Key Observations

- Markets rapidly unwound the “war premium” following the June 14 ceasefire announcement.

- Oil prices have fallen sharply, but supply disruptions and infrastructure damage remain unresolved.

- Equity markets have largely recovered, with earnings expectations now above pre-conflict levels.

- The Federal Reserve has shifted toward a more hawkish stance due to lingering inflation concerns.

- Gold underperformed during the conflict as rising real yields reduced its appeal.

- The structural drivers of Middle East geopolitical risk remain largely intact despite the ceasefire.

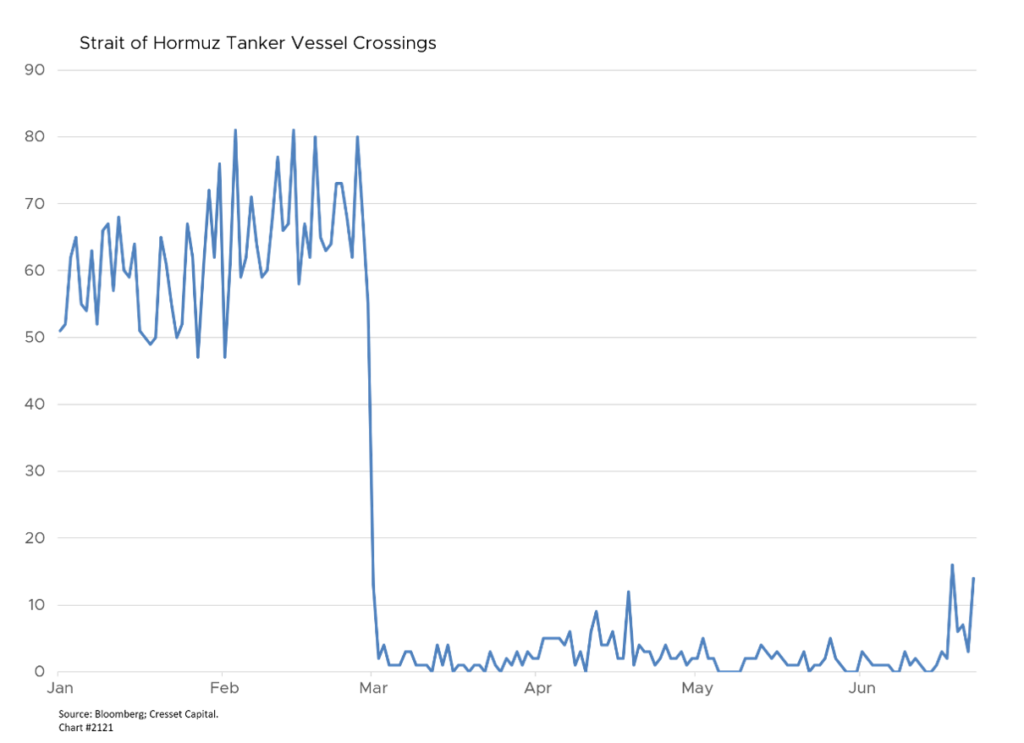

When the United States and Israel launched strikes against Iran on February 28, markets repriced in hours what geopolitics had been telegraphing for years. Oil surged, Treasuries sold off, the dollar strengthened, and equity investors scrambled to model a scenario none had fully stress-tested: a sustained closure of the Strait of Hormuz, the chokepoint through which roughly one-fifth of global oil and liquefied natural gas (LNG) supply flows. For 109 days, that scenario was not a model assumption, it was reality.

The ceasefire announced June 14 triggered an equally swift reversal. Brent crude fell below $80 per barrel for the first time since the conflict began. Treasury yields rallied across the curve. Emerging market currencies edged higher. European equities hit record closes. The relief trade, however, is running ahead of the resolution. Iranian mines have not been fully cleared from Hormuz. Vessel traffic through the strait remains a fraction of pre-war levels. The European Central Bank (ECB) chief economist cautioned this week that the inflation pipeline from the energy shock is still flowing, even as oil prices retreat.

A Ceasefire Without Resolution

More consequentially for investors, the ceasefire memorandum left unresolved the structural issues that made Iran a risk premium in the first place. Iran’s nuclear program, while heavily damaged, was not eliminated, its fate deferred to future negotiations. Its ballistic missile arsenal goes unaddressed by the agreement. Its proxies, including Hezbollah, remain armed and active. As one retired Israeli intelligence officer observed, the memorandum represents a collapse of the strategy designed to defang Iran for a generation.

Markets are celebrating a pause. The underlying architecture of Middle East risk has not fundamentally changed. That distinction matters how investors should think about what has been priced in, and what has not.

The Strait of Hormuz Shock

The trigger was the Strait of Hormuz. When Iran effectively closed the waterway in retaliation for U.S.-Israeli strikes, it cut off roughly one-fifth of the world’s daily petroleum supply, an estimated 10 to 11 million barrels per day. Brent crude, which had been trading near $72 per barrel in late February, surged above $112 by late March, a gain of more than 55% in under a month. West Texas Intermediate (WTI) climbed in parallel, topping $98 per barrel by mid-March.

The International Energy Agency (IEA) responded by authorizing the release of 400 million barrels from emergency stockpiles, a historically large intervention that temporarily capped prices but failed to arrest the broader inflationary impulse. Futures markets, at the height of the conflict, were pricing Brent above $100 well into 2027, reflecting not just supply disruption but structural damage to regional production infrastructure and port capacity that analysts warned would take years to repair.

With the peace deal announced and the Strait was set to reopen, although recent headlines belie that assumption. Nonetheless, Brent dropped below $80 per barrel, down more than 5% on the deal news and at its lowest level since early March. The relief is real but incomplete. The IEA’s May Oil Market Report projects the global oil market will remain in supply deficit through at least the fourth quarter of 2026, given cumulative production losses exceeding one billion barrels from Gulf producers since February, permanent damage to regional infrastructure, and the time required to bring idled capacity back online.

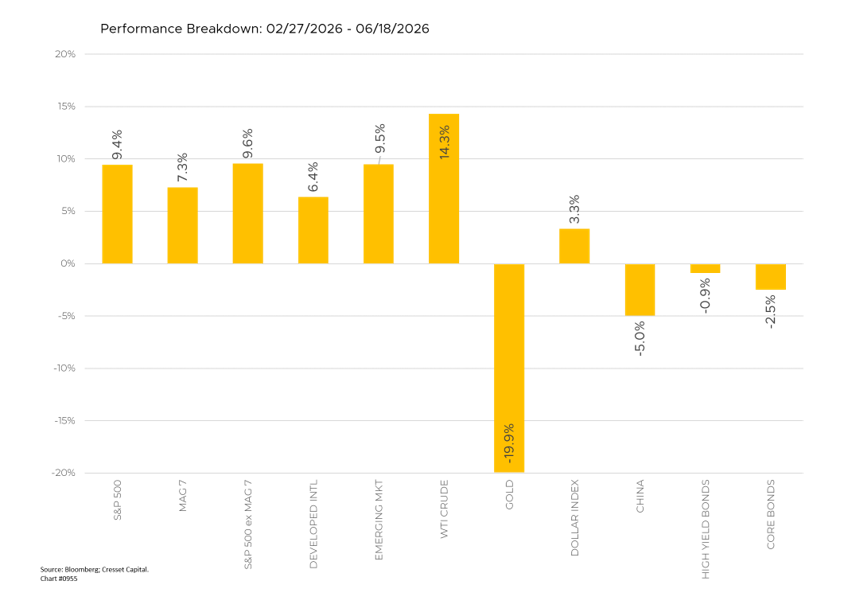

Equities Rebound as the War Discount Fades

Equity markets entered the conflict near all-time highs and plunged in the initial shock. The S&P 500, which had been trading near record levels in late January, shed all year-to-date gains within the first days of the war, falling toward 6,715 by early March. At one point the index had declined roughly 6.8% from its January peak. The Dow extended a four-week losing streak, its longest in three years. The Nasdaq dipped into correction territory, down nearly 10% from its October high, hit hardest by the combination of rising inflation expectations and higher discount rates on long-duration growth assets.

Sector damage was concentrated in semiconductors, airlines, materials, and rate-sensitive growth names. At the worst moments, nearly 90% of S&P 500 stocks were trading in the red simultaneously. International markets followed, with the outperformance many European and Asian indices had built through 2025 quickly evaporated.

The picture today, however, is materially different. Last week, the S&P 500 closed at 7,554, up 1.65% on the peace deal announcement, with the Dow hitting a new all-time intraday high and the Nasdaq surging 3.07%, its best session since late March. Asian markets responded with equal enthusiasm: Japan’s Nikkei jumped 3.5%, South Korea’s KOSPI surged more than 4% at the open, and technology names across the region posted outsized gains. The war discount has been substantially unwound, though the path back was uneven and will continue to be tested by implementation of the accord’s terms.

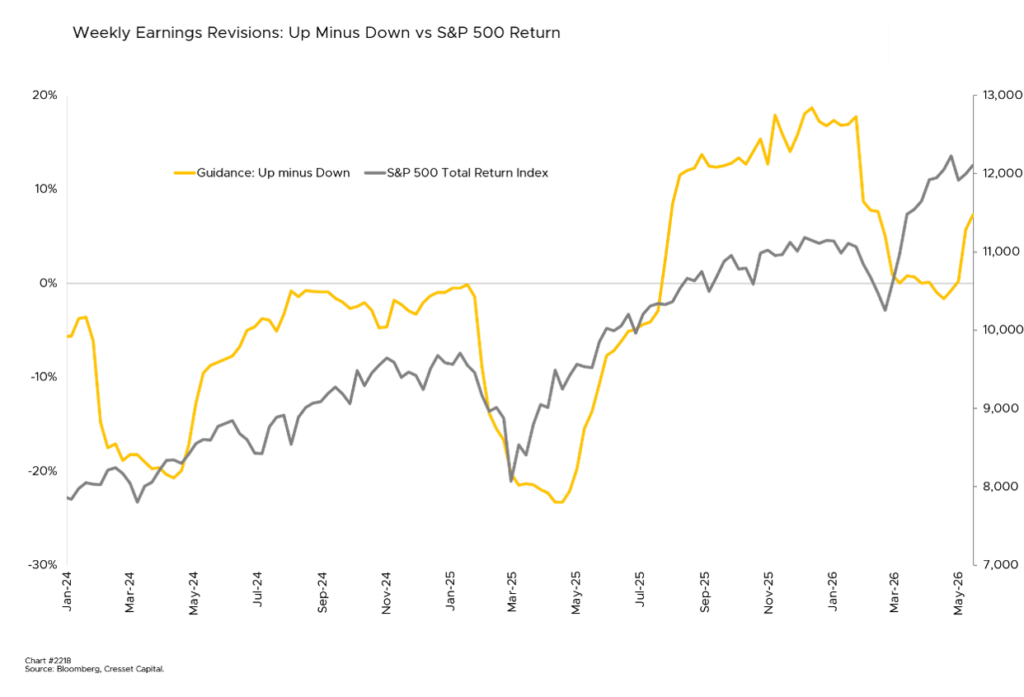

Why Earnings Expectations Have Improved

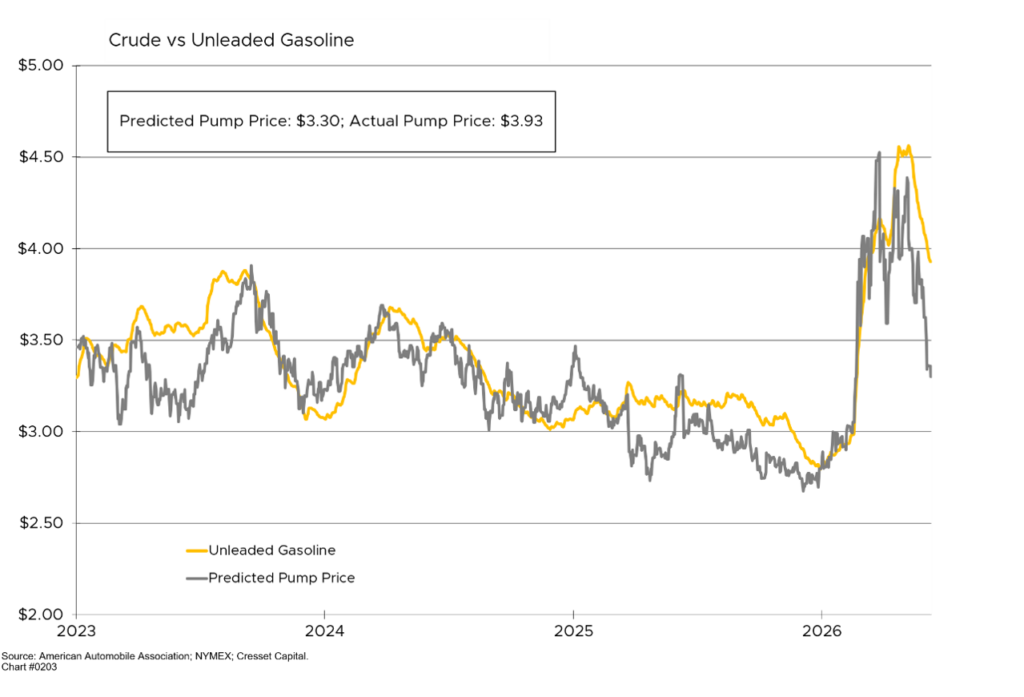

It should be noted that earnings growth expectations have improved since the war began, for a counterintuitive reason. The energy shock accelerated fiscal spending, defense contractors posted blowout quarters, and AI capital expenditures never slowed. Meanwhile, the companies most exposed to the conflict — airlines, manufacturers, and importers — are now looking at meaningful cost relief as oil retreats. Lower energy input costs fall straight to the bottom line.

Equity markets are also pricing in a re-acceleration of consumer spending as the energy tax on households lifts. Gasoline prices near the pump were a quiet drag on discretionary spending throughout the conflict. That headwind is reversing. Add it all together and forward earnings estimates for the S&P 500 are higher today than they were before hostilities erupted, reflecting both the sectors that thrived during the war and the sectors now positioned to benefit from its end.

Fixed Income and the Fed’s New Challenge

Perhaps the most consequential market shift during the conflict was in fixed income, because it rewired Federal Reserve expectations and repriced risk across every asset class. Through January and into early February, a softening macro environment, cooling consumer confidence, and subdued oil prices had pushed the 10-year Treasury yield down to 3.96% and the market was building toward a rate-cut consensus.

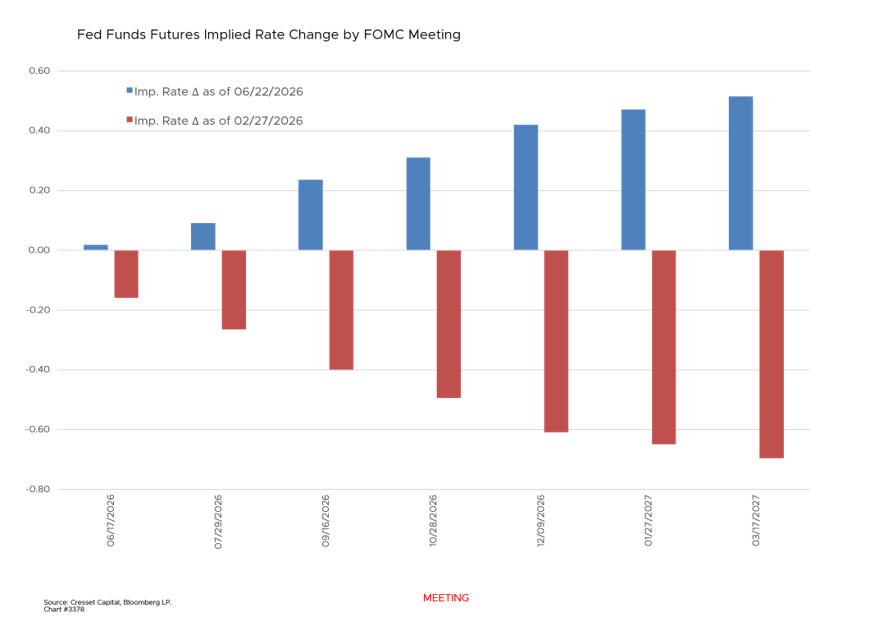

That narrative collapsed on February 28. Rather than triggering a traditional flight-to-safety bid into Treasuries, the energy shock from the Strait closure acted as a blunt inflationary force. By late March, the 10-year yield had climbed to 4.46%, a gain of 50 basis points in under a month. Interestingly, most of the rate move can be attributed to rising real rates, the “distrust premium” Treasury investors require to purchase U.S. Treasury obligations. Meanwhile, at the June Federal Open Market Committee (FOMC) meeting, Kevin Warsh’s first as chair, the committee voted unanimously to hold at 3.50%–3.75%, but the dot plot delivered the real message: nine of eighteen officials now project at least one rate hike before year-end, pushing the median 2026 rate forecast to 3.8%, up sharply from March’s 3.4%. The committee also raised its personal consumption expenditures (PCE) inflation projection to 3.6% for 2026 and stripped forward guidance language from a dramatically shortened policy statement.

Gold, the Dollar, and Global Spillover Effects

Gold’s behavior during the Iran conflict defied the simple safe-haven script. In the early weeks of the war, gold sold off sharply, losing more than 10% in a single week, its worst weekly performance since 1983. The reason was mechanical: surging Treasury yields offered real returns that competed directly with non-yielding bullion, and the inflation shock raised the prospect of higher rates, which further pressured gold through the real-yield channel.

Compounding the pressure, central bank buying from India and China, which had been a powerful structural bid underneath gold throughout 2024 and early 2025, has quietly slowed. Both nations appear to be pausing accumulation at these elevated price levels, removing a key source of incremental demand.

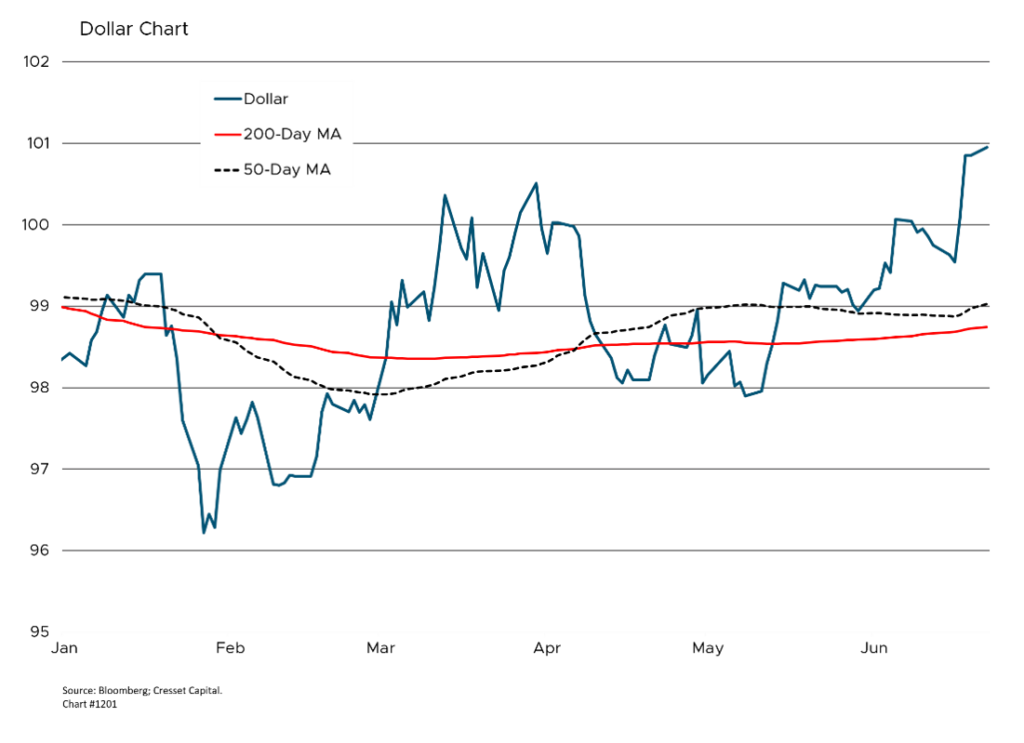

The dollar strengthened during the conflict, reflecting the traditional risk-off demand and elevated U.S. rate expectations. Emerging market currencies came under pressure, particularly those of energy-importing economies in Asia. The energy shock fell disproportionately on Japan, South Korea, and several Southeast Asian nations heavily dependent on Gulf oil. Japanese manufacturers and Korean chipmakers faced margin pressure from higher energy costs and supply chain disruptions that cascaded from the port closures. The peace deal has eased these pressures, as evidenced by the immediate 12% surge in SoftBank shares last week and the sharp rally in Korean memory giants Samsung and SK Hynix.

Bottom Line

The peace deal has compressed the tail risk premium that weighed on markets, but investors should resist the temptation to declare a full reset. Oil is retreating, yields are rallying, and equities have surged, yet the ceasefire memorandum leaves Iran’s nuclear program and ballistic missile arsenal unresolved, Hormuz mines uncleaned, and Iranian proxies intact across the region. The relief trade is real, but it appears to be outrunning the fundamentals.

The Federal Reserve’s June meeting underscored that gap. The message from the Fed is that even with oil retreating from its war-driven peak, the inflation pipeline is not yet clear, and policy will remain tighter for longer than markets had hoped entering the year.

For investors, the most important distinction is between what has been priced in and what has not. The worst-case energy shock scenario has been removed. Rate-hike probabilities have come off their peaks. Emerging market carry trades are reviving. Those are genuine tailwinds. What has not changed is the underlying architecture of Middle East instability, a Fed now tilting toward hikes rather than cuts, and an inflation backdrop that the ECB’s chief economist cautioned this week is still working through the pipeline. Peace is a necessary condition for normalization.