Key Observations

- Roughly 20% of global oil consumption flows through the Strait of Hormuz, making it a critical vulnerability.

- Supply disruptions are already pushing oil toward $120–$130, with limited rerouting capacity.

- Qatari LNG exports are highly exposed, with no viable pipeline alternatives.

- Non-energy trade, including fertilizers and metals, faces concentrated disruption risk.

- Rising freight, fuel, and insurance costs are resetting global supply chain economics.

- The shock increases the risk of stagflation, especially in energy-importing economies.

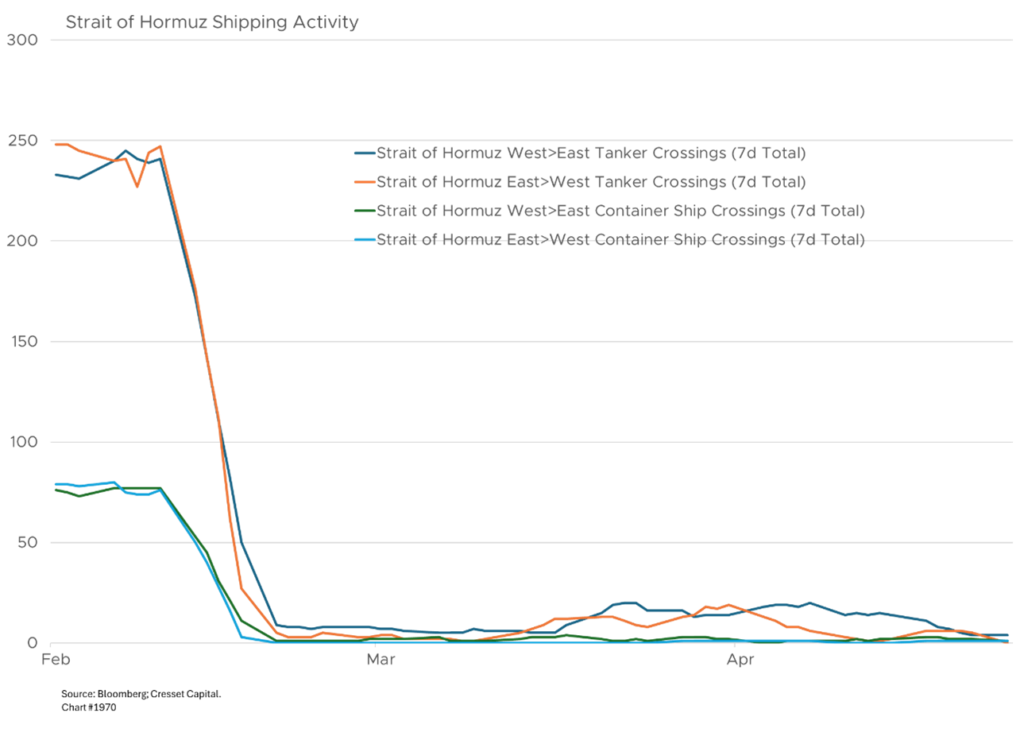

The Strait of Hormuz is a critical chokepoint in the global energy system. Roughly one-fifth of the world’s oil consumption and a comparable share of seaborne liquefied natural gas (LNG) move through a waterway that narrows to 21 miles. Before the current war, an average day saw about 21 million barrels of crude and refined product pass through the Strait, alongside Qatari and Emirati gas bound for Asia and Europe. An indefinite closure not only raises prices but reorders the flows that keep modern economies running.

Oil Markets Face Immediate Supply Shock

The first-order impact is on crude. With non-Iranian shipping largely halted since the war began, the International Energy Agency estimates Gulf supply has already dropped by roughly 13 million barrels per day, with inventory drawdowns masking the full picture. Brent climbed from about $68 in mid-February to a peak near $118 in late March, and analysts forecast $120 over the next three months. Under a prolonged closure scenario, $130 is a credible ceiling rather than a tail outcome.

The constraint is physical: only 6.5 million barrels per day of pipeline capacity exists as a workaround, with about two-thirds of regional crude unable to be diverted at all. Saudi Aramco has captured what it can, reporting a 25% jump in Q1 profit after shifting volumes onto its East-West Pipeline, but the system cannot scale.

LNG Disruption Threatens Global Gas Balance

LNG is the more delicate problem. Qatar alone routes nearly all of its 80 million tons of annual exports through the strait, and there is no pipeline alternative. A single Qatari tanker reached Pakistan recently, but observable traffic is otherwise at a standstill. Asian buyers face the most acute exposure, and European gas, having spent two years rebalancing away from Russia, loses a swing supplier at precisely the wrong moment. The U.S. has increased its LNG exports in recent years to fill some of the gap. Meanwhile, the price of jet fuel has risen roughly 150% in three weeks as refining throughput in the Gulf falls.

The Hidden Risk: Non-Energy Trade Exposure

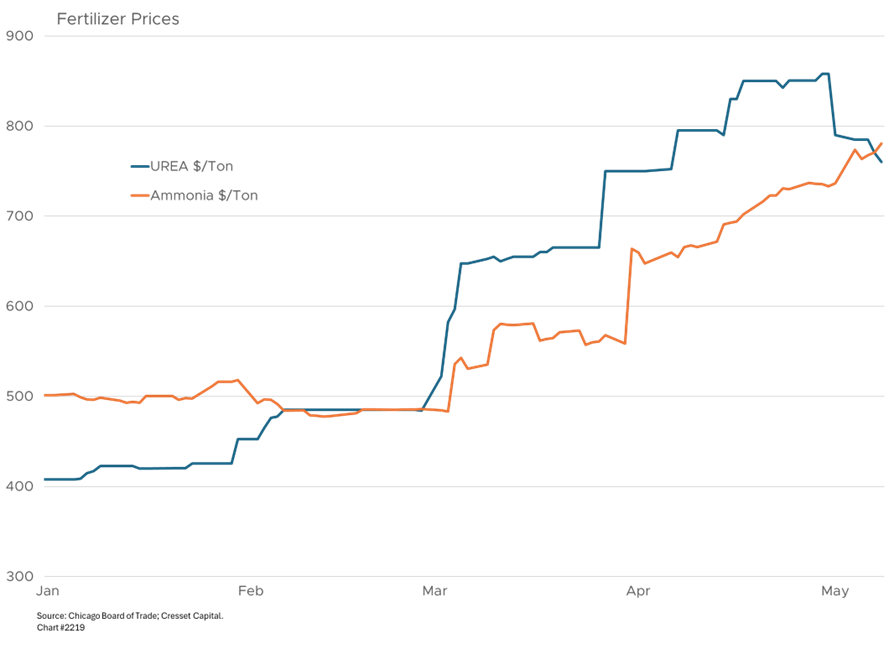

The second-order channel is non-energy trade, which is underappreciated. Approximately 2.4% of global non-energy trade crosses the strait, but the concentration matters more than the headline. Between 4% and 7% of the world’s imports of fertilizers, precious metals, aluminum, and cement move through these waters. Roughly one-third of globally traded urea, a fertilizer critical to Indian, Brazilian, and American agriculture, transits Hormuz. A sustained closure threatens not just energy CPI but food CPI, with a lag measured in growing seasons rather than weeks.

Shipping Costs and Supply Chains Under Pressure

Shipping economics are deteriorating in parallel. Freight on the Shanghai to Jebel Ali route is up 55% month-over-month, war-risk premiums have widened, and rerouted vessels are adding one to two weeks of transit and as much as $1 million per voyage. Lufthansa has warned that closure adds $2 billion to its fuel bill alone. These are not transient costs; they are the new baseline for any company whose supply chain touches the Gulf.

Inflation and Growth: A Fragile Balance

Analysts estimate that tightening energy markets could lift global inflation by roughly 70 basis points while shaving global growth by a smaller margin. Estimates from European banks suggests every $10 move in oil reduces GDP growth by 0.2 to 0.3 percentage points in the UK, Germany, and France, and by 0.4 points in Italy and Spain. India absorbs roughly $15 billion of additional import bill, equivalent to about 0.4% of GDP, for each $10 move. A prolonged three-month closure could trigger a global recession through demand destruction. Fuel demand is already down about 4 million barrels per day.

A sustained energy shock would simultaneously raise prices and slow activity, and it lands at a moment when consumer expectations are already fragile. The preliminary May sentiment reading from the University of Michigan fell to 48.2, a fresh low. The Fed’s Financial Stability Report placed geopolitical risk and the oil shock at the top of surveyed concerns. Global central banks face a terrifying tradeoff, as cutting rates into a supply shock could aggravate inflation while staying restrictive risks recession.

Corporate Margins and Earnings at Risk

Energy pass-through tends to hit corporate margins with a lag. We expect companies to fully absorb the impact of $120 crude, elevated jet fuel, and rerouted freight by Q3 2026. Transports, airlines, chemicals, packaged food, and industrials carrying long supply chains would be expected to lower guidance. With Q1 earnings growth tracking at 27.7%, that high bar could be subject to disappointment later this year.

Pricing power will be the dividing line. Companies with pricing power will preserve their profit margin, while companies without it won’t. The dispersion inside the S&P 500 widens, and the narrow leadership that drove the recent rally becomes a vulnerability rather than a strength.

Central Banks Confront a No-Win Scenario

Stagflation forces central banks into a politically difficult choice. A new Fed chair, likely confirmed during this period, will take office amid a supply shock as inflation expectations drift and growth softens. Cuts look like accommodation of inflation and holds look like indifference to growth. Either choice could erode credibility, and the term premium could widen to reflect it. Long bonds underperform even if the Fed eases.

Asia Bears the Brunt of the Shock

About 80% of crude transiting Hormuz is bound for Asia, which means Asia carries the highest stagflation risk. India is already restricting industrial and commercial gas supply, having received its last Middle East tankers in early April. Currencies of energy importers, such as the Indian rupee, Korean won, Thai baht, and Philippine peso, are likely to underperform.

Gulf economies are themselves exposed on the import side. Bahrain and the UAE see disruptions to more than half their inbound trade. The United States, with domestic shale production and limited direct Gulf import exposure, is relatively insulated from supply disruptions but not from prices, since crude is a global commodity.

Limited Paths to Reopening

Reopening the strait requires either a diplomatic resolution or a credible naval coalition, neither of which is imminent. President Macron stated that France never envisaged warships into Hormuz, proposing instead a security mission coordinated with Iran. The U.S. proposal remains unanswered. Markets are pricing in a risk premium without a clear catalyst for de-escalation.

Political pressure to reopen the Strait is building, as both the U.S. and Iran are absorbing costs of the closure daily. Trump faces rising gasoline prices heading into the midterms, inflation trends that complicate the Fed transition, and pressure from Gulf allies who want the waterway reopened without American boots on the ground. Inaction looks weak, but military action would spark a wider war. Tehran, meanwhile, faces a collapsing economy, lost oil revenue it cannot replace, and growing isolation as even sympathetic neighbors lose patience with stranded cargoes. The regime’s leverage is real but diminishing. Each week the strait stays closed, the political cost of accepting terms rises for both leaders simultaneously.

Bottom Line

An indefinite Hormuz closure converts a geopolitical event into an inflation regime. A scenario of oil at $120 to $130, stranded Qatari LNG, fertilizer and freight repricing, and central banks caught between mandates is not fully priced into the market. Equity investors appear to be treating the energy shock as background risk, while commodity and policy coverage are treating it as a continuing inflation input. That gap closes one of two ways. Either the strait reopens and the risk premium fades, or Q2 guidance begins reflecting higher fuel, freight, and input costs — and the inflation regime takes hold. Portfolios should be positioned in quality companies, particularly in industries with pricing power. Duration risk, not headline risk, is now the variable that matters.