Key Observations:

- Elevated uncertainty: The U.S.–Israel strikes on Iran and subsequent retaliation increase escalation and duration risk.

- Markets adjusting, not dislocating: Equities are modestly lower, bond yields slightly higher, and the dollar stronger.

- Energy is the key economic channel: Oil prices have risen sharply, European natural gas has surged, and shipping through the Strait of Hormuz is paused.

- Inflation back in focus: Higher energy prices are contributing to upward pressure on yields.

On Saturday, February 28, the U.S. and Israel launched attacks on Iran. In response, Iran has launched attacks against U.S. military bases and Israeli targets. We have been monitoring the ongoing conflict in Iran and neighboring countries closely.

At this stage, the key issue remains uncertainty, specifically what comes next and how long the conflict will continue.

Capital Market Reaction

As of this morning, capital market reaction, which began somewhat muted, has started to accelerate. Overall, the move has been somewhat less than one might have expected, with the key exception being the European natural gas markets.

The U.S. dollar is up about half a percent across major currencies. U.S. and European bond markets are selling off modestly, with yields rising around 5 basis points across the curve. Rather than yields dropping in moments of crisis, this rise is attributed to concerns that higher energy prices will increase inflation.

S&P 500 futures are trading lower by approximately 1 percent. European markets are down around 2 percent, and Japanese markets finished the day down approximately 1 percent. Overall, this price action appears somewhat less severe than expected given the headlines.

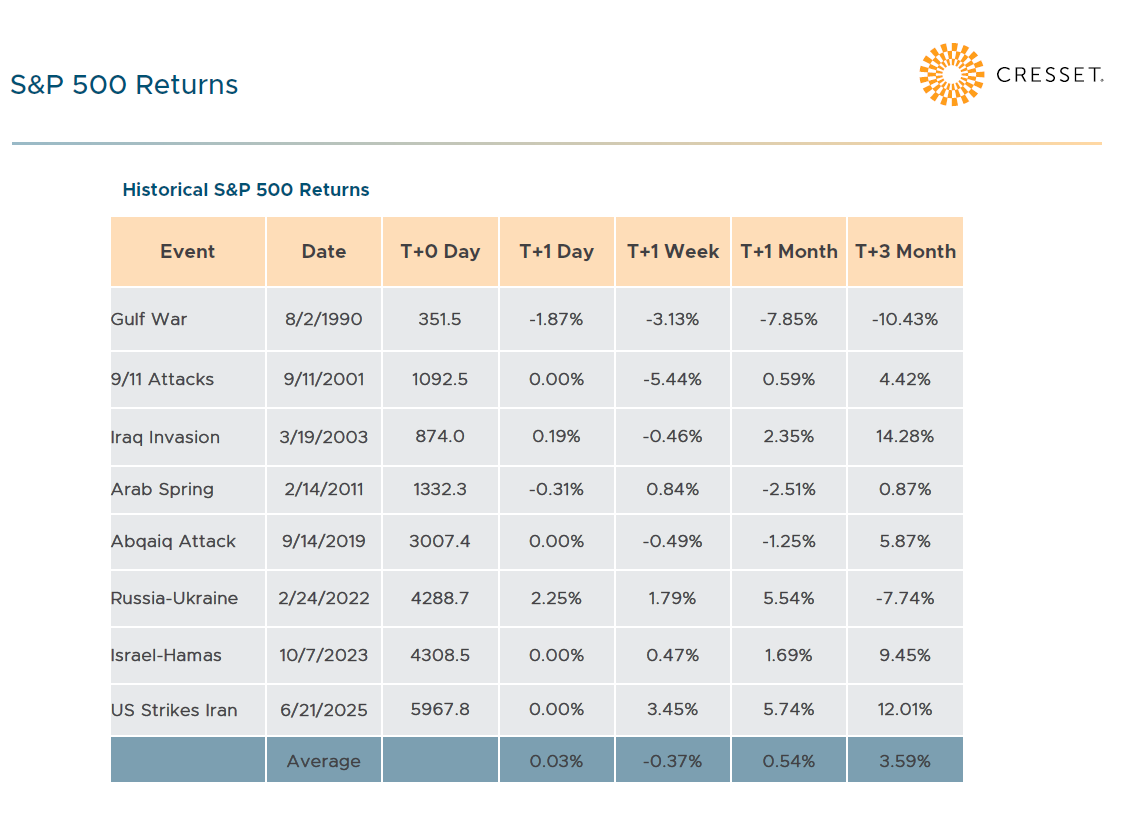

History shows (image below) that U.S. equity markets have often demonstrated resilience following military events. That said, something extreme or unanticipated should still be part of our thinking. Volatility should be expected as markets continue to digest developments.

Uncertainty and Duration Risk

This remains the biggest risk and is closely linked to the potential for civilian and U.S. casualties.

Over the past several days, we have seen extensive damage from U.S. and Israeli military actions, but we do not discount the risk that Iran has additional military capabilities in the region. As Iran attempts to form a new government, in whatever form that takes, the transition is unlikely to be orderly.

Public comments indicate that military action is expected to continue for several weeks. Iran’s ability to continue weapons production will be an important factor in determining the length of the conflict.

Further, while reports vary widely, it is believed that the Iranian Revolutionary Guard controls between 20 percent and 50 percent of the Iranian economy. Given their influence, it is unlikely they will cede power easily.

Casualties

Reports of casualties are beginning to rise. We know of four U.S. troops killed thus far, nine fatalities in Israel, and five across other Middle Eastern countries. The President has said he expects casualties to increase. Three American fighter jets were downed by friendly fire from Kuwait; all six crew members ejected safely.

Casualties will factor into the duration of the conflict and its impact on sentiment toward the U.S. government at home and abroad.

Oil and Natural Gas Prices

Oil presents the most immediate economic risk.

As of this writing, the spot price for Brent crude is up just under 9 percent, and European natural gas is up 40 percent. The European market is heavily dependent on liquefied natural gas (“LNG”) shipments from the Middle East. U.S. natural gas is up about 5 percent.

Shipping is currently at a standstill through the Strait of Hormuz. The immediate impact is most pronounced in the European energy market. While oil pipelines in the Middle East provide some alternative sourcing options, that flexibility does not exist for LNG.

China and Russia

We have not seen any clear action from either country. We will continue assessing how changes in Iran may impact their activities in the Middle East and elsewhere. China is a significant lender to Middle Eastern countries, so that exposure could be impacted.

If the current regime in Iran changes, it seems plausible that China’s alignment with Russia could strengthen out of necessity for oil and gas supply. All of this is to say, it remains an uncertain situation that we will continue to monitor closely.

Iranian Proxies

Whether organized or reactive to the conflict, there may be ongoing risks of terrorism, including potential cyberattacks against the U.S. and others. We are saddened by the killings in Austin, Texas, and concerned by protests and violence against U.S. consulates abroad.

Perspective

As with any event like this, the natural tendency is to pause before taking new investment action. Discipline remains important. Decisions should be grounded in long-term objectives rather than short-term headlines.

Developments will continue to be monitored closely, and updates will be provided as circumstances evolve.

Cresset will host a Special Market Update event at 12:00pm CT, Register here to hear a more timely update.