly rated private institutions, given the additional revenue diversification from appropriations.

Lastly, institutions with academic medical centers warrant careful analysis. Patient care revenues provide diversification, but Medicaid changes in 2027 and beyond create longer-term uncertainty.

The higher education sector faces legitimate challenges, but for selective investors focused on well-capitalized institutions with strong demand profiles, current valuations may offer reasonable entry points. The key is rigorous credit differentiation rather than sector-wide positioning.