Key Observations

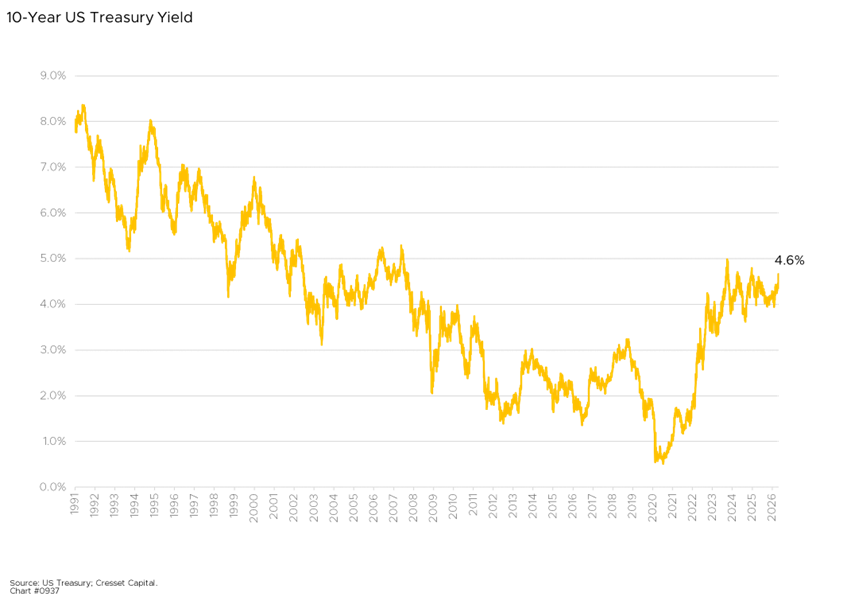

- The 30-year Treasury yield has moved above 5% for the first time since 2007.

- Higher Treasury yields directly pressure equity valuations by reducing the present value of future cash flows.

- Bonds once again offer meaningful competition to equities for investor capital.

- Leveraged companies are increasingly constrained by higher refinancing and borrowing costs.

- Rising yields are a global phenomenon tied to persistent inflation and elevated government borrowing.

- Markets are demanding a larger term premium amid uncertainty around the Fed’s policy path.

The yield on the 30-year Treasury has pushed above 5%, a threshold not crossed since 2007, while the 10-year recently touched 4.68%, its highest reading in about two years. For most of the past fifteen years, the risk-free rate was a background variable — low, stable, and easy to ignore. It is now becoming a problem. The question for investors is not whether higher yields matter, but how widely the effects travel once the anchor of the financial system moves.

Why Higher Yields Ripple Across Markets

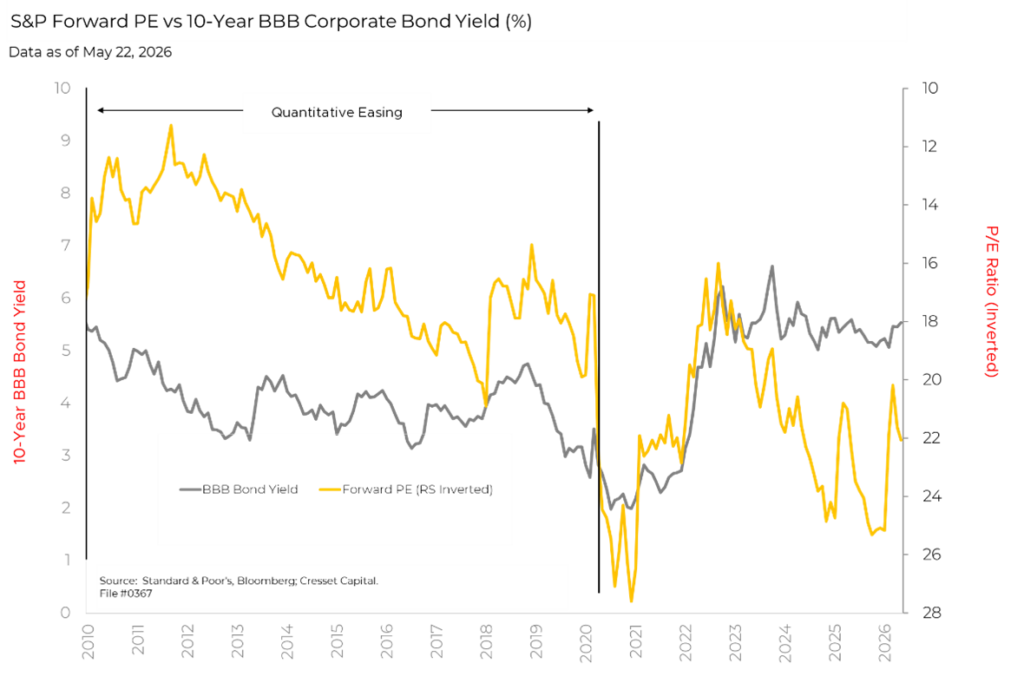

The value of every financial asset from a U.S. investor’s perspective relies on the Treasury yield. When yields rise, the present value of distant cash flows falls, and it falls hardest for assets whose payoff lies furthest out. That’s why the market’s forward price-earnings ratio is tied directly to the 10-year Treasury yield. The benchmark Treasury’s recent move through 4.6% halted an equity rally that had carried major indexes to fresh records. Investors are not abandoning equities, but they’re simply paying less for anticipated future cash flows.

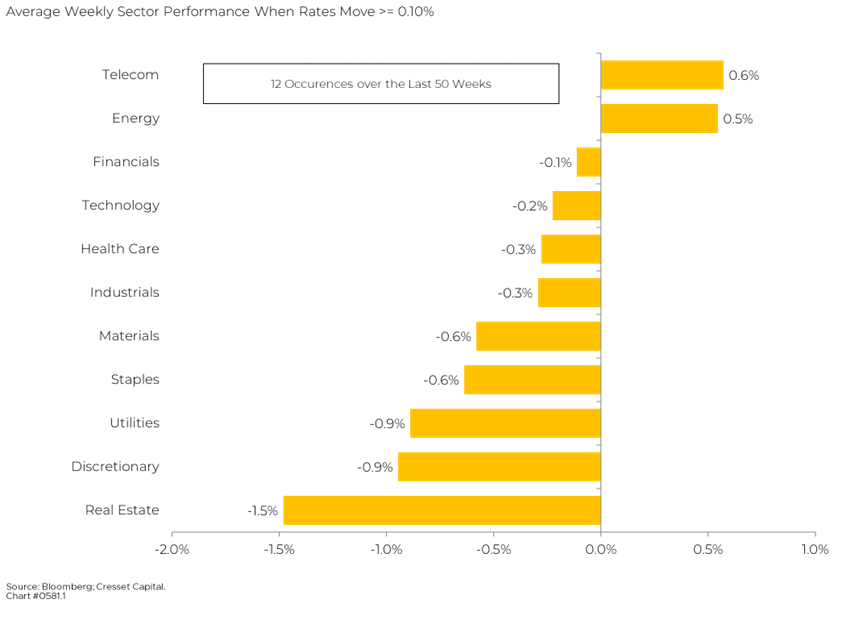

Stocks Now Face Real Competition

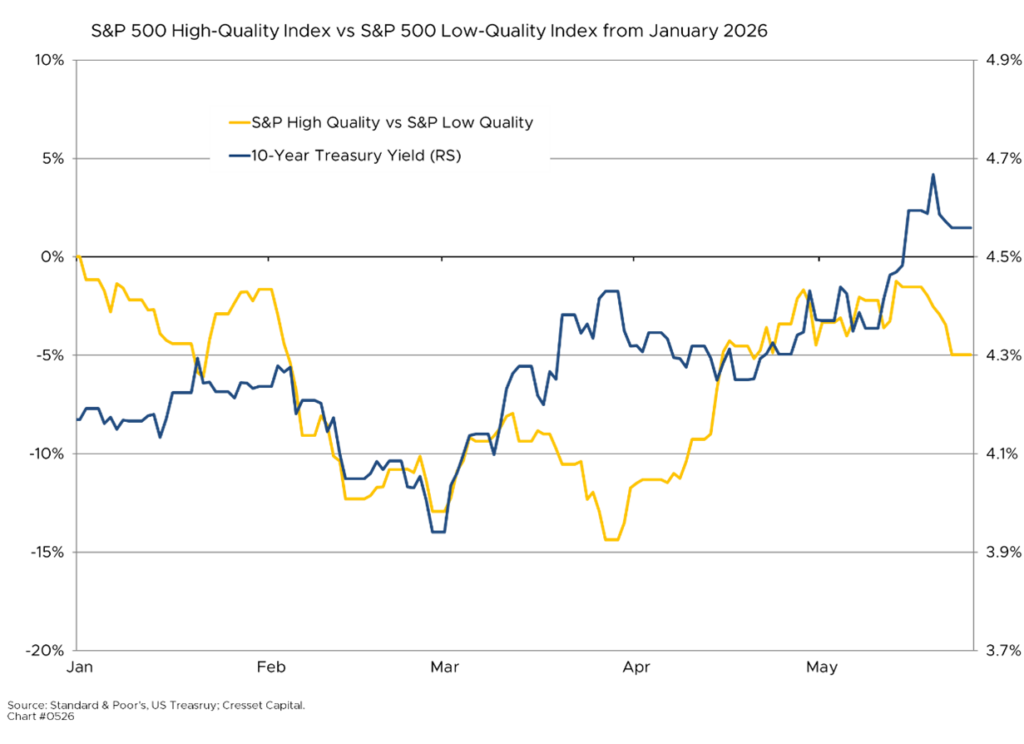

A 5% long-bond offers a genuine, contractual alternative to equity risk, something it could not credibly do during the quantitative easing days. The hurdle rate for owning stocks rises accordingly. Capital-intensive, rate-sensitive sectors feel this first, utilities, real estate, and consumer staples among them, since their steady cash flows compete directly with bond coupons, although the effect is not uniformly negative. A steeper curve widens net interest margins for banks, and the financial sector can benefit even as rate-sensitive groups lag.

The Financing Channel Tightens

As Treasury yields climb, so does the cost of refinancing maturing debt, funding capital expenditure, and sustaining share repurchases. Lower-quality companies with leveraged balance sheets tend to feel the impact first, as their marginal corporate decisions — whether to invest, repurchase shares, or take on additional debt — increasingly tilt toward caution. It is the financing channel through which a financial-market repricing morphs into an earnings-growth story.

Meanwhile, heavy corporate bond issuance tied to the artificial-intelligence (AI) build-out adds to the supply of debt that investors must absorb, which only reinforces the upward pressure on rates.

A Global Repricing of Sovereign Risk

This is not just an American episode. The British 30-year gilt has pushed toward 6%, Japan’s 30-year has cleared 4%, and German bund yields are rising in step. The common thread is a reassessment of two long-running assumptions, that inflation would revert to 2% and that governments would eventually restrain borrowing. Neither has held. U.S. deficits have averaged more than 6% of GDP across 2023 through 2026, a level historically associated only with war or recession, and inflation has run above target since 2022.

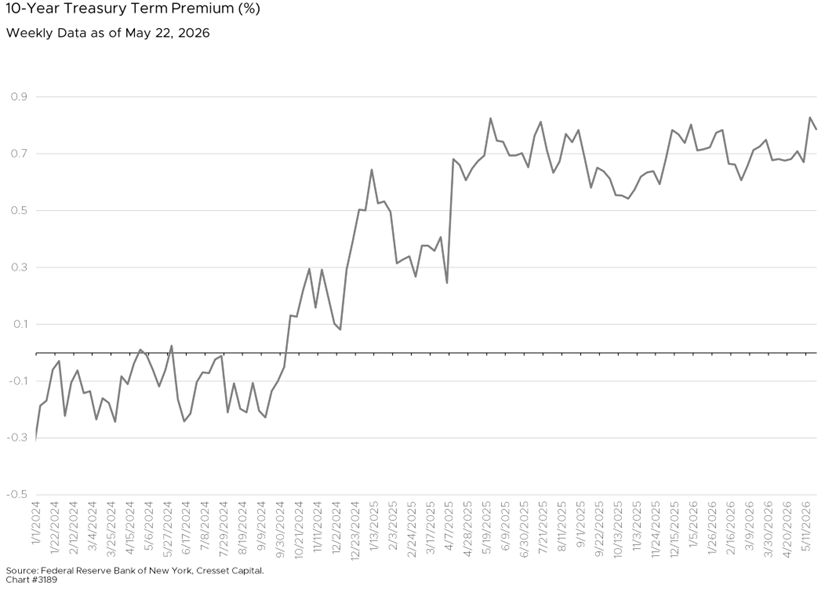

Uncertainty Around the Fed Is Raising the Term Premium

The Fed’s next move is compounding the uncertainty. Officials have signaled that a hike is now as plausible as a cut, given inflation pressure tied to elevated energy prices, and that ambiguity has lifted short-term yields as well.

When the market cannot confidently price the central bank’s reaction function, it demands additional term premium — additional compensation for lending long rather than short. That premium, more than any single data point, explains why the long end has risen even as the policy rate sits below its prior peak.

Bottom Line

The striking feature of this market is how little the yield surge has dampened enthusiasm for equities, which have posted record highs on optimism around energy prices and AI. That resilience is real, but it should not be mistaken for immunity. A long bond yield sustained near or above 6% would likely force a broader repricing of risk assets.

The prudent response is not retreat but recalibration: favor quality balance sheets and shorter-duration cash flows, treat fixed income as a legitimate competitor for capital rather than a default afterthought, and recognize that the move closing the valuation gap between bonds and stocks may close from the equity side. The risk-free rate is rising and investors should pay attention.

Reader Note: I will be traveling for the next few weeks and will not be publishing a weekly market update in the interim.