Key Observations

- Energy drove markets as oil surged following the Strait of Hormuz closure.

- Equities fell but held up better than expected, given the shock.

- Economic growth slowed as labor markets weakened and inflation persisted.

- Rate cut expectations faded as inflation remained elevated.

- Market leadership narrowed, led by a sharp rally in energy stocks.

- Private markets diverged, with strength in large deals and weakness in smaller transactions.

The first quarter of 2026 was supposed to be the year markets broadened. Economic growth was accelerating into year-end 2025, the Federal Reserve was ready to cut rates, and the tariff overhang had largely dissipated following the Supreme Court’s February ruling striking down much of the Trump administration’s trade duties. The setup for an expansion beyond Big Tech and mega-cap artificial intelligence (AI) names looked as good as it had in years.

Then came Iran.

On February 28, the United States and Israel launched a series of strikes on Iran. Within weeks, the Strait of Hormuz, which had handled roughly a fifth of global energy flows, was effectively closed. The investment landscape that greeted January gave way to something far more complicated.

Economic Resilience Faces Growing Strains

The U.S. economy navigated a challenging first quarter in 2026, marked by decelerating growth, labor market turbulence, and persistent inflationary pressures that were further complicated by geopolitical shocks. While the economy continued to expand, the quarter revealed underlying fragility that raised questions about the sustainability of the recovery and the Federal Reserve’s policy path.

Economic growth lost momentum as the quarter progressed. The fourth quarter of 2025 closed the year with GDP expanding at just 1.4% on an annualized basis, well below the 4.4% pace of the prior quarter and missing economists’ forecasts. Early estimates for Q1 2026 suggest growth could rebound to around 2.4% on an annualized basis, subject to revision given the evolving geopolitical landscape.

A Volatile Labor Market Takes Shape

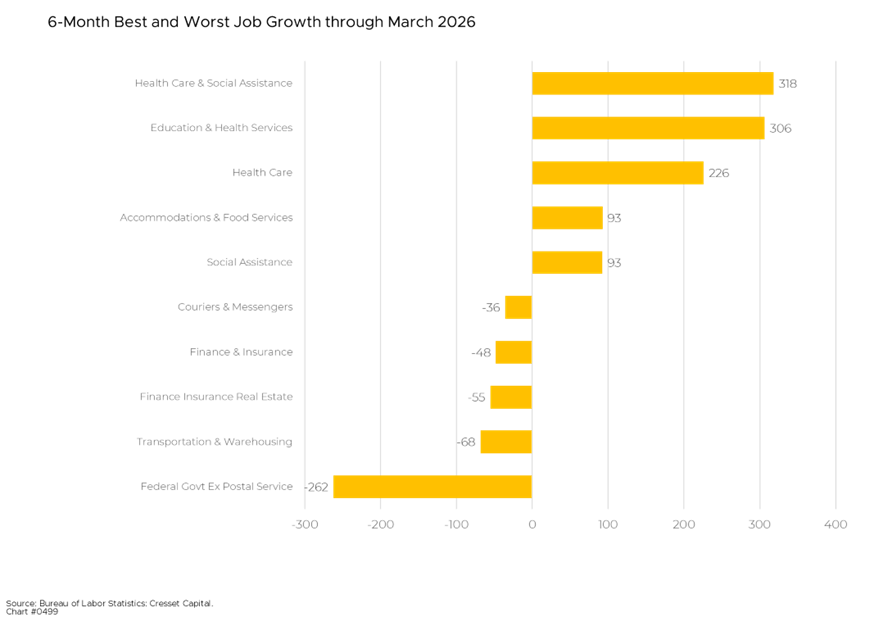

The U.S. labor market in 2026 has been characterized by weakness and volatility, alternating between job gains and losses while generating minimal net employment growth. After adding just 50,000 jobs in December 2025, the market deteriorated sharply in February, with employers cutting 92,000 positions, one of the largest declines since the pandemic. Meanwhile, the economy added 178,000 jobs in March, the best monthly total in more than a year and well ahead of expectations. The unemployment rate ticked down to 4.3% even though the labor force shrank by nearly 400,000 people, pulling the participation rate to 61.9%, its lowest level since fall 2021. Beyond healthcare and social assistance hiring, private sector job growth has been anemic, with ADP reporting only 22,000 new jobs in January and 63,000 in February, well below historical norms.

The unemployment rate, at 4.3% through the first quarter, could rise incrementally to 4.5% for the full year. Federal Reserve officials have noted that the labor market stabilized in the second half of 2025 into early 2026, but payroll gains have been “pretty weak,” leaving policymakers feeling “uncomfortable” about the trajectory.

Despite the weak hiring environment, layoffs have remained surprisingly low. Initial jobless claims fell to 202,000 in late March, near a two-year low, suggesting employers are reluctant to cut workers even as they refrain from adding new positions. However, technology sector job cuts have accelerated, with over 52,000 announced in the first quarter as AI adoption drives leaner staffing. The combination of minimal job creation and low layoffs has created what observers call an unprecedented “jobless boom,” an economy generating wealth without meaningful employment opportunities.

Inflation Keeps the Fed on Edge

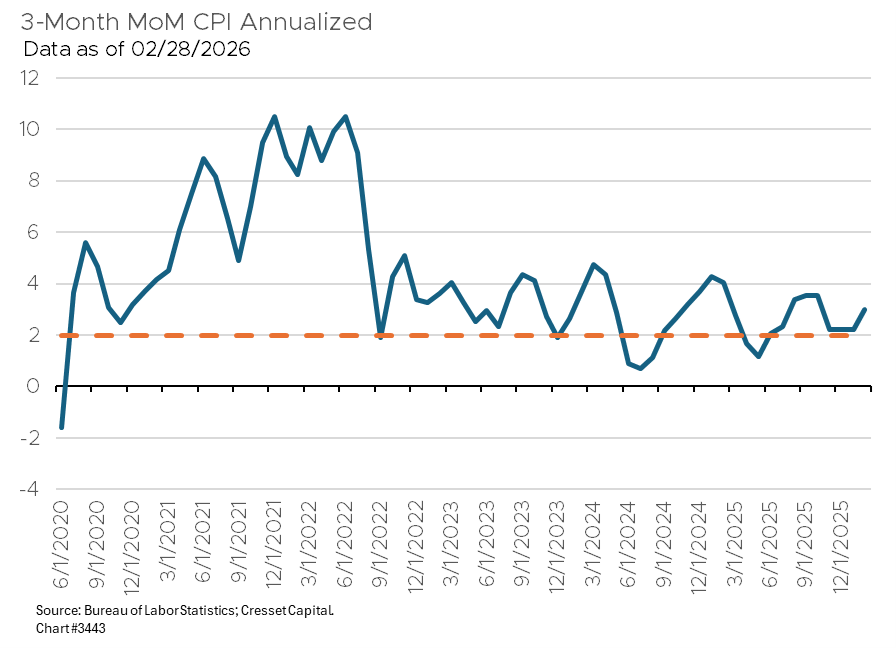

Inflation remained stubbornly elevated throughout the quarter, complicating the Federal Reserve’s policy calculus. The core personal consumption expenditures price index, the Fed’s preferred inflation gauge, rose a firm 0.4% in January, suggesting underlying price pressures remained entrenched. Wholesale inflation accelerated unexpectedly in February, with the producer price index rising 0.7% month-over-month, well above the 0.3% forecast, reflecting higher costs for both goods and services. On a year-over-year basis, headline CPI stood at approximately 2.7% as of the end of 2025, with estimates for the first quarter suggesting inflation would remain near that level. These persistent price pressures occurred even before the outbreak of war with Iran in late February, which triggered significant supply chain disruptions and energy market volatility that threatened to push inflation higher.

Consumers Turn More Cautious

Consumer spending, the primary engine of U.S. economic growth, exhibited tepid enthusiasm last quarter. Real consumer spending increased just 0.1% in January, barely advancing after the weak fourth quarter GDP. Retail sales painted a similarly lackluster picture, declining 0.1% in January before rebounding 0.6% in February, suggesting consumers remained cautious amid economic uncertainty. Industrial production showed modest year-over-year growth of 2.3% in January and 1.4% in February, indicating manufacturing activity remained subdued.

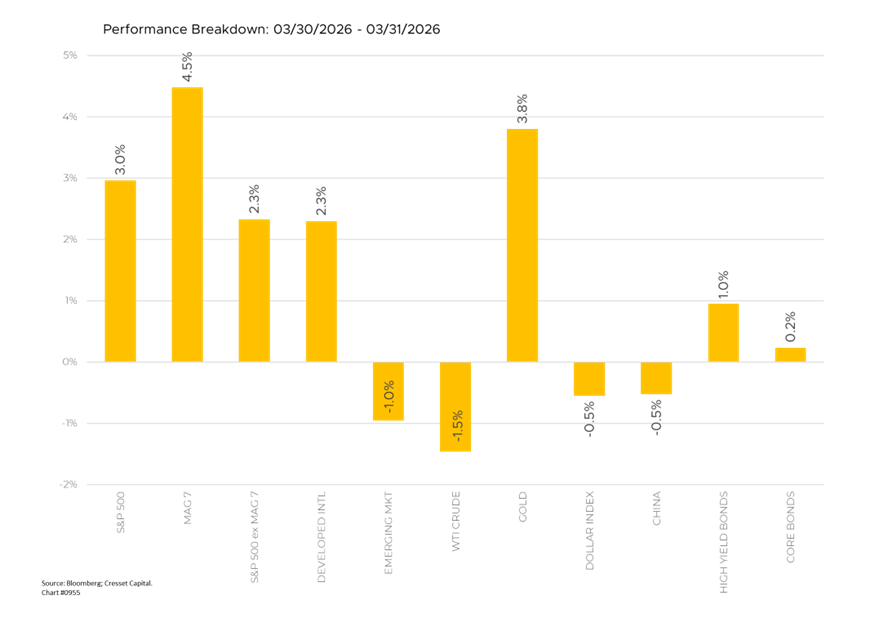

Stocks: The Worst Quarter in Four Years

U.S. equity markets recorded their worst quarterly performance since the second quarter of 2022. The S&P 500 fell 4.4% for the quarter, with most of the damage concentrated in March. The Dow Jones Industrial Average slid 3.2%, while the Nasdaq Composite dropped 7.0%. Both the Dow and the Nasdaq entered correction territory in March, meaning each fell more than 10% from a recent high. The S&P 500 ended the quarter 3.8 percentage points shy of that threshold.

In March alone, the Dow suffered its steepest monthly decline since September 2022. The S&P 500 dropped 5.1% for the month. These are not catastrophic numbers in isolation. However, in the context of a war that shut down one of the world’s most important shipping lanes, they were surprisingly restrained.

The quarter did deliver a broadening of sorts, just not the kind we expected. Ten of the S&P 500’s eleven sectors fell in March, by an average of 6.2%. Energy was the lone stand-out. The sector surged 34% for the quarter, its best quarterly performance in four years. Oil and gas names dominated the list of top S&P 500 performers. By mid-March, most of the index’s best-performing stocks were direct beneficiaries of the energy squeeze. The quarter ended on a hopeful note with all three U.S. equity indexes posting their best single-day gains of 2026.

Energy Shock Reverberates Across Markets

U.S. crude oil futures surged 77% in the first quarter to $101.38 per barrel, representing their largest quarterly percentage gain since the second quarter of 2020, when prices collapsed and then rebounded sharply from negative territory. International crude, as measured by Brent futures, rose 95% to $118.35, the largest quarterly gain since 1990, coinciding with Iraq’s invasion of Kuwait. Wholesale gasoline prices rose 60% in March alone, the biggest monthly gain on record, pushing the national average for regular unleaded gasoline ended the quarter at $4.02, the highest level since August 2022.

Expectations for Fed easing this year took an abrupt about-face. Before the conflict, traders were assigning an 80% probability to two Fed rate cuts by the end of the year. By quarter-end, those odds had collapsed to less than 5%. The prospect of sustained $100-plus oil undermined the case for easier monetary policy, and bond markets responded accordingly. The 2-year Treasury yield rose to 3.799%, higher than the Fed Funds rate for the first time since 2022, the year Powell & Company ratcheted up rates by more than 3 percentage points. For investors who expected their bond portfolios to cushion equity losses, the correlation provided little comfort.

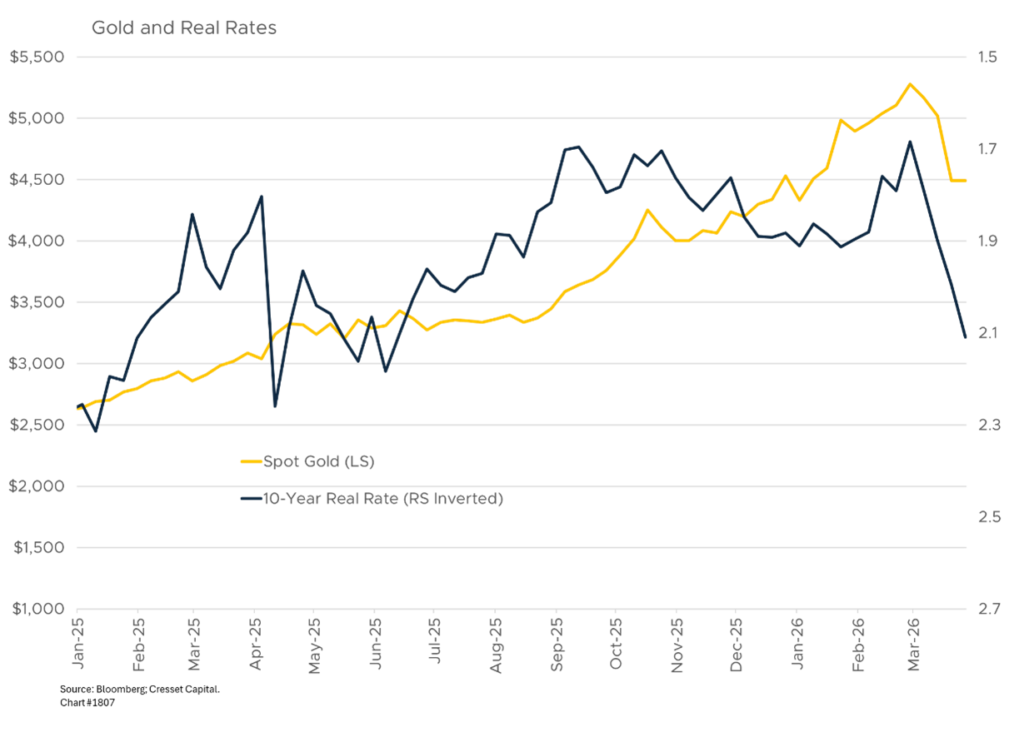

Gold Falters as the Dollar Strengthens

Is gold a risk asset or a safe haven? For the full quarter, gold gained 7.4% to $4,647.60 per troy ounce, extending a winning streak to five consecutive quarters and cumulative gains of nearly 77% over that stretch. Investors seeking an inflation hedge found it early in the period.

Once hostilities broke out, gold told a different story. The precious metal shed 11% in March, its largest monthly decline since 2013. Silver fell more than 19%, the biggest monthly drop since 2011. When oil prices surged, investors likely sold precious metals to cover margin calls and fund energy positions. Meanwhile, India and China, gold’s biggest price-insensitive buyers, put their buying spree on hold against a backdrop of high energy prices. Half of India’s crude oil imports come from the Persian Gulf. For China, it’s about a third.

The U.S. dollar strengthened considerably, posting its largest quarterly gain since the third quarter of 2025, extending its winning streak to three consecutive quarters. The dollar’s gains were fueled by the U.S.’s position as a net oil exporter, which boosts America’s fundamentals relative to the developed world. The euro fell 1.7% against the dollar, its largest quarterly decline since the fourth quarter of 2024.

Private Markets Split Between Opportunity and Constraint

The first quarter of 2026 revealed a private markets landscape marked by cautious momentum and sharp bifurcation. While certain sectors attracted substantial capital, the broader environment remained constrained by fundraising pressures, liquidity concerns, and defensive deal flow. Market participants navigated an uneasy balance between pockets of optimism, particularly in artificial intelligence, defense technology, and infrastructure, and persistent challenges around exit visibility, valuation gaps, and capital distribution.

Private credit faced mounting scrutiny as redemption pressure intensified, forcing many funds to maintain caps or gates on withdrawals and potentially prompting asset sales rather than new loan origination.

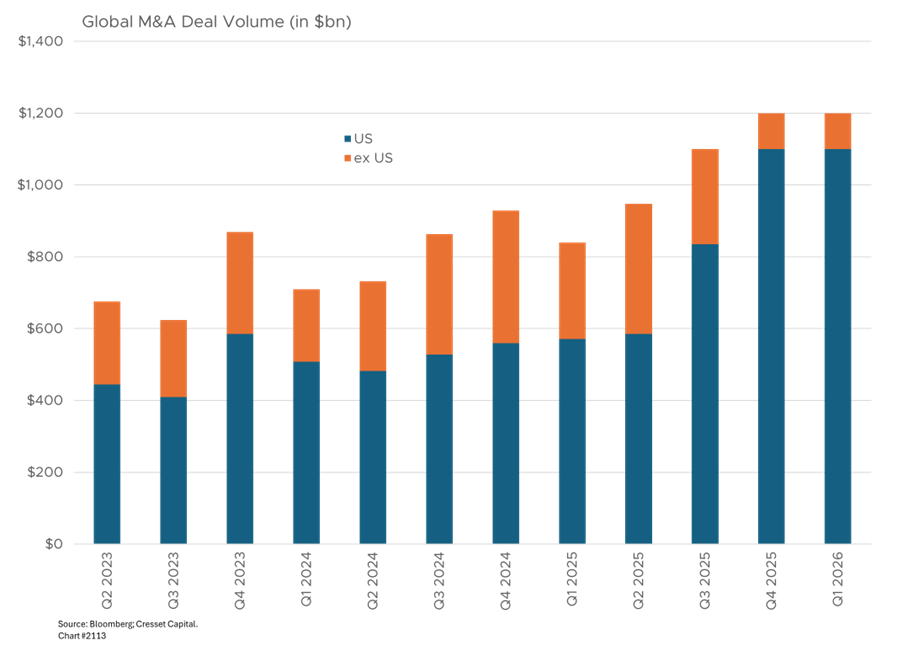

Mega Deals Drive M&A to Record Start in 2026

Corporate dealmakers flexed their muscles. The first quarter of 2026 recorded 22 transactions valued at $10 billion or more globally, the highest quarterly total ever, surpassing the previous record of 21 such deals in the fourth quarter of 2015. Total global mergers and acquisitions (M&A) volume reached $1.2 trillion, making it the third consecutive $1 trillion quarter for dealmaking.

Notwithstanding deal activity, CEOs acknowledged they were less optimistic than they had been a few months earlier. Nonetheless, the regulatory environment remains conducive, boosting the strategic landscape of large transactions regardless of where oil was trading. Smaller deals were a different story. Activity below $5 billion fell in both deal count and total value, as buyers chose caution and private equity firms resisted selling at depressed prices. The number of private equity-backed deals fell 12%, to a six-year low by deal count, according to the Financial Times.

Looking Ahead: What’s Next in Q2?

The quarter ended with energy prices driving virtually every asset class. As we enter the second quarter, risk markets will have a difficult time advancing as long as energy prices remain high. Investors need clearer visibility on the Strait of Hormuz and Iran more generally.

On a positive note, analysts are still projecting a sixth consecutive quarter of double-digit earnings growth for S&P 500 companies. We expect their projections assume that the conflict is relatively short-lived and Iranian reintegration into the global energy market would lower, or at least stabilize, energy prices. The persistence of $100-plus per barrel oil increases the likelihood of a global recession.

We should appreciate the market’s resilience. Investor selling has slowed and earnings estimates have held. The S&P 500 entered the quarter near all-time highs and finished down less than 5% despite a genuine geopolitical shock. That suggests the underlying demand for global risk assets has not dissipated.

Bottom Line

The path forward hinges on how long the Strait of Hormuz remains functionally closed. A negotiated resolution opens the door to lower oil prices, revived rate-cut expectations, and a resumption of the broadening trade. A prolonged conflict pushes stagflation risk higher and compresses valuations further, particularly in rate-sensitive sectors.

We expect the U.S. administration and Iran will find a reason to de-escalate. The economic pressure on both sides is mounting, but base cases are not certainties. Portfolios should lean into quality across asset classes, however, the March 31 rally told us the market is ready to move quickly when it sees a credible off-ramp. The goal now is to be positioned for that moment without assuming its imminent arrival.