Key Observations

- AI valuations warrant caution, but today’s market leaders have far stronger fundamentals than those of the dot-com era.

- Strong earnings growth and robust cash generation continue to support AI infrastructure investment.

- Productivity gains from AI could create long-term economic benefits that extend beyond technology companies.

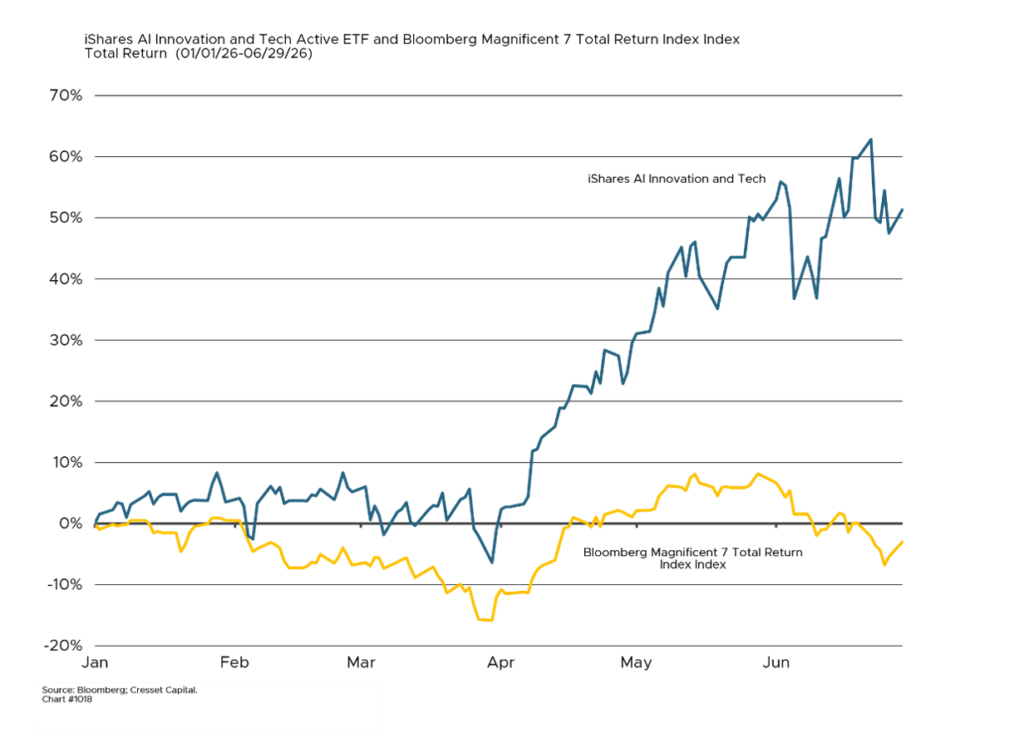

- Investment opportunities are becoming more selective as leadership broadens beyond the Magnificent 7.

- Second-order beneficiaries and private AI-related lending may offer attractive risk-adjusted opportunities.

- Long-term success will depend on quality, valuation discipline, diversification, and patience.

Is artificial intelligence (AI) an opportunity or a bubble? The evidence cuts both ways. Concentration risk is real, valuations in certain pockets are stretched, and the monetization timeline for hundreds of billions in annual capital expenditure remains uncertain. At the same time, the fundamental underpinnings of this cycle are categorically stronger than the dot-com era that bubble analogies typically invoke. We believe the balance tips toward opportunity, but only for investors who approach it with clear eyes about where the risks are concentrated.

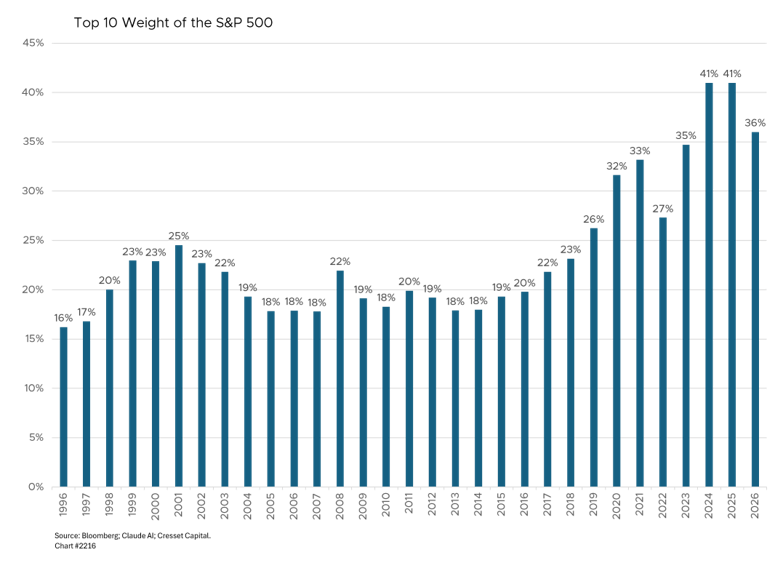

Nearly one-fifth of U.S. equity market capitalization is now tied to AI, while the ten largest S&P 500 constituents represent nearly 40% of the index, a concentration that has prompted legitimate comparisons to prior bubble peaks. Meanwhile, AI chip stocks have been responsible for a disproportionate share of market gains, and Taiwan, the linchpin of global semiconductor supply, sits at the center of an unresolved geopolitical fault line.

The Risks Behind the AI Rally

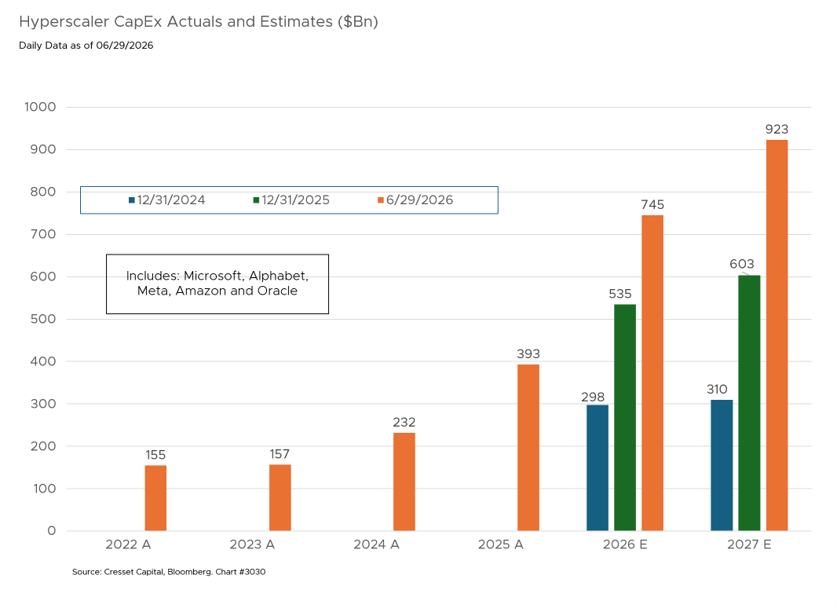

The capital expenditure picture warrants scrutiny as well. The five largest American hyperscalers — Alphabet, Amazon, Meta, Oracle and Microsoft — have collectively guided toward roughly $745 billion in combined capital expenditures for 2026, up approximately 89% from 2025. Amazon is targeting $200 billion, more than doubling its prior year outlay. Several of these firms are beginning to tap debt markets to fund ambitions that exceed their operating cash flows, transforming what were asset-light, high-margin businesses into capital-intensive enterprises. If AI monetization timelines slip, free cash flow will compress, and valuations will need to adjust. Analysts have begun to trim their valuation assumptions for Big Tech to account for uncertainties around the funding and timing of AI infrastructure returns, particularly given resurgent inflation and a hawkish Fed under Chair Kevin Warsh, who held rates at 3.50 to 3.75%.

The mid-June selloff, triggered by a single report that a South Korean chipmaker was slowing AI memory production combined with renewed fears about lower-cost Chinese AI model competition, produced broad-based declines across U.S. equity markets. That kind of hair trigger reactivity suggests markets are priced for a narrow path of continued execution, with limited tolerance for negative surprises.

Why This Cycle Looks Different from the Dot-Com Era

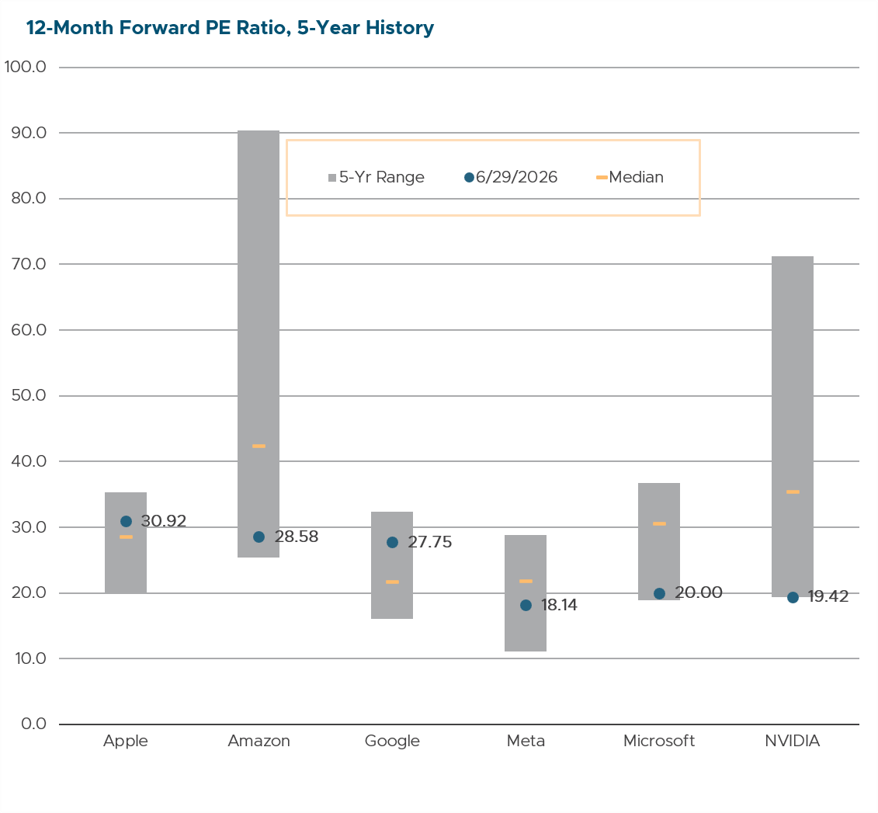

The AI boom differs fundamentally from the dot-com bubble because its leading companies are supported by robust profitability and cash generation. The Magnificent 7 trade at approximately 27 to 31 times forward earnings, compared with 52 to 66 times for the seven largest stocks at the peak of the dot-com era. Today’s AI leaders generate substantial free cash flow, maintain strong balance sheets, and fund most of their capital expenditures from operations rather than debt or equity issuance. The circular leveraged capacity-trading that doomed Global Crossing and its peers a generation ago has no analog in the current cycle. Alphabet and Meta, for instance, trade at or only modestly above the broader market multiple, a far cry from bubble-era excess.

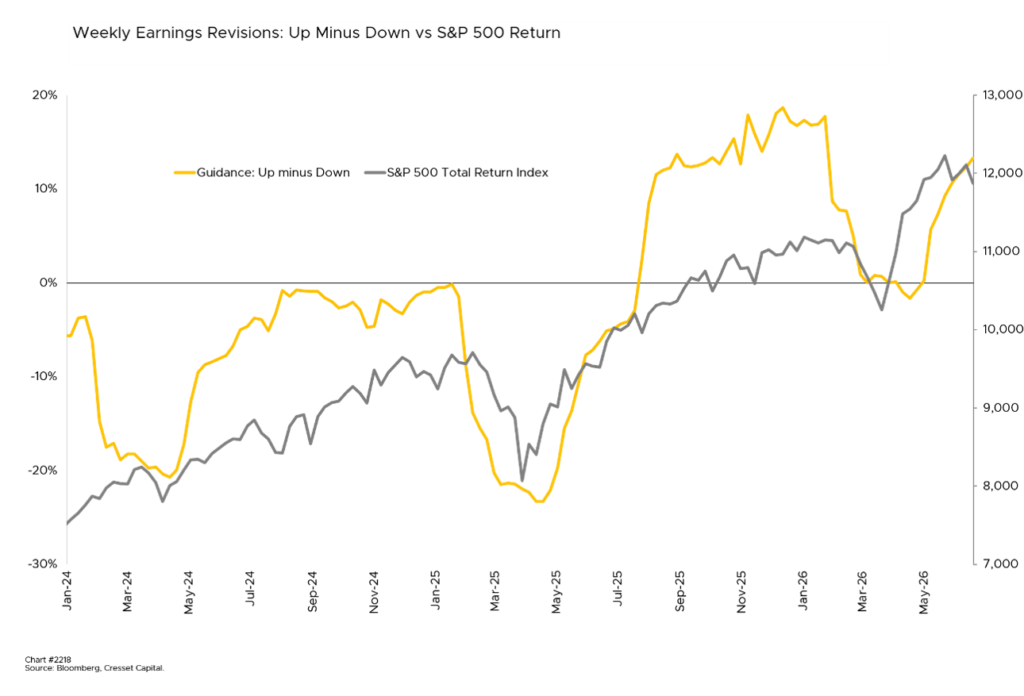

The earnings evidence is tangible and broadening. Analysts have raised their S&P 500 earnings growth forecast to approximately 23% for Q2 2026, with semiconductors and IT hardware accounting for more than half of the full-year upward earnings revisions and supporting higher year-end price targets for the index. Early returns on AI investment are no longer speculative: Meta’s advertising algorithms deliver a measurable revenue lift, Microsoft’s Copilot suite is deepening enterprise retention, and AWS is growing faster than consensus expected, driven by AI workloads moving from pilot to full deployment across corporate America.

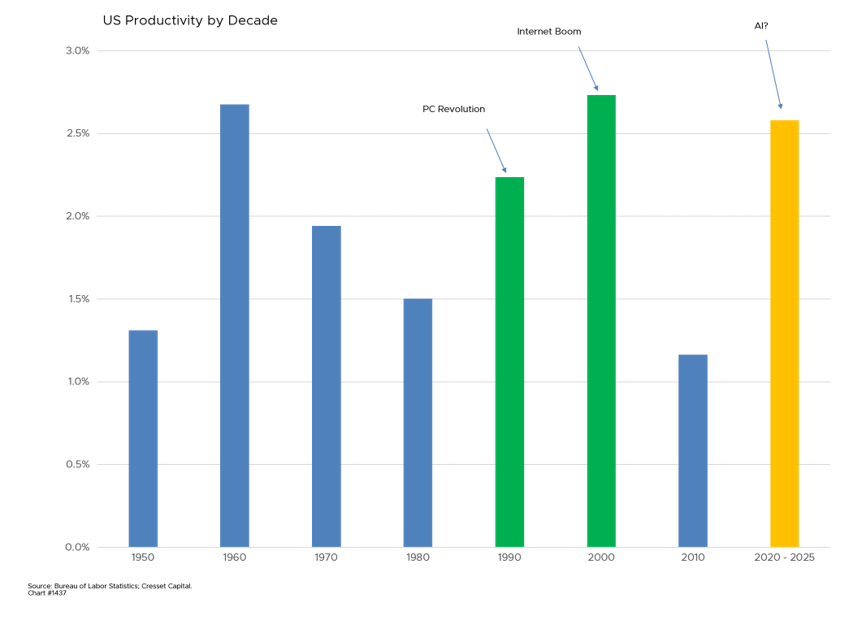

Productivity Could Be the Bigger Story

The broader productivity argument adds a dimension that pure valuation analysis tends to overlook. AI functions as a productivity shock, with compounding spillovers into labor efficiency, capital allocation, and energy demand. AI’s macroeconomic impact is still early to determine and uncertain in its distribution, but the direction toward higher output per unit of input is unquestionable. Historical precedent for transformative technology — railroads, electrification, and the internet — is that the eventual returns to patient investors exceeded the expectations of both optimists and skeptics at the cycle’s midpoint.

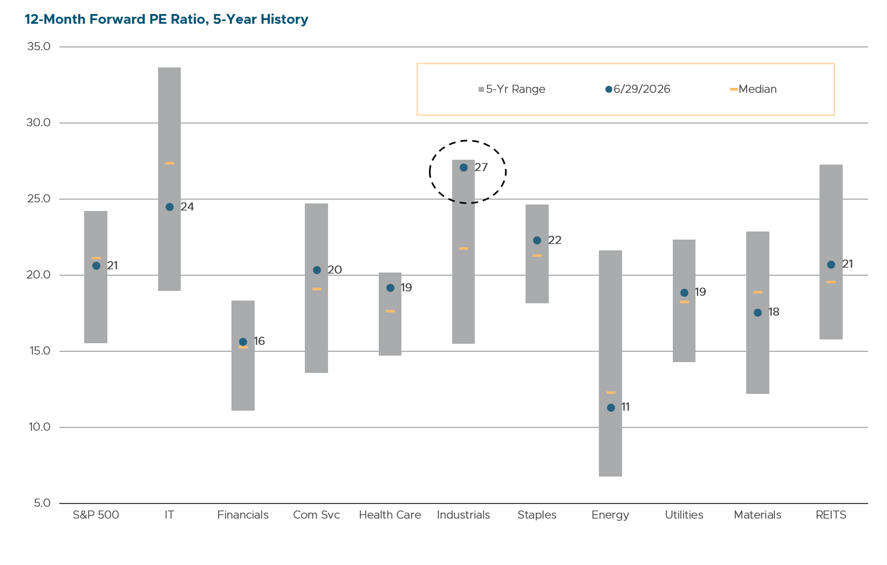

The investment opportunity is real, but unevenly distributed. The infrastructure layer, U.S. hyperscalers and leading semiconductor names, retains the most credible earnings support, although disciplined entry points matter more than they did a year ago. The Magnificent 7’s collective dominance is likely to give way to greater dispersion in 2026. Names with stretched valuations and capex programs that outrun operating cash flow carry meaningfully more risk than those that self-fund their AI strategies. Industrials, fueled by datacenter buildout beneficiaries, are overvalued relative to history. At 27 times next year’s earnings, industrials are trading at their highest valuation in at least five years and at a premium to every other economic sector.

Where Investors May Find the Best Opportunities

The more compelling risk-adjusted opportunity may lie in second-order beneficiaries that carry less valuation overhang and are earlier in their adoption curves. For taxable investors, private asset-based lending opportunities tied to AI-linked equipment leasing, particularly those capturing the 100% bonus depreciation provisions of the One Big Beautiful Bill Act, offer after-tax yield advantages that make the opportunity case even more compelling across the full portfolio.

The productivity gains AI is already delivering are real. The companies funding the buildout are profitable, cash-generative, and operationally credible. The cycle will produce volatility, and selectivity will determine who captures its returns. But sitting on the sidelines while one of the most significant technology transitions in decades unfolds carries its own form of risk, one that does not show up in standard risk models, but that compounds quietly against long-term wealth creation goals.

Bottom Line

AI carries genuine risks like elevated concentration, uncertain monetization timelines, geopolitical supply chain exposure, and a rate environment that is not forgiving of speculative excess. We take those risks seriously. Those risks, however, should shape how we invest, not whether we invest. We believe the fundamental case, grounded in real earnings, cash-funded infrastructure, and a productivity dynamic with historical precedent, is strong enough to clear the bar.

Success will depend on owning high-quality businesses at reasonable valuations, diversifying across the AI value chain beyond the headline names, and maintaining a time horizon long enough to weather the volatility this cycle will inevitably produce. We also believe investors should avoid leveraged long and short ETFs tied to the sector, as well as companies that depend on continuous access to capital markets to fund their AI ambitions. The opportunity is real, but selectivity rather than speculation will determine who captures it.