Key Observations

- Inflation is shifting from a cyclical phenomenon to a structural regime.

- Energy markets now reflect a persistent geopolitical risk premium.

- Tariffs and supply chain diversification are increasing baseline production costs.

- AI infrastructure spending is creating unexpected demand-side inflation pressures.

- Electricity demand and grid constraints may become major inflation drivers.

- Essential household expenses are likely to outpace headline inflation for many consumers.

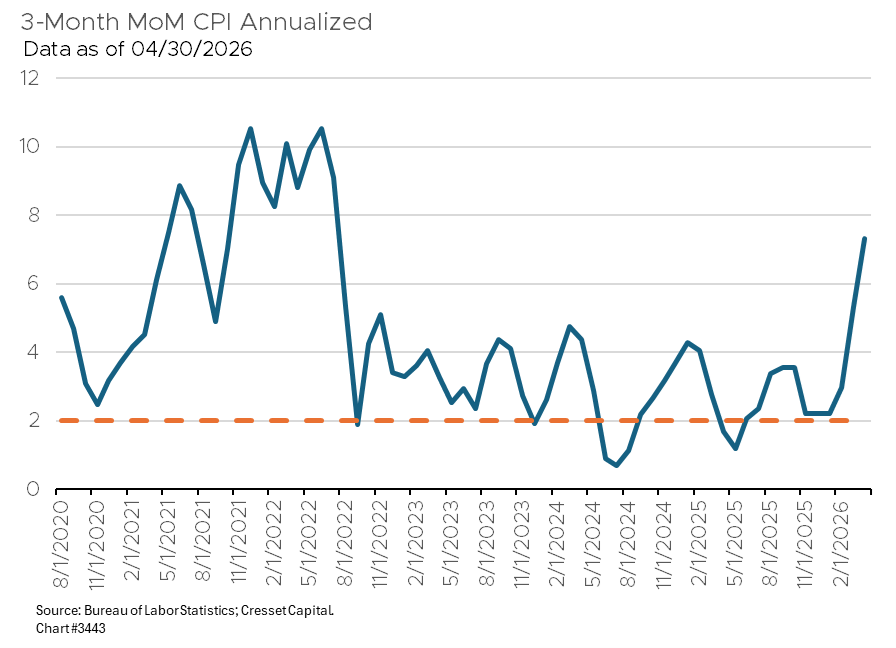

Inflation in 2026 is no longer the cyclical post-pandemic story. The drivers that fueled both the surge and the subsequent disinflation, namely the normalization of goods supply chains and shelter costs rolling over, have largely played out. What remains appears to be a structural inflation regime shaped by three forces that will define the price environment for years: energy and trade policy, the artificial intelligence (AI) infrastructure buildout, and the cumulative pressure these forces place on U.S. household budgets.

Energy and Trade: The Return of Cost-Push

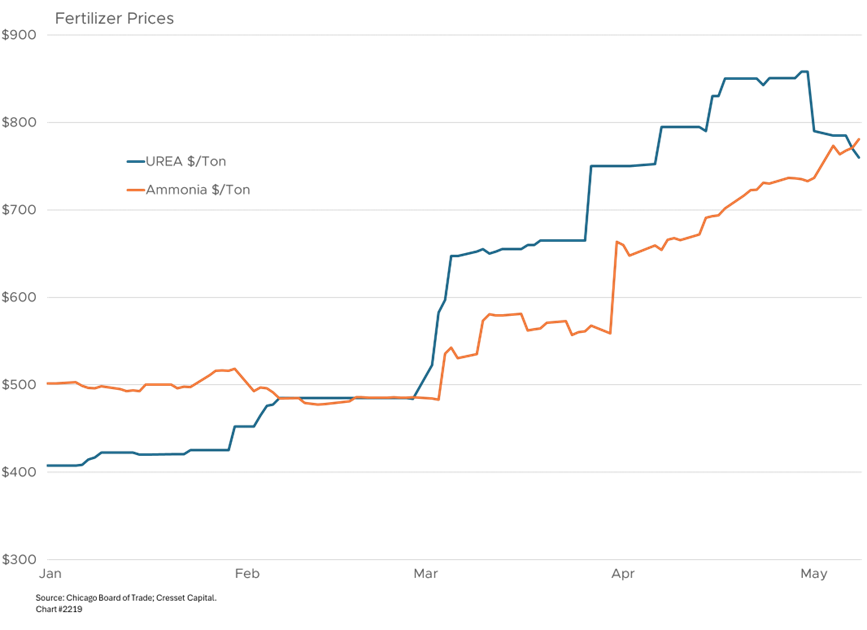

The geopolitical risk premium embedded in energy markets has become a persistent feature rather than a transient shock. Conflict in the Middle East, ongoing sanctions on Russia’s energy exports, and declining OPEC+ production have conspired to create a higher structural floor under oil prices. Its first order impact on consumer price index (CPI) contribution remains modest, however the second-order effects on transportation, petrochemicals, fertilizer and electricity generation could have an important impact on a broad basket of goods and services.

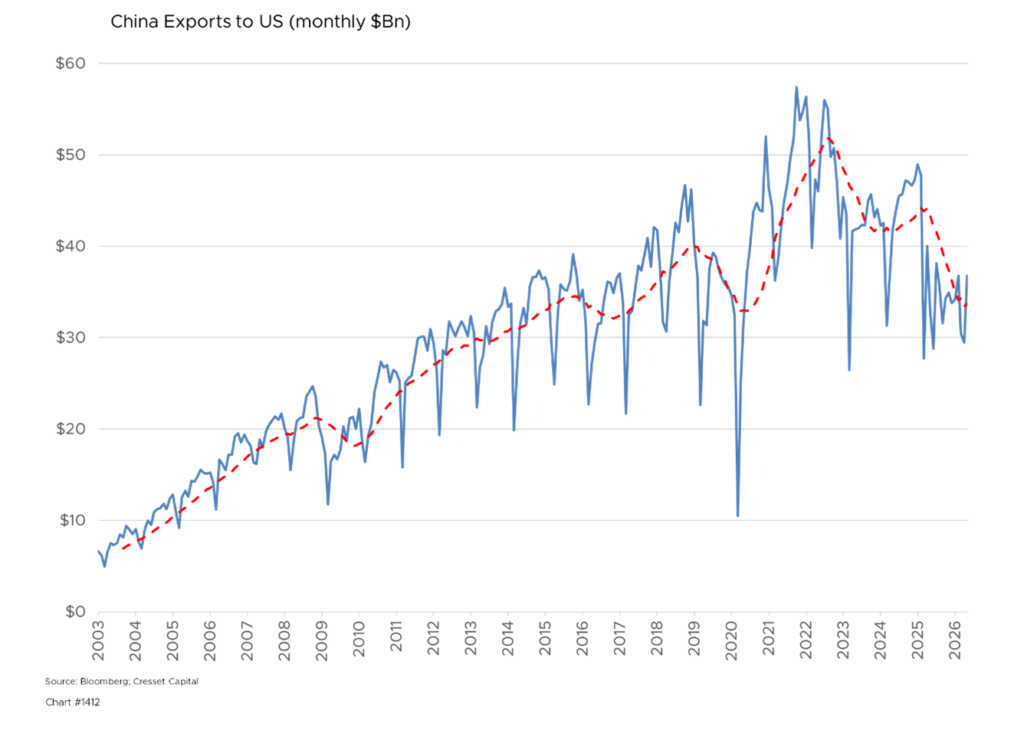

Trade policy compounds the picture. The cumulative tariff structure now in place represents the most significant repricing of imported goods in a generation. While economists debate whether tariffs produce one-time level adjustments or persistent inflation, categories with limited domestic substitution, such as consumer electronics, apparel, certain industrial inputs, and pharmaceuticals, are exhibiting price stickiness that goes well beyond the initial pass-through period. Supply chain diversification away from China has reduced single-source risk, but has raised baseline production costs, with those costs eventually reaching consumers.

AI Infrastructure: The Demand Shock Nobody Modeled

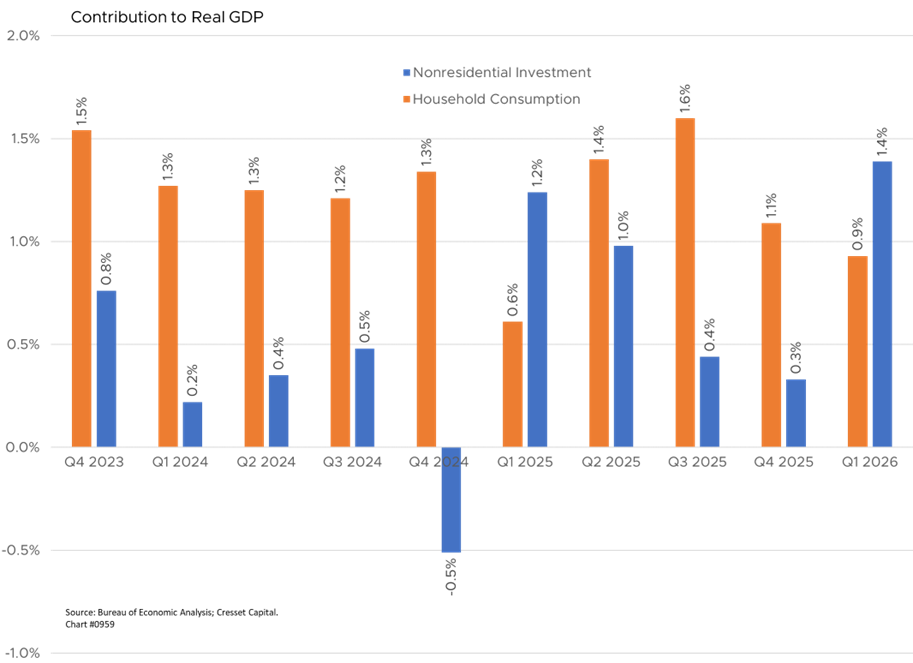

The capital expenditure cycle underpinning AI infrastructure has become an inflationary force, and one that traditional models struggle to capture. Hyperscaler capex now exceeds $300 billion annually, with the bulk of that spending concentrated in data center construction, specialized semiconductors, and the electrical infrastructure required to power both. Last quarter, business spending and investment contributed more to U.S. economic growth than did household consumption.

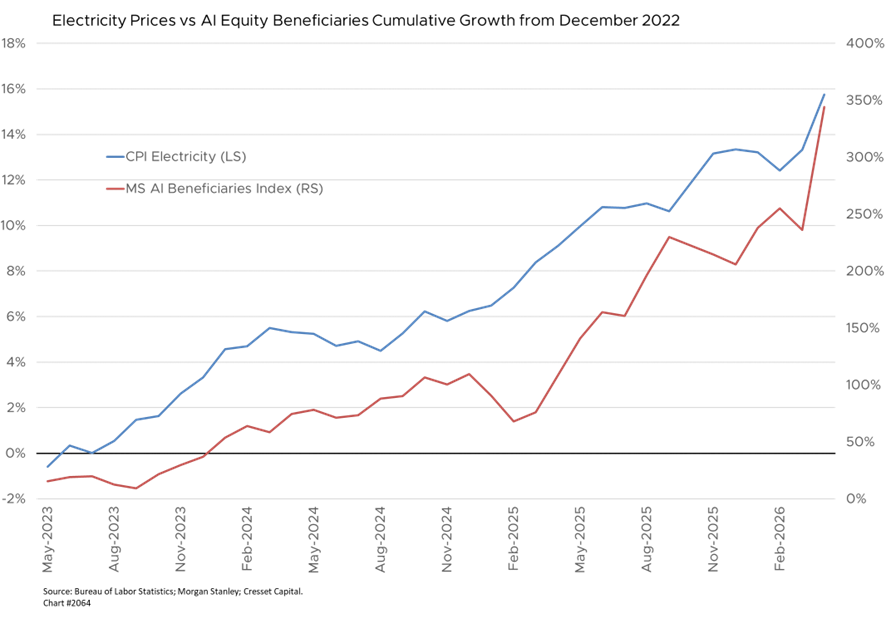

Electricity demand profile is the most underappreciated channel. Data center power consumption is projected to roughly double over the next several years, colliding with a domestic grid that took decades to build and cannot be expanded on a comparable timeline. Utilities across the Southeast, Mid-Atlantic, and Texas are already signaling capacity constraints. The result is upward pressure on industrial electricity rates that will eventually flow through to residential customers, and through them to the broader services economy.

Beyond electricity, the buildout is absorbing skilled construction labor, specialty steel, transformers, switchgear, and copper. These categories heretofore were not central to the post-pandemic inflation story, but they have now taken center stage.

The Household Squeeze

For American households, the inflation experience over the next several years will feel different from the headline numbers. The basket of essential expenditures, including electricity, insurance, healthcare, food at home, and shelter in supply-constrained markets, is likely to run persistently above the all-items index.

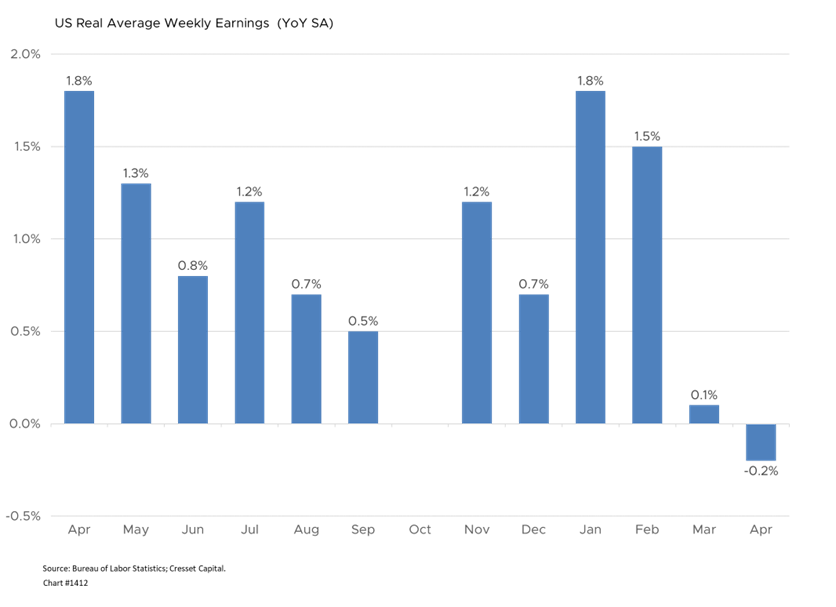

The price of discretionary goods may continue to slow or even decline, but the share of household budgets devoted to non-discretionary categories has been rising, particularly for middle-income families. Wage growth has not kept pace with inflation recently.

The bifurcation matters for both political and economic reasons. Wealthier households, whose spending skews toward services and experiences and whose asset portfolios benefit from elevated nominal growth, will experience inflation as a tailwind. Lower and middle-income households, more exposed to essentials and dependent on wage growth that has decelerated in many service sectors, will experience it as a squeeze. This K-shaped inflation experience reinforces the broader bifurcation in consumer behavior that has defined this cycle.

Bottom Line

For investors, the assumption that inflation reliably returns to two percent should be discarded as a planning baseline. A range closer to two and a half to three and a half percent is more realistic, with episodic spikes tied to energy and geopolitics.

Energy producers — and sectors tied to the AI buildout — offer both inflation protection and exposure to the dominant capex cycle. Fixed income allocations need to account for the possibility that the long end remains pressured by fiscal supply and term premium normalization, favoring shorter duration and credit selectivity over duration extension.

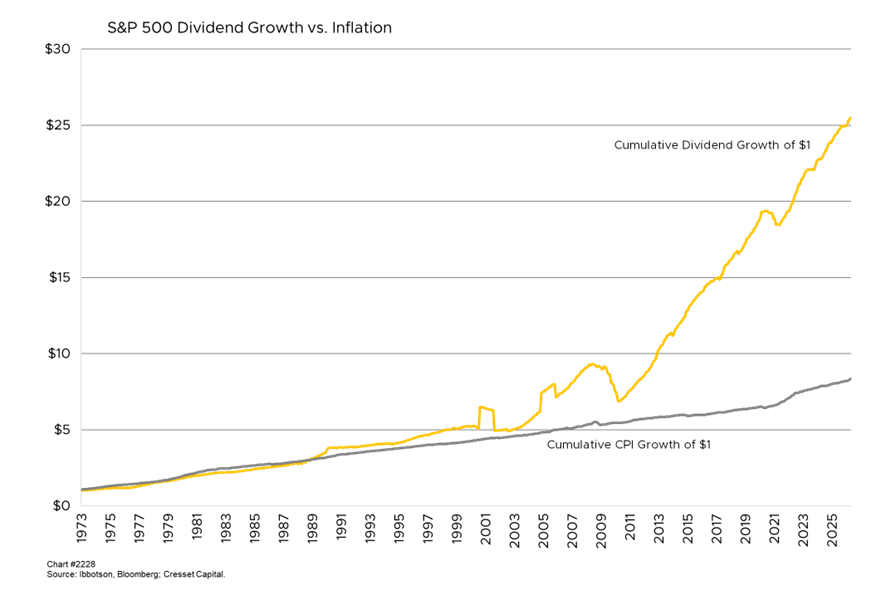

Finally, equity portfolios should tilt toward high-quality companies with pricing power, capital discipline, and exposure and persistent dividend growth rather than relying on the multiple expansion that defined the prior decade. History has shown that quality dividends have been a valuable inflation hedge.