For many ultra-high-net-worth (UHNW) families, entrepreneurs, and athletes, there comes a point when traditional wealth management no longer fits the complexity of their finances. When this happens, there are two primary wealth management models to consider: a family office or private bank.

Family offices are independent, client-owned entities designed to fully align with a family’s interests. Private banks are institution-owned divisions of large financial firms that provide specialized products and services. Both options offer high-touch financial services, but their ownership, incentives, and scope of advice differ significantly.

When comparing private banking vs. wealth management through a family office, some key differences include:

- Fee structures

- Fiduciary duty

- Breadth of access

- Scope of services

For UHNW families and individuals, this choice isn’t just about services — it’s about trust, goals, and long-term alignment.

In this article, we’ll explore the practical differences between family offices and private banking, and provide a framework to help you determine which model — or combination thereof — is best aligned with your wealth, needs, and future goals.

17 Considerations When Choosing Between a Family Office and Private Banking

1. Wealth Goals and Complexity

Start by getting clear about what you want to achieve with your wealth. For instance, if your main focus is on growing your investments, a private bank may be all you need. However, if your focus is on preserving wealth across generations, giving back through philanthropy, or upgrading your lifestyle, a family office may be a better fit. The complexity of your finances will also influence which option is best suited to your needs.

2. Ownership and Accountability

Consider how much control and accountability you want regarding how your wealth is managed. Some family offices are employee- and client-owned, there are no outside shareholders. They can focus exclusively on their clients’ needs. Private banks, on the other hand, may prioritize shareholder returns alongside client outcomes.

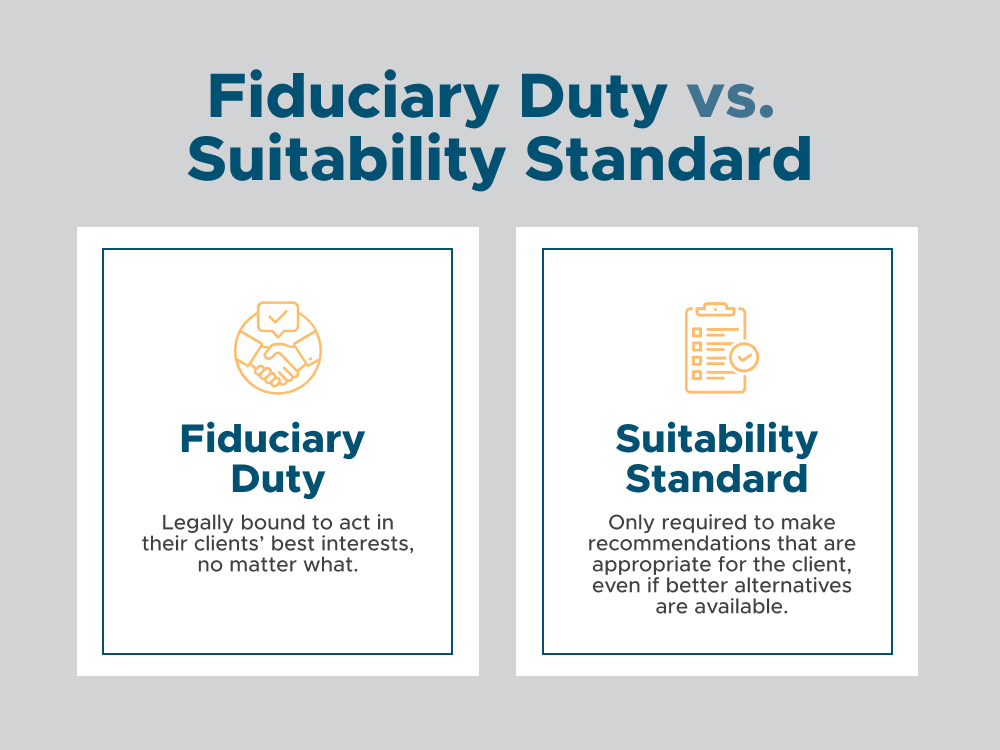

3. Fiduciary Duty vs. Suitability Standard

An important distinction between family offices and private banks is their obligation to their clients. Many family offices are fiduciaries, which means they are legally bound to act in their clients’ best interests. Private banks must only meet a suitability standard. This means they are only required to make recommendations that are appropriate for the client, even if better or more cost-effective alternatives are available.

4. Independence vs. Product-Driven Advice

The products you have access to will vary depending on which wealth management model you choose. While private banks primarily recommend their own products, family offices can select from a broader array of options.

5. Transparency in Fees

Compensation differs significantly between family offices and private banks. Many family offices follow a fee-only model with one revenue source and no commissions. Private banks utilize multiple revenue sources, including commissions, markups, custodial fees, revenue sharing, and 12b-1 fees, which can limit transparency about where your money is going.

6. Regulatory and Legal Record

Trust is a critical factor when choosing who you want to manage your money. For family offices, you’ll want to make sure they have no history of fines or regulatory disclosures. For private banks, you’ll want to check for any prior Securities and Exchange Commission (SEC) or Financial Industry Regulatory Authority (FINRA) fines and plaintiff awards.

7. Breadth of Services Beyond Investments

In general, family offices offer a broader range of services than private banks. While private banks focus primarily on portfolio, lending, and cash management, family offices also offer tax, estate, philanthropy, concierge (lifestyle, travel), and governance services.

8. Customization of Portfolios

How much your investment portfolio is tailored to your needs will differ between family offices and private banks. While family offices are able to design bespoke portfolios for each family they serve, private banks generally use model portfolios with limited customization.

9. Institutional vs. Retail Pricing

When working with a family office, you’ll get access to institutional-level investments and negotiated costs. In contrast, private banks offer retail pricing, leverage multiple revenue sources for compensation, and are incentivized to recommend their own products, even when better options may be available.

10. Custodial Safekeeping

Protecting your assets is essential. With a private bank, you’ll have a single custodian that keeps all your assets in-house. With a family office, you’ll have multiple, independent third-party custodians. This diversification may help keep your assets safer.

11. Investment Access and Innovation

Both family offices and private banks offer investment management as part of their core services. However, the investment opportunities they have access to are not the same. While a private bank primarily has access to large-cap or “mega” private funds, a family office also has access to niche private strategies and early-stage investments.

12. Performance Measurement

Trusting the performance data on your investments is important. If you’re working with a family office, independent third parties are responsible for measuring your returns. If you’re working with a private bank, the bank is responsible for the reporting, which could potentially introduce bias.

13. Costs and Infrastructure

Set-up costs for a family office are higher than with a private bank due to hiring, compliance, and technology. However, private banks have higher hidden costs over time that can really add up.

14. Privacy and Confidentiality

Although family offices and private banks may both prioritize confidentiality, private banks are required to disclose some information as part of regulatory compliance and institutional reporting. With a family office, privacy is built-in because there is no institutional data-sharing.

15. Lifestyle and Concierge Support

If you’re looking for support beyond just financial management, such as concierge services, travel planning, governance, and family education, a family office may be your best option. Private banks typically do not offer these services.

16. Suitability for Expats and Global Families

Private banks tend to have limited specialization for expats, so if you need support with cross-border tax, FX, and regulatory compliance, a family office is more likely to have the expertise you need.

17. Best Fit by Client Type

Family offices tend to service UHNW families, entrepreneurs, and athletes with intergenerational wealth. Private banks tend to cater more toward HNW individuals who want financial services without the infrastructure of a family office.

Frequently Asked Questions (FAQs)

What is the difference between a private bank and a family office?

Family offices and private banks both offer high-touch financial services, but there are significant differences between them. These differences include the level of control and accountability, fee structure, scope of services offered, investment access, amount of customization, and more.

What are the disadvantages of a family office?

The main disadvantage of a family office is that the initial setup costs tend to be higher than with a private bank. However, private banks have higher hidden fees that add up over time.

How wealthy do you need to be to have a family office?

The minimum net worth required to start a family office depends on the type of family office being established (single family office, multi-family office, outsourced family office) and the family’s ability to sustain the operational costs long-term.

Choosing Your Ideal Wealth Management Partner

There are a number of factors to consider when deciding between a family office, private bank, or hybrid model of the two. These factors include cost structure, service scope, and level of control. Using the framework above will help you decide which structure and services best match your unique needs.

If you’d like to learn more about whether our family office is right for you, request an introduction with one of our founders today. Together, we can explore how our tailored approach can meet your family’s unique needs, goals, and vision for the future.