Key Observations

- Markets proved remarkably resilient despite war, an energy shock, and renewed inflation.

- AI-related investments continued to drive equity leadership and earnings growth.

- Treasury yields rose as investors demanded higher real returns, while credit markets remained healthy.

- The Federal Reserve shifted from anticipating rate cuts to signaling possible hikes.

- Energy markets normalized quickly following the Iran peace agreement, easing inflation pressures.

- Elevated valuations leave markets increasingly dependent on continued earnings growth.

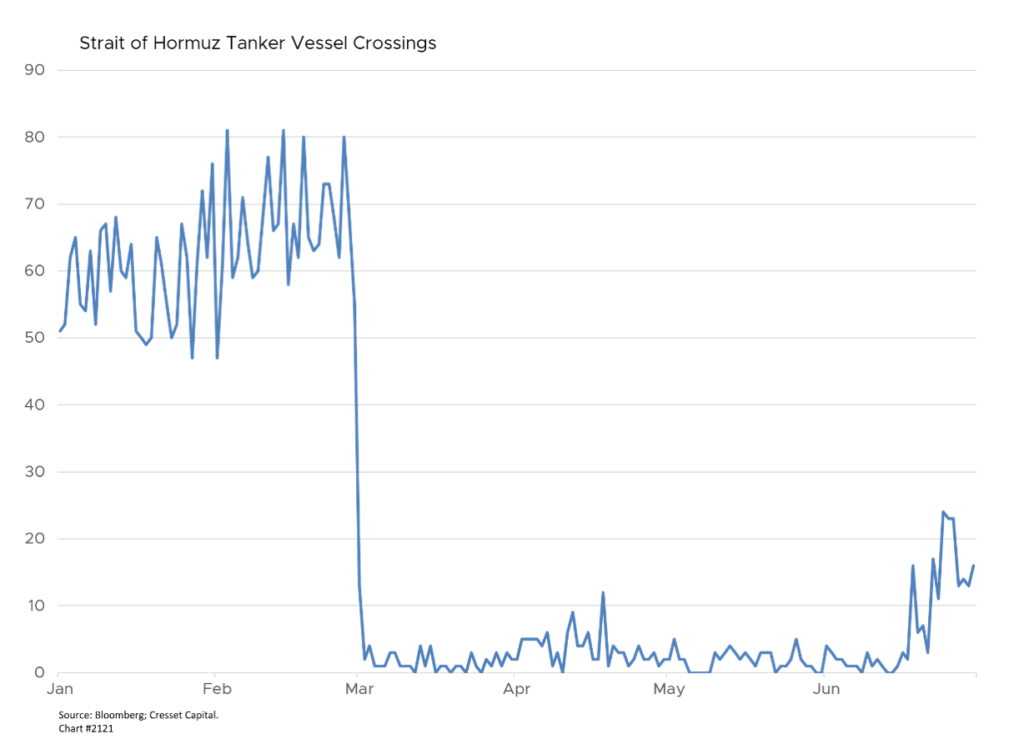

The first half of 2026 will be remembered for the U.S.-Iran war and the speed with which markets absorbed it. The conflict erupted in late February, and the near-total closure of the Strait of Hormuz, a chokepoint that normally carries roughly 13 million barrels of oil per day, delivered the most severe energy shock since the 1970s. Inflation pressures that central banks had spent years extinguishing came roaring back, supply chains buckled, and policymakers from Washington to Frankfurt recalibrated their outlooks in real time.

The turning point came on June 14, when the U.S. and Iran announced an interim peace deal to reopen the strait and set the stage for nuclear talks. President Trump signed the memorandum of understanding on June 17. The reopening was not seamless; Iran briefly re-closed the strait on June 20 in response to alleged ceasefire violations, but by quarter end, Saudi crude exports had recovered to roughly 90% of pre-war levels and tanker flows were normalizing quickly.

Equities Advance Despite War and Volatility

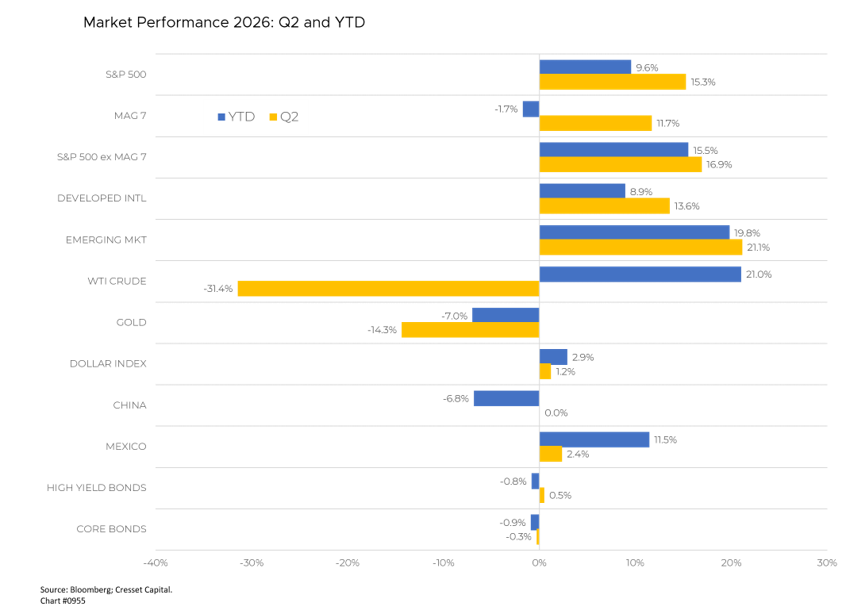

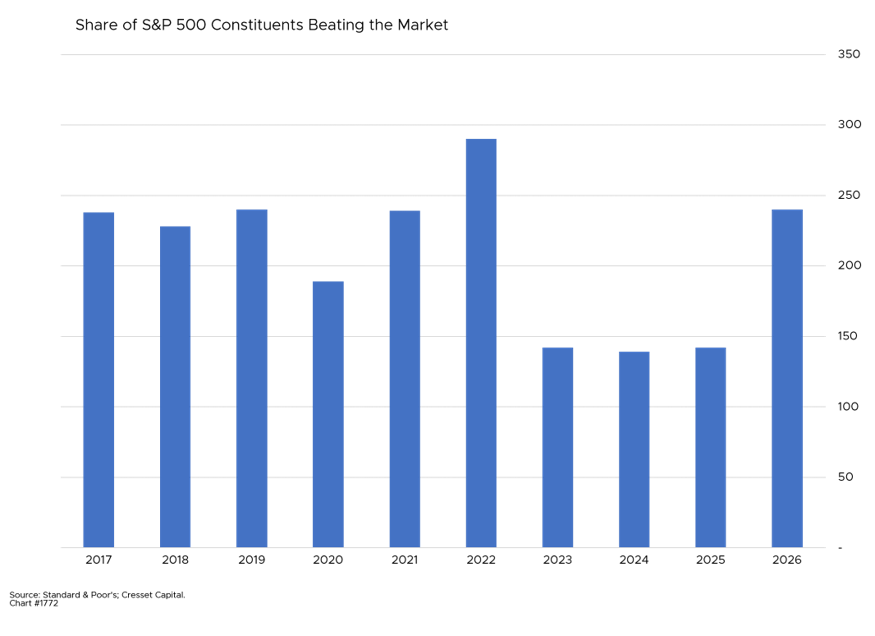

Against that turbulent backdrop, U.S. equities delivered a remarkable second quarter. The S&P 500 surged 14.4%, lifting its year-to-date total return to 10.5%. The Nasdaq Composite led the major benchmarks, surging 20.2% in the quarter and 13.0% for the year, powered by the artificial intelligence (AI) trade. The Dow, meanwhile, rose 12.8%, and Russell 2000 climbed 20.8%, leaving small caps nearly 22% higher year to date, a sign that market participation is broadening beyond mega-cap technology. For the first time in four years, nearly half of S&P 500 constituents are ahead of the index.

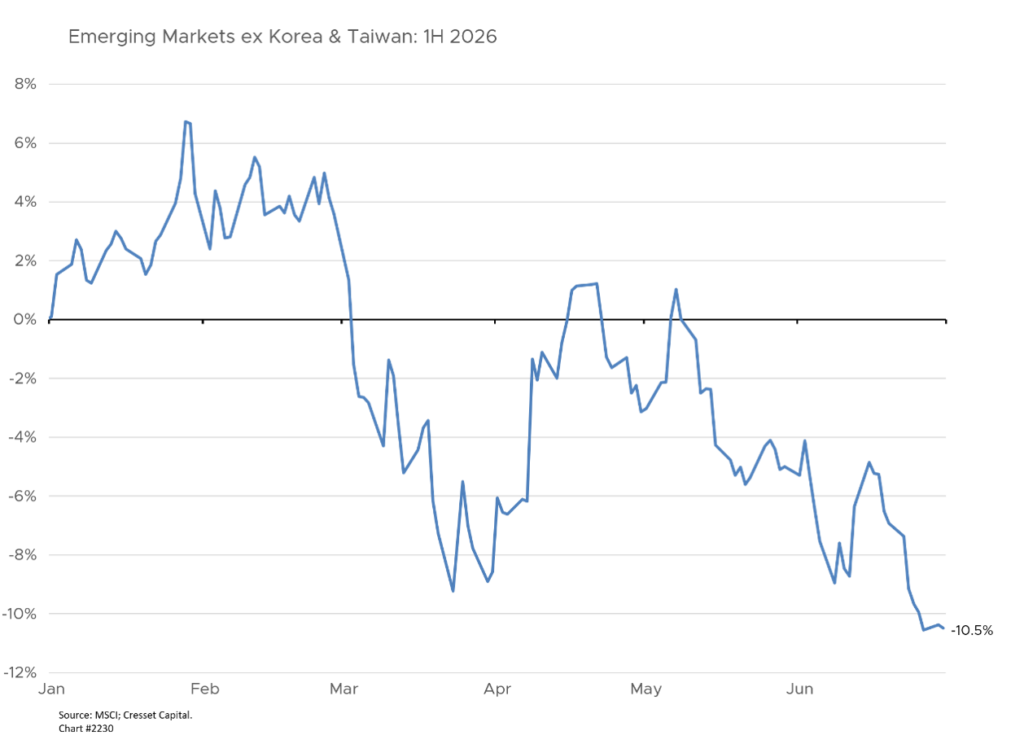

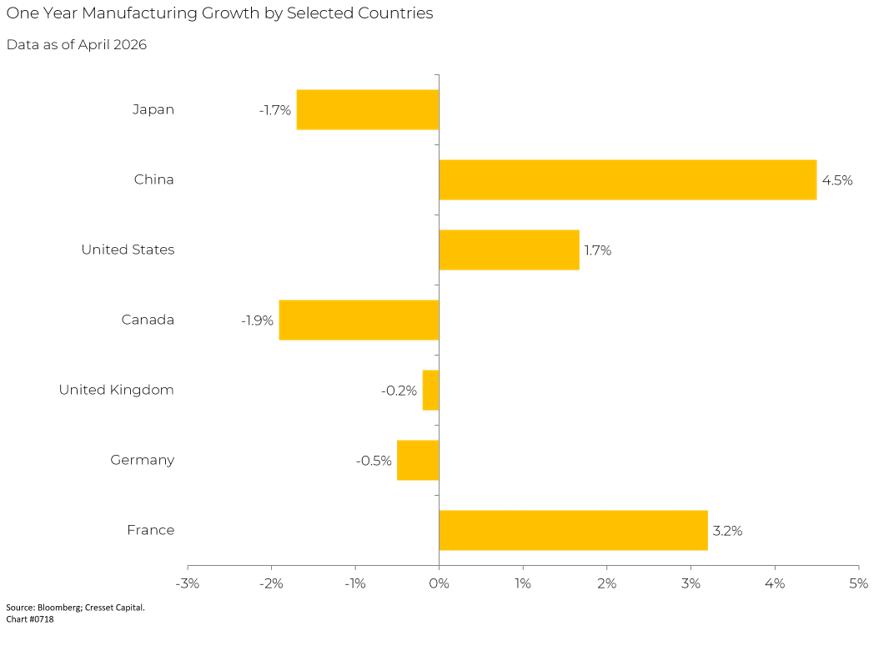

The AI investment supercycle was the primary driver of gains. Blockbuster results from semiconductors and data center companies, including a 17% one-day surge in chipmaker AMD kept enthusiasm elevated all quarter, while the peace deal added a mid-June relief rally on top. Emerging markets were an even more striking story. The MSCI Emerging Markets Index climbed 23%, its best quarter since June 2009, led by a handful of South Korean and Taiwanese technology chipmakers that were direct beneficiaries of AI infrastructure spending. While many believe the emerging market index “broke out” last quarter, excluding Korea and Taiwan, the EM is in correction territory, down more than 10% in the 1H 2026. Manufacturing gauges across six Asian economies crossed into expansion simultaneously for the first time since March.

Fixed Income Yields Grind Higher

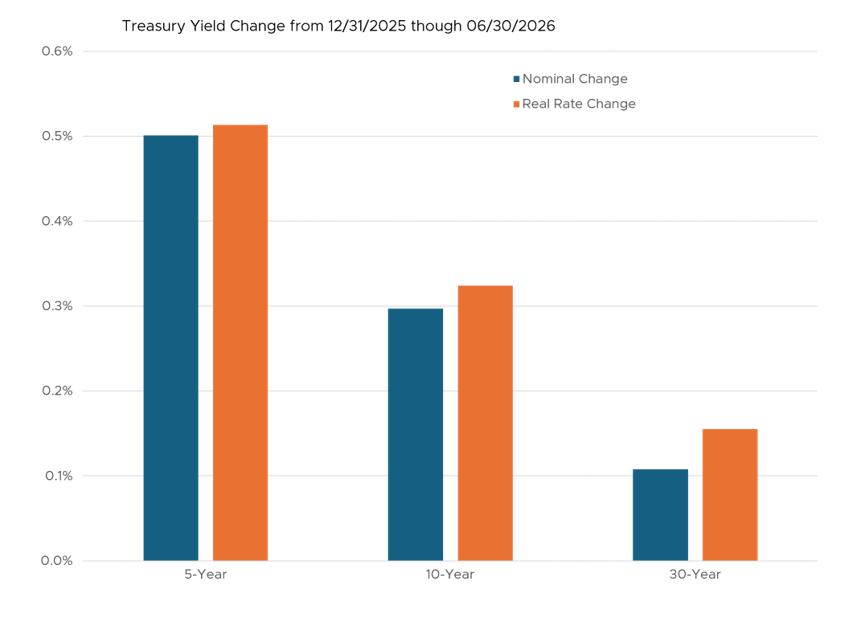

The bond market told a more cautionary tale as the benchmark Treasury yield rose steadily. The 10-year Treasury yield opened the year at 4.19%, ended the first quarter at 4.32% and finished June at 4.47%. Yields spiked in May as energy-driven inflation accelerated, with the 10-year briefly touching the high 4.60s and the 30-year reaching its highest level since 2007, before a softer-than-expected inflation reading sparked a late-June rally that rescued first-half performance. The rate rise, however, was entirely attributed to rising real rates, the “distrust premium” bond holders require on U.S. government debt. Credit conditions improved, with leveraged loans closing the gap on high yield as floating-rate paper found favor in a rising-rate environment.

Inflation and the Fed: The Pivot That Wasn’t

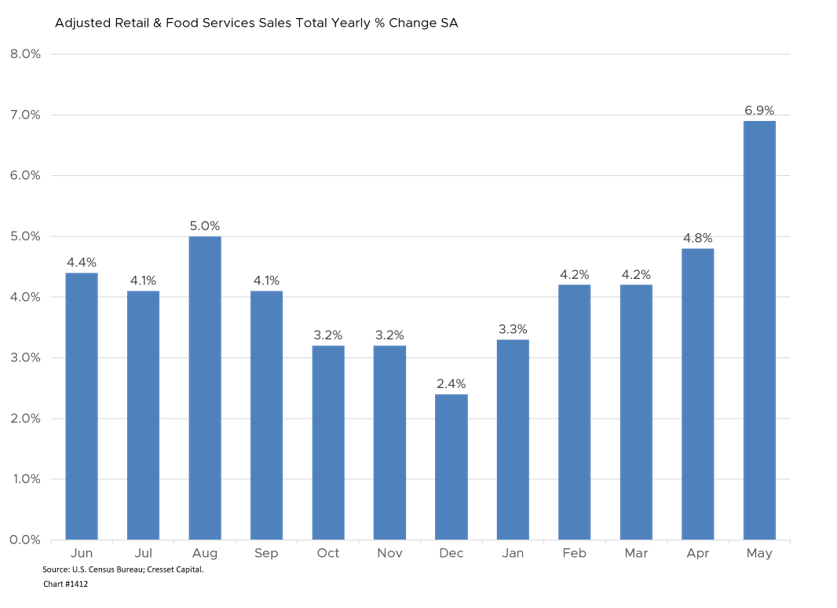

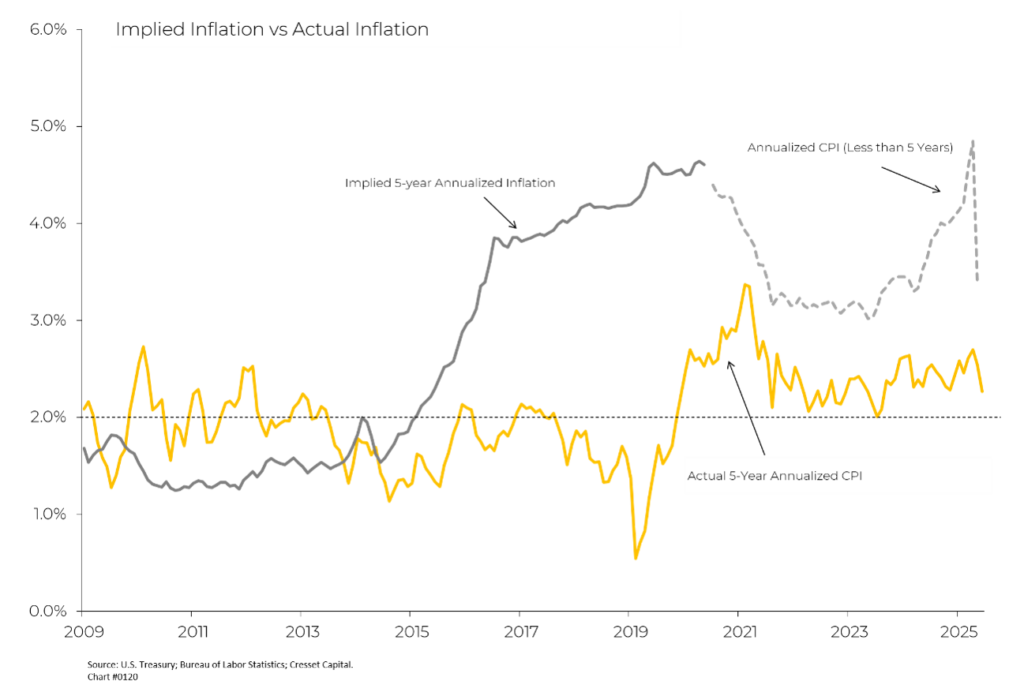

Inflation re-emerged as the central policy challenge of the year. CPI rose 3.8% year-over- year (YoY) in April, the fastest pace since 2023, and by May the headline PCE index reached 4.1% with core PCE at 3.4%. Consumers, remarkably, kept spending through the squeeze. Retail sales accelerated steadily through the first half of 2026, rising from 3.3% YoY in January to 4.2% in February and March, before picking up additional momentum in the spring. April posted 4.8% YoY growth and May surged to 6.9% YoY, its strongest reading of the period, suggesting robust consumer demand heading into the summer.

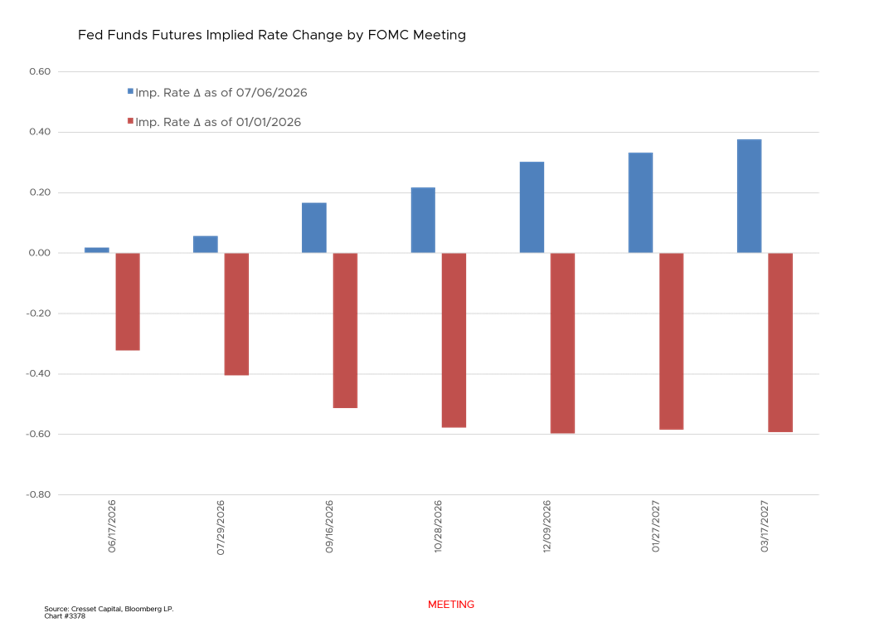

The Federal Reserve, under new Chair Kevin Warsh, entered the year biased toward cuts and spent the second quarter walking that guidance back. The June Federal Open Market Committee (FOMC) meeting held the policy rate at 3.50 to 3.75%, but the message was hawkish, with the dot plot split evenly between officials calling for hikes this year and those against. Nine of 18 officials now project at least one hike by year-end, up from none in March, and the median year-end rate projection has risen to 3.75%. The Fed Funds anticipated rate path has shifted from two cuts this year to more than one hike, representing a near one-percent turnaround.

Commodities Reset as Risk Appetite Returns

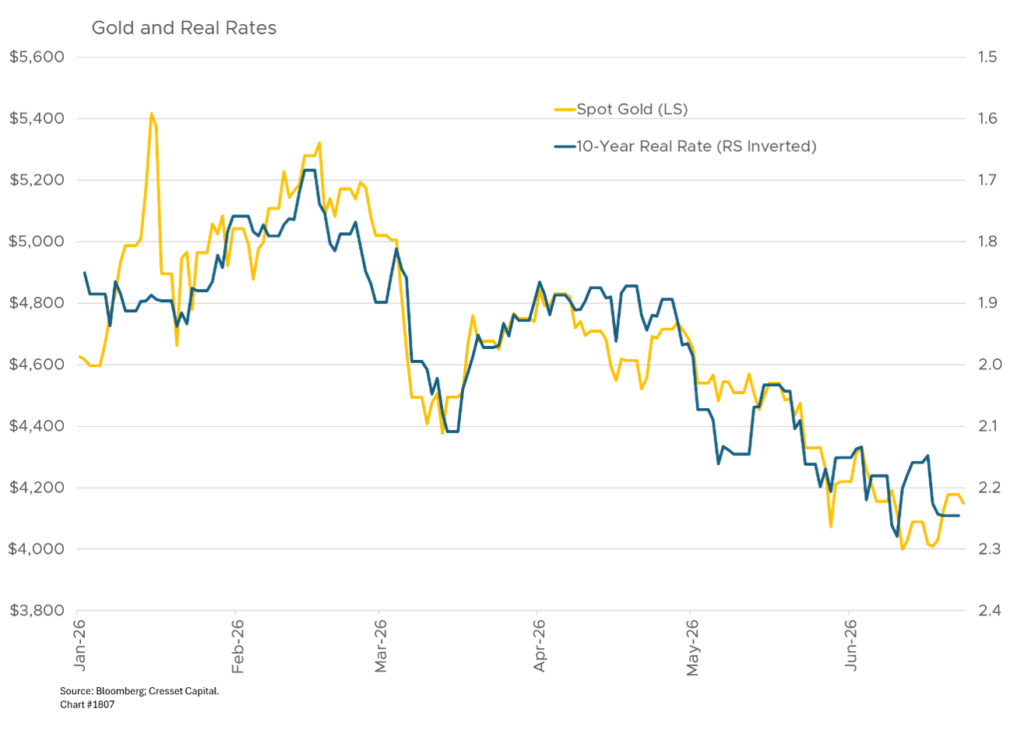

Oil was the most volatile asset of the quarter. WTI crude, which spiked as the Hormuz closure took hold, fell 30.6% in the second quarter as the peace deal and recovering Saudi exports replenished supply. At roughly $68 per barrel, crude sits near its lowest level since before the war began, though it remains up about 18% for the year. Gold gave back 15.8% in the quarter as safe-haven demand faded and now trades near $4,126 per ounce, down 4.8% year to date. While pundits argued gold’s decline was tied to a lack of central bank buying, our analysis reveals it had more to do with rising real rates, making financial assets incrementally more attractive than real assets. The dollar, meanwhile, gained 1.5%, supported by hawkish Fed repricing.

Economic Resilience Under Strain

The World Bank cut its global growth forecast to the slowest pace since 2020, citing a global energy shock. The European Central Bank raised rates in June for the first time in nearly three years even though German industrial output continued to slide. The U.S. labor market remained a bright spot through May, with payrolls advancing 172,000 and unemployment steady at 4.3%, though this morning’s June report showed a sharply weaker 57,000 gain, pulling market-implied odds of a July hike down to roughly 20% from 36% at quarter end.

The Second Half: Narrower Margins, Higher Stakes

Our base case for the remainder of 2026 is above-trend economic growth with above-target inflation. Growth will be slow enough to keep the Fed on hold through year-end with the first hike deferred to 2027. Inflation likely peaked in the second quarter and should moderate as energy effects fade, although we don’t expect annual inflation below 3% before well into next year. Growth should decelerate toward 2% as elevated energy costs bite consumers, and a fiscal deficit near 6.6% of GDP, swollen by war-related outlays, will keep supply pressure on longer maturities. We expect the 10-year yield to remain range-bound near current levels, with the front end of the curve outperforming.

Looking forward, we expect between 3-6% additional upside for the S&P 500 over the second half of the year, although given current valuations, earnings must carry the load from here. Analysts are anticipating about 14% earnings growth this year at valuations near 25 times, which leaves little room for disappointment as second-quarter results reveal the first full-quarter impact of elevated energy costs on corporate margins. The key risks are the durability of AI capital spending and the stability of the Iran peace deal. Meanwhile, positive earnings revisions are outpacing shortfalls, and CEO confidence remains steady against a backdrop of falling consumer confidence.

Bottom Line

The first half of 2026 tested markets with war, an energy shock, and the prospect of a tighter Fed, and equities passed with room to spare. The second half offers a narrower margin of safety. Valuations are full, earnings expectations are lofty, and the Fed’s next move is genuinely uncertain for the first time in years. We remain constructively positioned but disciplined, favoring quality companies with pricing power, broadening exposure beyond the mega caps, and emphasizing the front end of the yield curve while inflation finds its footing. The opportunity is real, but capturing it requires sound judgment.