Key Observations

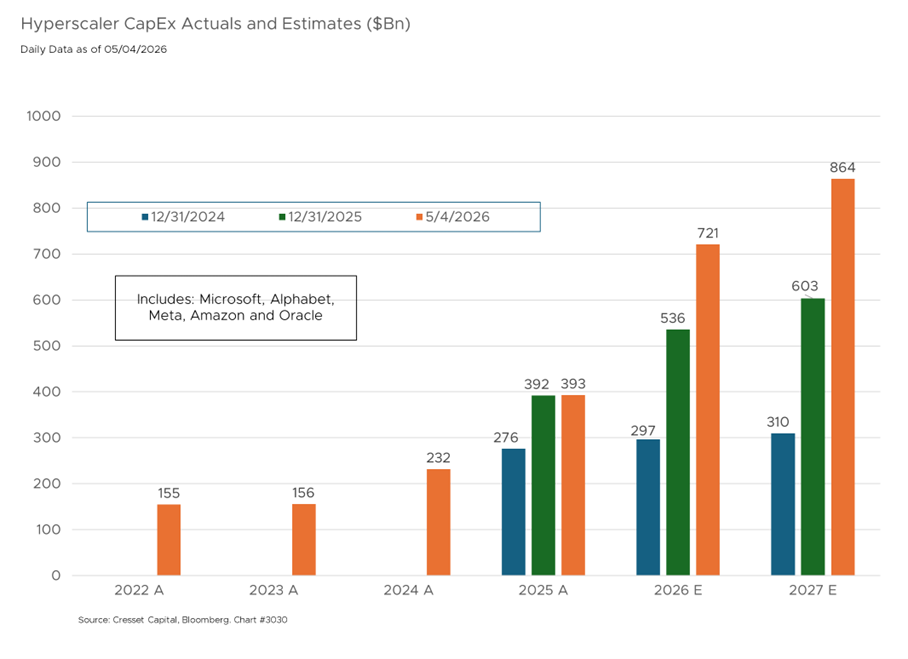

- Hyperscaler capex is reaching unprecedented levels, signaling strong conviction in AI-driven demand.

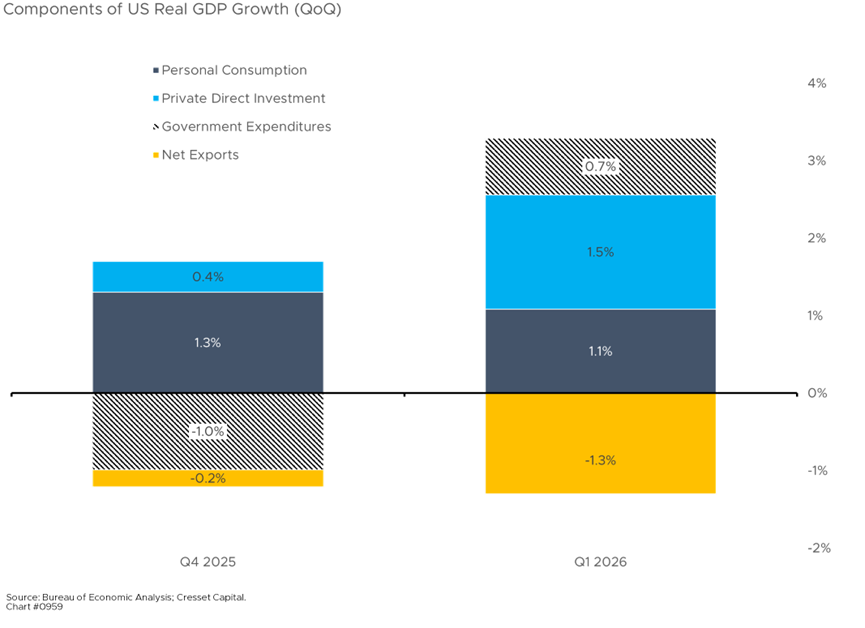

- Business investment, not consumer spending, is now the primary driver of GDP growth.

- Big Tech earnings remain exceptionally strong, with high beat rates and accelerating AI revenue.

- Index-level valuation concerns mask meaningful dispersion beneath the surface.

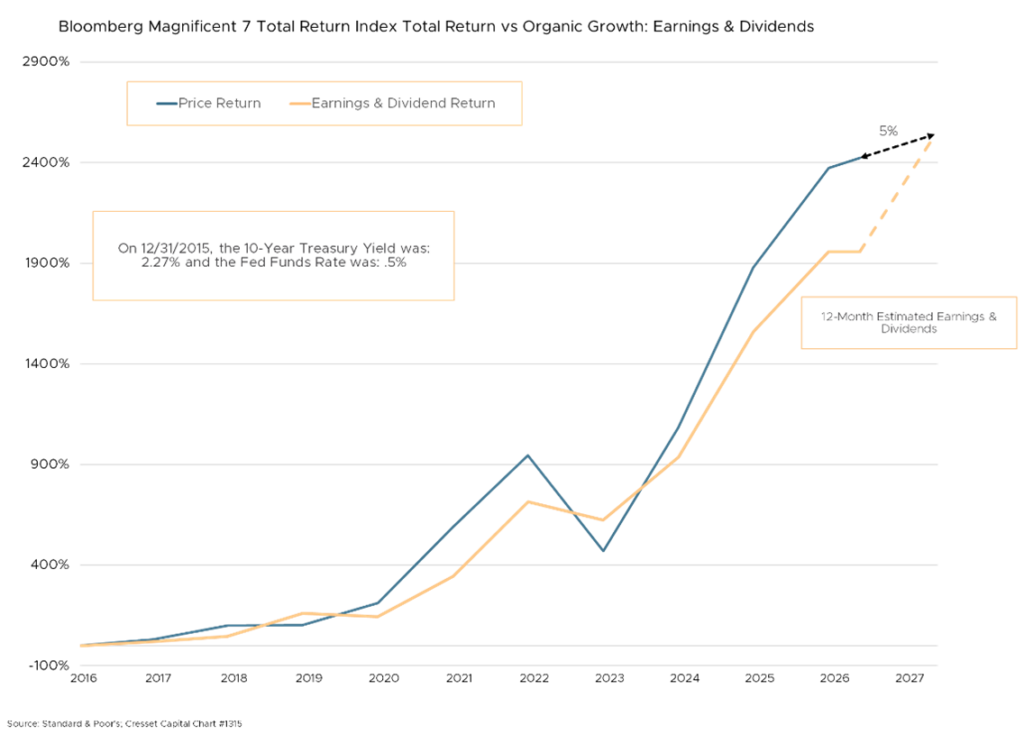

- The Magnificent Seven continue to justify premiums through superior earnings power and balance sheets.

- The AI infrastructure buildout is backed by real, monetizable demand, not speculation.

The current earnings season has produced a rare combination: record operating results, a record-high index, and unprecedented capital expenditures. Hyperscaler capex plans now exceed a combined $700 billion for 2026, with Alphabet, Microsoft, Amazon, and Meta clustered between $125 billion and $200 billion, and Tesla approaching $25 billion. The S&P 500 closed April above 7,200, representing its best month since 2020, and currently trades at 20.9 times forward earnings, above its long-term averages. Wary investors are asking whether this represents confidence or risk. The weight of the evidence points to a confidence signal grounded in genuine, monetizable demand.

Investment, Not Consumption, Is Driving Growth

For the first time in recent memory, Q1 2026 business investment outpaced consumer spending as the primary driver of GDP, contributing roughly 1.5 percentage points to growth versus 1.1 from consumption. Overall, GDP expanded at a 2.0% annualized rate, a meaningful rebound from Q4’s 0.5% pace. The investment surge was concentrated in AI-related categories, computer equipment, software, and non-residential construction, which expanded at the fastest pace in nearly three years. Households remained a positive contributor to growth but played a supporting role last quarter. This shift is positive for GDP durability, since business investment tends to enhance productivity, while consumer spending is ephemeral.

Hyperscaler Earnings Power Remains Exceptional

Hyperscalers’ fundamentals are outstanding. Q1 earnings per share surprised to the upside by 20.7%, with an 84% beat rate, the strongest showing since early 2021. Operational results across big tech were uniformly strong. Meta posted its largest revenue jump in nearly five years, with ad revenue up 12%. Alphabet grew 22% to $109.9 billion, with Google Cloud accelerating to 63% growth. Microsoft reported record revenue of $82.9 billion and an AI run rate above $37 billion, up 123% year over year.

Amazon delivered $181.5 billion, with AWS expanding 28%. Operating leverage helped drive margin expansion. Alphabet and Meta grew operating income by roughly 30%, Apple’s gross margin reached 48.2%, and Meta’s net income surged 61%. A new partnership between Google Cloud and Apple Intelligence further reinforces a multi-year demand pipeline. These are the signatures of companies meeting real, accelerating demand.

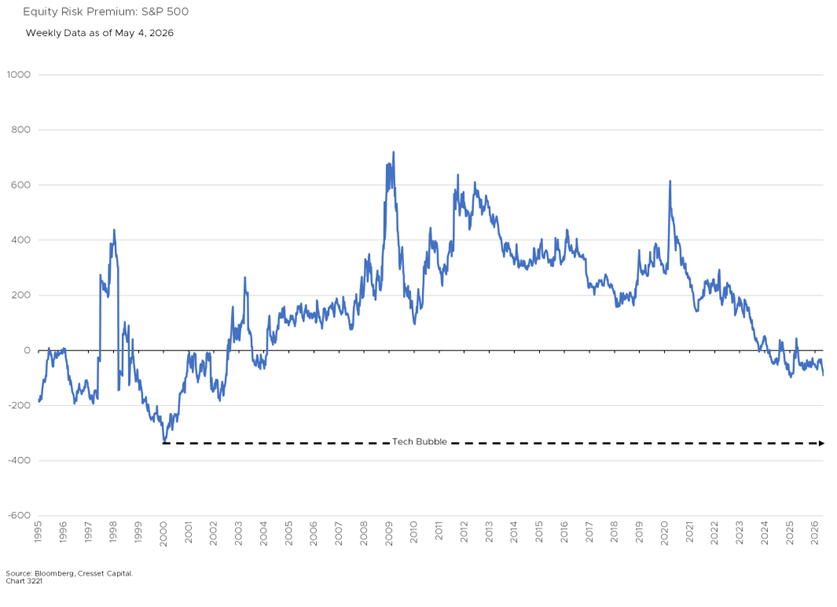

Valuation Concerns vs. Earnings Reality

While valuation concerns at the index level are legitimate, they should not be conflated with hyperscaler valuations. The 20.9x forward multiple on the broad market does sit above historical averages, and the equity risk premium is compressed against a 3.5% to 3.75% fed funds rate. However, differentiation between the Magnificent Seven (Mag 7) and the S&P 493 is already underway. The largest hyperscalers offer robust earnings growth, solid balance sheets, and accelerating AI revenue that support multiples that look reasonable, even attractive, against forward earnings power that few other parts of the market can match.

Bottom Line

While the S&P 500 at 20.9 times forward earnings is stretched by traditional valuation measures, the hyperscalers underpinning that index appear reasonably valued once their earnings trajectory is properly considered. Cloud backlogs, AI run rates approaching scale, and demonstrated pricing power confirm that the demand thesis is real and durable. The capex cycle, far from a warning sign, reflects management teams investing aggressively because they see the demand. Even the absence of a Fed dot plot under the new policy regime is a manageable backdrop, given the cash-flow strength of these franchises. For long-term investors, the Mag 7 should remain a core holding, and recent volatility around capex announcements should be viewed as an opportunity rather than a warning. These companies are leading the AI infrastructure buildout from positions of operational strength, and their valuations, properly contextualized, remain compelling.