Key Observations

- Energy disruptions are broadening beyond oil into natural gas, amplifying global economic risk

- A prolonged shock could materially reduce global growth and increase recession probabilities

- Regional exposure is uneven, with Japan, Europe, and China particularly vulnerable

- Markets are already repricing risk through dollar strength and weaker emerging markets

- Bond markets reflect classic inflation shock dynamics with flattening yield curves

- Long-term investment leadership, particularly U.S. technology, remains structurally intact

The current standoff between Washington and Tehran has settled into a war of economic attrition, and investors should prepare for the possibility that this dynamic persists well beyond what markets are currently pricing. Direct diplomacy is frozen, both sides are relying on economic pressure and coercive leverage to force the other’s hand, and the stalemate could endure until one side yields. The investment implications run far deeper than the headline oil price.

Energy Shockwaves Extend Beyond Oil

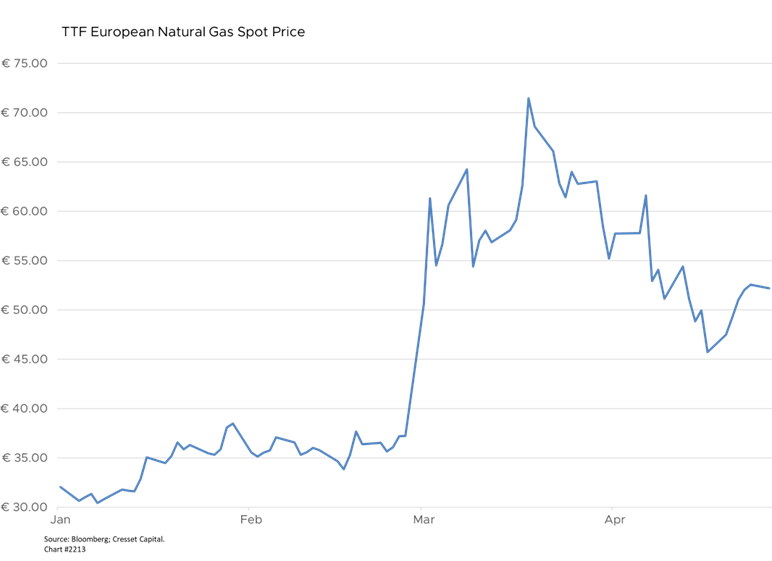

The investment implications radiate outward from energy. The current supply disruption has pushed Brent crude, an international energy benchmark, to $107 per barrel. Analysts estimate a three-month outage could push Brent far higher. The energy crisis extends beyond crude. European Title Transfer Facility (TTF) natural gas prices are projected to average €50 per megawatt-hour under a two-week disruption, and could reach €108 under prolonged outages, with monthly highs near €115 — levels that would force outright demand destruction given the absence of equivalent strategic gas reserves.

Macro Consequences: Growth, Inflation, and Recession Risk

The global macroeconomic consequences would be severe. Analysts suggest an extended disruption could strip 140 basis points from global growth, while even a two-month interruption could inflict nearly a half-percentage point hit. Oil prices rising toward $150 per barrel would materially increase U.S. recession risks, as higher energy costs and tighter financial conditions compound existing growth headwinds.

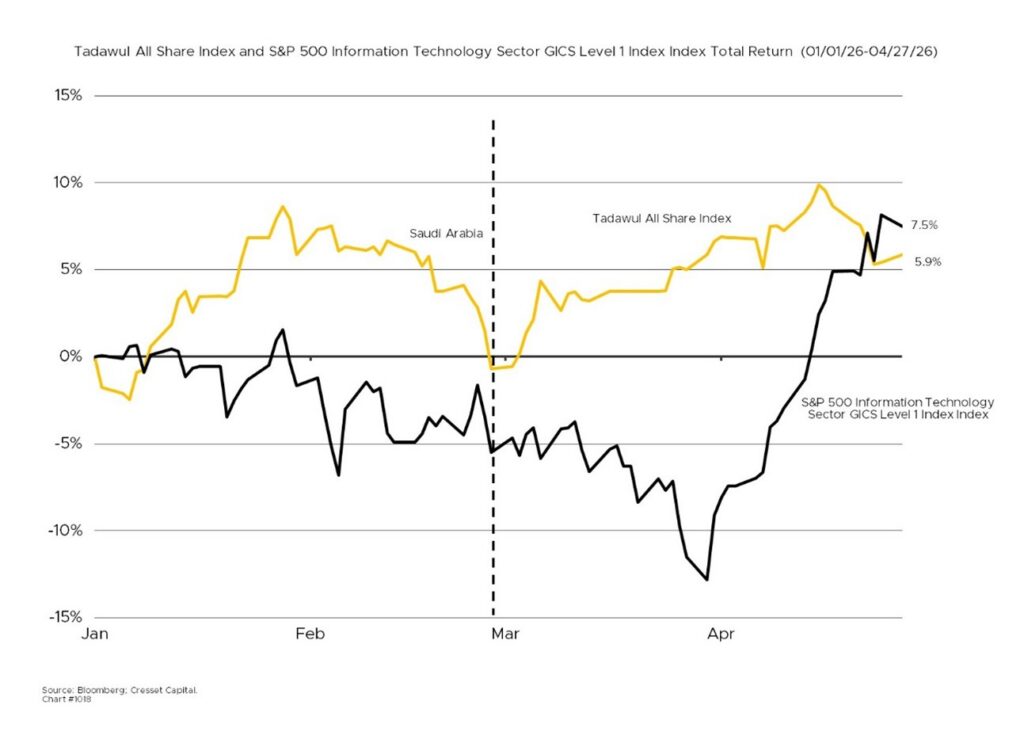

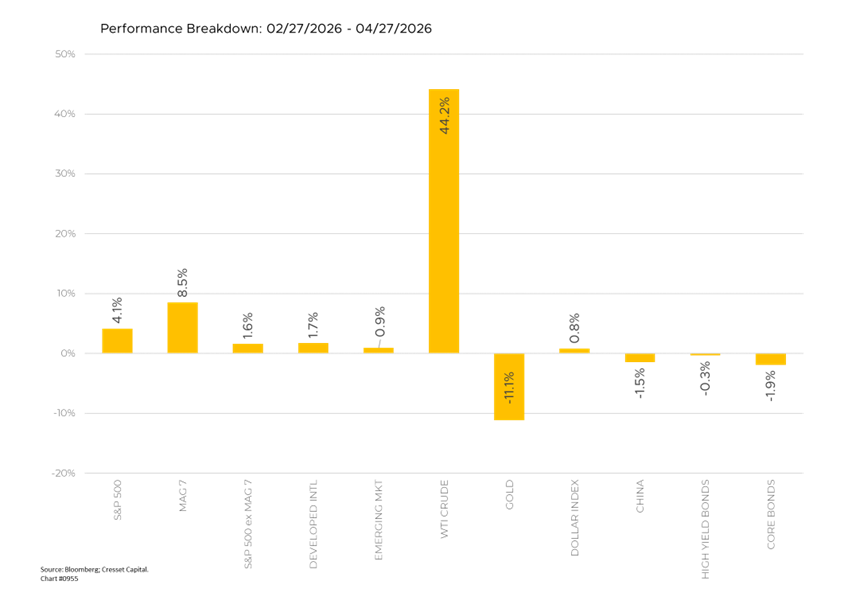

Historically, a 10% increase in oil prices is expected to reduce global growth by 0.15%, while raising global inflation by 0.4%. The market preview came in early March, when the initial conflict triggered a risk-off move that sent global equities down nearly 7% and reordered market leadership, with energy exporters like Saudi Arabia and Colombia outperforming the technology stocks.

Regional Fault Lines in a Global Shock

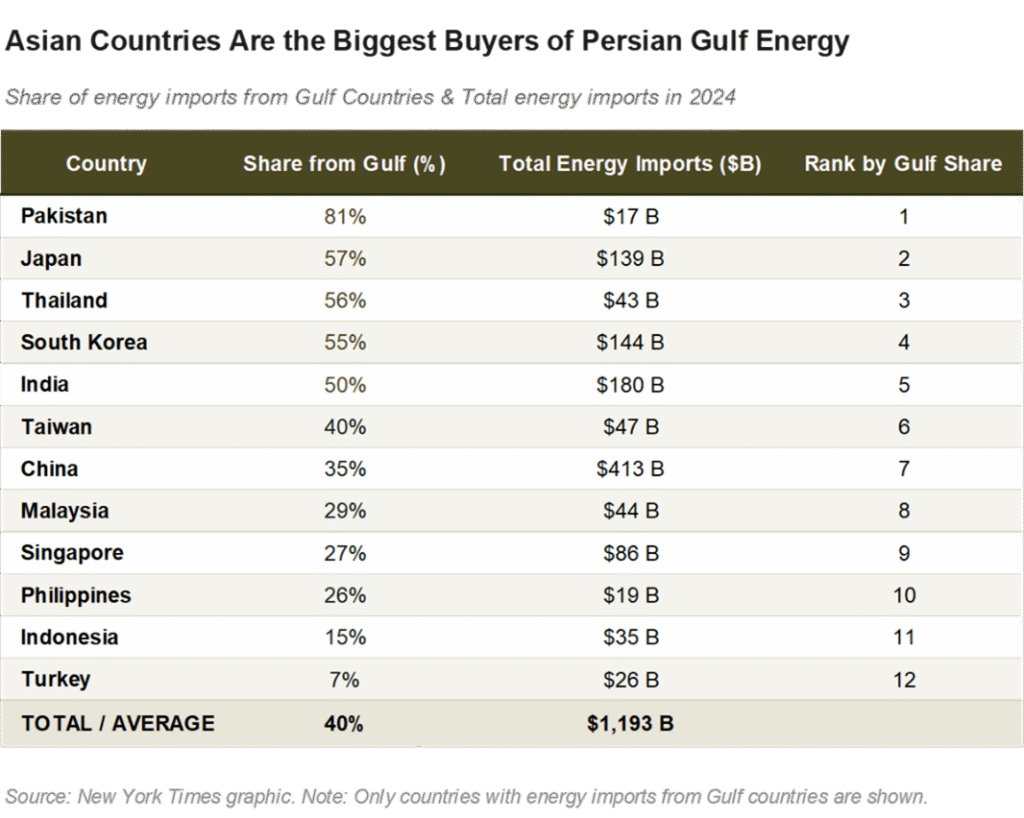

Regional vulnerabilities vary dramatically, although Japan stands out. The world’s fourth-largest economy derives nearly 60% of its oil imports from the Persian Gulf. Analysts estimate that an extended disruption could reduce Japan’s real GDP growth by 0.9 percentage points in 2026 and 0.7 in 2027, while pushing core CPI to 2.7% in 2026 and 3.3% in 2027, levels that could force the Bank of Japan back to zero rates and aggressive fiscal expansion.

Meanwhile, China’s export-driven economy carries serious risks, since Asia, China’s primary export destination, absorbs the most direct effects through energy and food prices, transportation disruption, and tighter financial conditions. Europe could also confront both inflation and growth risks that could push the region into outright stagflation. In the United States, prolonged conflict argues for persistent inflation alongside a meaningful growth slowdown, potentially prompting the Federal Reserve to cut rates even as inflation runs above target. Latin America faces weaker growth, higher inflation, and currency depreciation.

Market Repricing and Capital Rotation

The investment landscape has shifted during the hostilities. The dollar emerged as principal beneficiary of rising risk aversion, appreciating significantly as capital rotated toward dollar-denominated assets. Emerging-market equities and currencies weakened, with energy importers hit hardest. Global bond markets reflected inflation risk consistent with classic shock models, with curves flattening as two-year yields rise more than ten-year yields. A prolonged stalemate or broader conflict would mean higher risk premiums and lower market valuations across the board.

Bottom Line

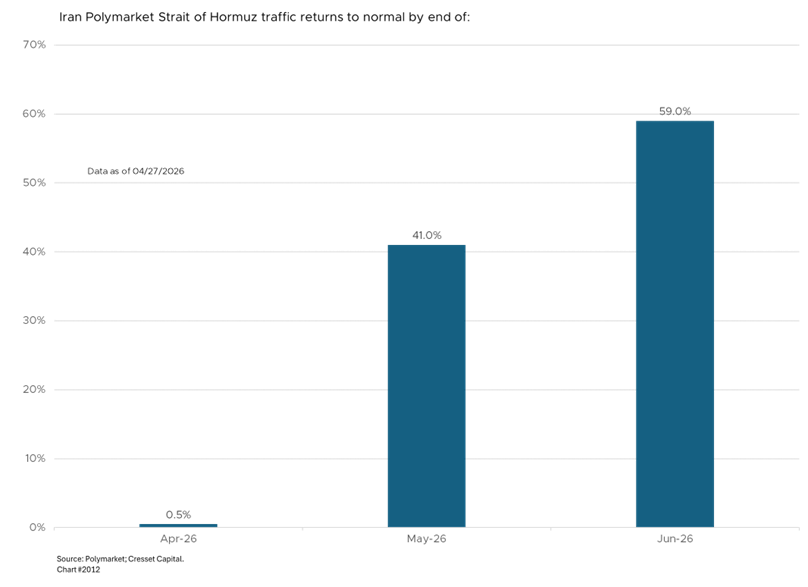

We acknowledge that a sustained closure of the strait would be a significant hurdle for the global economy. Long-term investors should resist the urge to reposition portfolios around what is fundamentally a contrived crisis. Both sides have strong economic incentives to find an off-ramp. Iran’s economy is buckling under the blockade, with food prices tripling, more than a million jobs lost, and inflation approaching 70%. The United States faces rising gasoline prices and political pressure ahead of the midterms. These conditions argue for resolution measured in months rather than years, and history suggests markets recover quickly once supply concerns ease. The 1956 Suez Crisis saw oil prices double and equities fall sharply, only to rebound to new highs once the canal reopened. A negotiated breakthrough would likely compress oil’s risk premium by $10 to $15 per barrel and trigger an immediate rotation back into previous leaders.

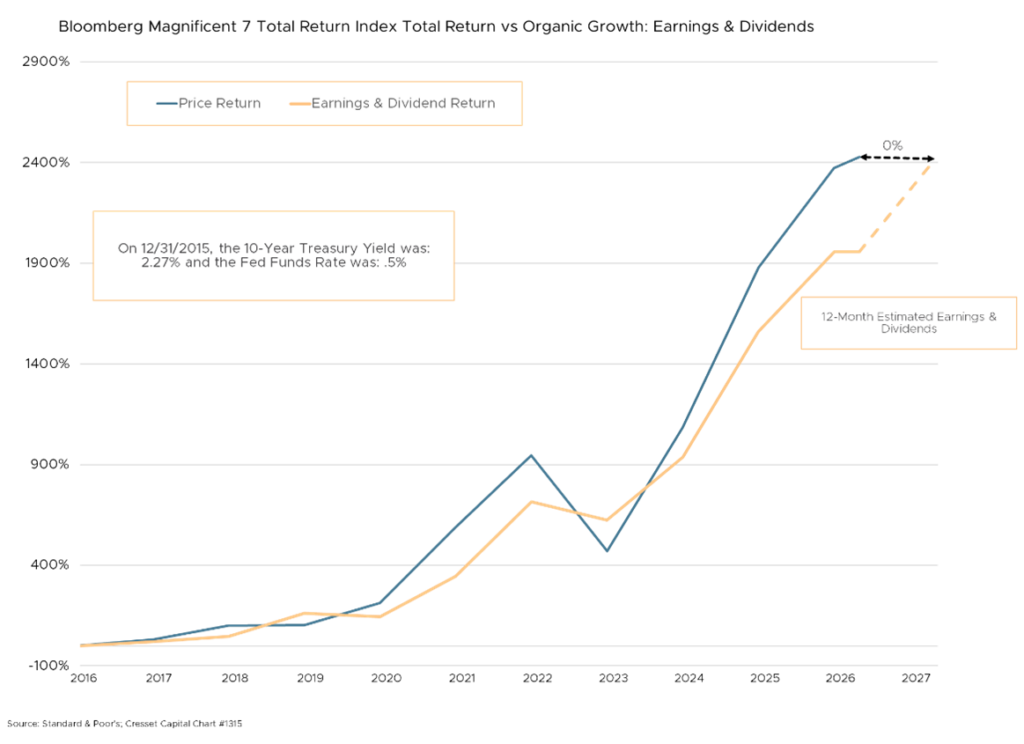

More importantly, U.S. technology remains structurally insulated from these global crosscurrents. The hyperscalers generate enormous free cash flow from domestic and global digital infrastructure spending that does not depend on the price of crude oil or the patency of the Strait of Hormuz. Their AI capital expenditure cycle is funded internally and continues to compound earnings power across the cohort. On forward earnings expectations, the hyperscalers are relatively cheap, with price-to-earnings multiples that look reasonable against projected earnings growth, particularly when measured against the broader market and against their own history. Investors who panicked out of technology during the March selloff have already missed a meaningful recovery, and those who remain underweight should reconsider rather than chase the energy trade at what may prove to be peak crisis pricing.

The disciplined approach is to stay the course: maintain strategic allocations across asset classes, hold core technology exposure, and resist the temptation to make outsized bets on a geopolitical outcome that is genuinely unknown. Geopolitical shocks are typically short-lived for most asset classes, and there is little reason to believe this episode will prove the exception. The portfolios that perform best will likely be those that remain invested rather than those that traded the headlines.