For many founders and business owners, selling a business represents the culmination of decades of work, risk-taking, and reinvestment. It is both a liquidity event and a life transition. Yet without thoughtful planning, taxes can meaningfully erode the value business owners have worked so hard to build.

Implementing effective tax strategies for selling a business requires more than last‑minute structuring. It demands proactive, integrated planning that aligns your business, personal wealth, estate plan, and philanthropic vision well before a letter of intent is signed.

In this guide, we outline key considerations, structures, and strategies that can help owners preserve after‑tax proceeds and transition their wealth with intention.

Important note: This material is for general informational purposes only and is not legal or tax advice. Tax outcomes depend on individual facts, deal terms, and evolving law.

Understanding the Foundational Tax Implications of a Business Sale

What are capital gains, and how are they taxed in a business sale?

In many transactions, a major tax consequence of selling a business is capital gains tax. Capital gain generally reflects the difference between your tax basis in the business (adjusted over time) and the amount realized on the sale.

In practice, however, sale proceeds are often a blend of tax character, not purely capital gain. Depending on what is being sold (e.g., assets vs. stock), prior deductions, and deal structure, a portion of the economics may be treated as ordinary income (including depreciation or amortization recapture), compensation, or other categories.

Holding period matters. In general:

- Short‑term capital gains: (property held one year or less) are taxed at ordinary income tax rates.

- Long‑term capital gains: (property held more than one year) generally receive preferential federal rates.

- Additional surtaxes may apply, such as the Net Investment Income Tax.

Federal, state, and in some cases local taxes can apply. For founders in high‑tax states, the combined rate can be substantial, making advance tax planning central to preserving net proceeds.

Key Factors Influencing Your Tax Outcome

No two exits are exactly alike. Several structural elements shape both the timing and character of income, and therefore your ultimate tax liability.

1. The structure of the business

Your entity type—sole proprietorship, partnership, LLC, S corporation, or C corporation—directly impacts tax treatment.

- C corporations may face double taxation in an asset sale (tax at the corporate level and again at the shareholder level).

- Pass‑through entities (S corporations, partnerships, and many LLCs) generally allow gain and income items to flow directly to owners, often avoiding entity‑level income tax.

Equity compensation, preferred equity, and recapitalizations can further complicate outcomes by affecting how proceeds are allocated, taxed, and distributed across stakeholders.

2. Asset sale vs. stock sale

Buyers and sellers often have competing tax preferences.

- Stock sales are often more favorable for sellers, as gains are generally treated as capital gains.

- Asset sales are frequently preferred by buyers due to depreciation benefits and a step-up in basis, but it can create ordinary income components (including recapture) and may be less favorable for certain sellers.

In some situations, the legal form can be a stock sale while the parties jointly elect asset-sale tax treatment (e.g., a §338(h)(10) or §336(e) election). This can be a negotiated “middle ground,” but it is highly fact-specific and requires careful modeling and documentation.

Negotiating this structure is one of the most consequential decisions in a sale process.

3. The terms of the sale

Earnouts, rollover equity, seller financing, indemnities, and working capital adjustments can influence both timing and character of income. Payment timing may determine whether taxes are due immediately or spread across multiple years.

4. Other taxes and exposures that may apply

Additional considerations may include:

- State and local taxation: State sourcing rules vary widely by jurisdiction and by transaction structure (including differences between asset sales and equity sales). A sale can create unexpected multi‑state filing obligations and tax exposure, especially where the business operated or where owners are resident.

- Depreciation and amortization recapture: In an asset sale, previously claimed depreciation or amortization may be “recaptured” and taxed at higher ordinary income rates rather than capital gain rates, increasing the overall tax burden.

- Employment taxes: Certain payments (bonuses, option cash‑outs, retention payments, or amounts conditioned on continued employment) may be treated as wages subject to payroll taxes and withholding.

- Alternative Minimum Tax (AMT): Certain transactions—particularly those involving incentive stock options (ISOs) or significant timing differences—can trigger AMT exposure and unexpected tax liabilities.

- Estate and gift tax: A pending or completed sale can significantly increase estate size. Pre‑sale planning (such as gifting shares or using trusts) may reduce future transfer taxes, but timing, valuation, and implementation are critical.

Understanding these dynamics early can materially affect how you approach deal negotiations.

A Strategic Approach to Pre‑Transaction Tax Planning

The imperative of early planning

The most powerful strategies are typically implemented well before a sale. Once a deal is under contract or a sale becomes effectively binding, flexibility narrows significantly.

Proactive planning may include:

- Restructuring ownership interests: Adjusting capital structure or converting entity types (where appropriate) in advance can improve tax efficiency and align economic rights with desired outcomes.

- Implementing trusts or gifting strategies: Transferring shares to trusts or completing lifetime gifts prior to a liquidity event can remove future appreciation from the taxable estate, and may leverage valuation dynamics when executed with sufficient lead time and proper support.

- Optimizing basis: Increasing tax basis (through capital contributions, certain elections, or restructuring) can reduce taxable gain and improve flexibility in allocating proceeds.

- Evaluating Qualified Small Business Stock (QSBS) eligibility: Determining whether shares qualify can create significant federal tax benefits for eligible shareholders, but qualification requirements must be satisfied and maintained well before a transaction.

- Reviewing state residency planning: Establishing residency in a more tax‑favorable state prior to a sale may reduce state income tax exposure, though documentation and adequate lead time are essential.

In certain cases—particularly for founders of high‑growth companies—exit planning may also include pre‑IPO considerations, including lock‑ups, equity compensation strategy, and diversification planning around valuation inflection points.

Coordinating early with experienced tax, legal, and wealth advisors helps ensure that decisions support both immediate tax efficiency and long‑term financial objectives.

Comprehensive Tax Strategy and Planning Services

A thoughtful, integrated planning process often includes:

- Investment Advisory, including access to private investments

- Accounting and Reporting

- Financial Planning

- Insurance Analysis and Management

- Family Governance and Education

- Tax Advisory and Regulatory Compliance

- Philanthropic Planning

- Estate Planning

- Concierge Services

A coordinated advisory team with a fiduciary mindset can help align these moving parts, reducing complexity and helping ensure that tax strategy, investment planning, and wealth transfer decisions work together rather than in isolation.

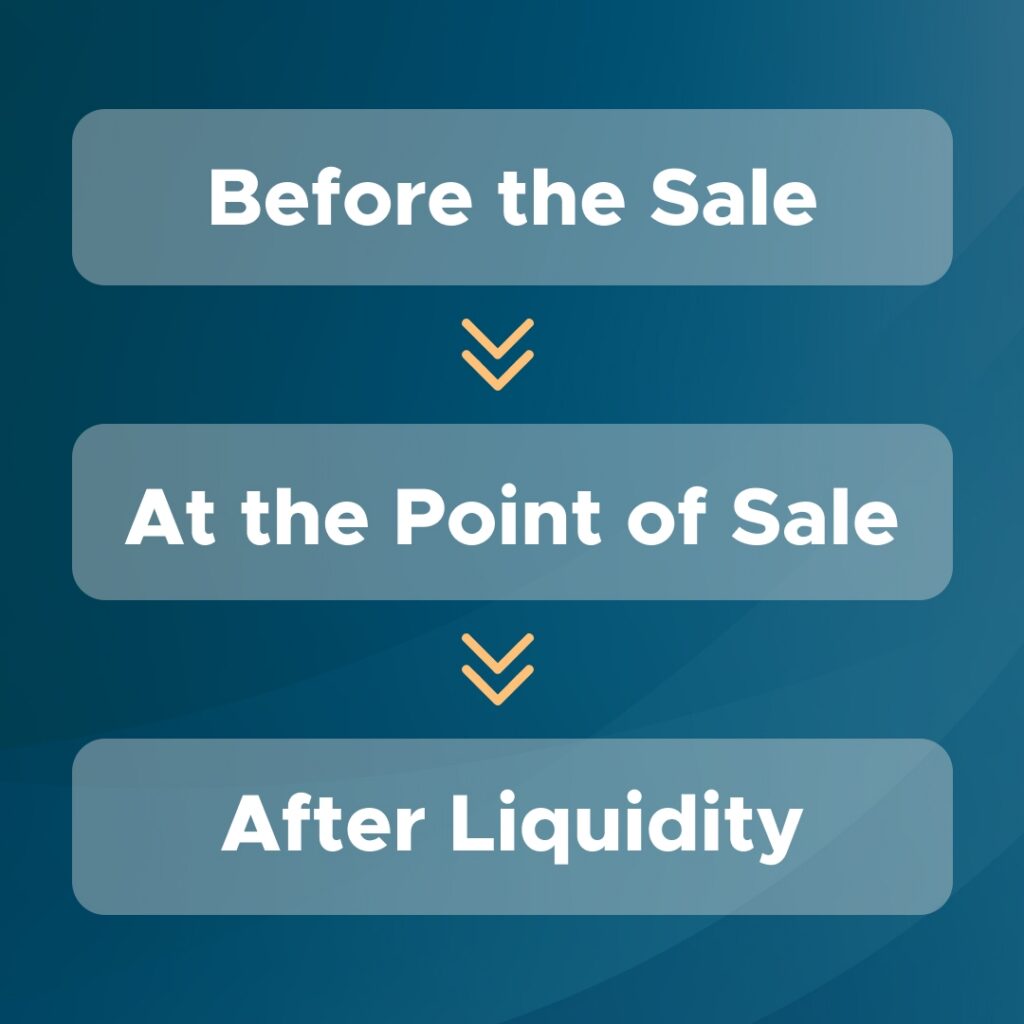

Optimize tax efficiency across the exit lifecycle

Thoughtful planning generally spans three stages: before the sale, at the point of sale, and after liquidity.

Pre‑Sale Structuring and Timing Strategies

For many founders, a business exit is preceded by years of holding a highly concentrated equity position. Whether in a privately held company or a late‑stage growth business, concentrated exposure can create both significant opportunity and substantial risk.

Pre‑transaction planning may include evaluating diversification strategies, liquidity pathways, and risk management techniques well before a formal sale process begins. Addressing concentrated exposure in advance can enhance flexibility and position owners to act strategically as market timing or buyer interest aligns.

Hold assets for more than one year (where feasible)

Long‑term holding periods can support preferential long‑term capital gain treatment where available and applicable.

Evaluate QSBS opportunities

If your company’s stock qualifies as QSBS and the shareholder meets applicable requirements, QSBS rules may allow an exclusion of some or all eligible gain, subject to limitations and technical rules. A QSBS review should occur early, as eligibility can be affected by entity type, asset thresholds, shareholder holding period, redemptions, and the company’s qualifying activities.

Consider gifting shares to family or trusts (well in advance)

Transferring shares prior to a sale may shift future appreciation to heirs and support broader estate planning objectives. Timing matters: gifts are typically most effective when completed before a transaction becomes effectively binding, and valuation support and documentation are essential.

Consider non‑grantor trust planning (where appropriate)

Properly structured non‑grantor trusts (including certain incomplete gift non‑grantor trust approaches, where suitable under applicable state law) may provide state tax planning opportunities and asset protection benefits. Outcomes depend heavily on trust design, administration, and the owner’s overall facts.

Use Charitable Remainder Trusts (CRTs) (generally pre‑transaction)

When funded with an appreciated business interest before a transaction becomes effectively binding, a Charitable Remainder Trust (including a CRUT or CRAT) can allow the trust to sell the contributed interest without immediate tax at the trust level, provide an income stream, and ultimately benefit charity, subject to the detailed requirements of IRC §664. Timing, valuation support, and documentation are critical to avoid assignment‑of‑income risk.

Execute pre‑transaction charitable planning

Donating appreciated shares prior to a sale can eliminate capital gains tax on the donated portion and generate a charitable deduction, subject to AGI limits, substantiation requirements, and timing considerations. This strategy is generally most effective when implemented before the sale becomes binding.

Strategies Applied at the Point of Sale

Offset gains with losses

Strategically harvesting capital losses can help offset gains recognized in the transaction year, subject to applicable limitations and ordering rules.

Structure the sale as an installment sale (seller financing)

Spreading payments over time may defer recognition of some gain and can potentially reduce exposure to higher marginal brackets in a single year. Installment structures require careful modeling of cash‑flow, credit risk, interest/imputed interest rules, and the character of income (including recapture items).

Use a 1031 exchange (real estate components in an asset deal)

If the transaction includes qualifying real property held for investment or business use, a like‑kind exchange may defer recognition of gain on the real estate portion, subject to strict timing, identification, and documentation requirements.

Consider an ESOP sale (where it fits the business goals)

An Employee Stock Ownership Plan may offer meaningful tax benefits and preserve company legacy, particularly for C corporations. ESOP transactions are complex and require specialized legal, valuation, and plan administration support.

Post‑Sale Investment and Philanthropic Strategies

Liquidity is not the end of planning, it is the beginning of a new chapter. After a sale, owners often shift from “building” wealth to “stewarding” it, with a focus on tax efficiency, governance, and long‑term legacy.

Invest in a Qualified Opportunity Fund (Opportunity Zones)

Reinvesting eligible gains into a Qualified Opportunity Fund may defer federal tax on those gains until the earlier of an inclusion event or December 31, 2026, subject to detailed timing and eligibility rules. Because the deferred gain is generally required to be recognized no later than 2026 under current rules, planning should include a cash-flow strategy for the resulting tax liability. Opportunity Zone strategies also require careful attention to liquidity needs, investment risks, and compliance requirements.

Charitable strategies after liquidity

After a sale, charitable vehicles (such as donor‑advised funds, private foundations, and—in some cases—CRTs funded with cash or marketable securities) can support philanthropic goals and may generate income tax deductions, subject to applicable limitations. These approaches generally do not change the tax character of gain already recognized on the sale.

Consider rollover equity (retain equity in the buyer)

Retaining equity in the acquiring company can align incentives and allow participation in future upside.

From a tax perspective, the result depends on how the rollover is structured. In some transactions, the equity component may qualify for partial or full tax deferral (for example, where the overall transaction qualifies for tax-deferred treatment under corporate reorganization principles or other rollover mechanics). In other cases, the rollover is simply a reinvestment and does not defer tax on the sale.

Because rollover treatment is highly fact-specific (including the form of consideration, any cash “boot,” and continuity requirements), it should be modeled early and papered carefully.

If structured as an asset sale: manage purchase price allocation

In asset deals, allocating the purchase price across asset categories can materially impact the mix of capital gain versus ordinary income (including recapture). Purchase price allocation is typically negotiated and reported consistently by buyer and seller, and it should be modeled carefully as part of deal economics.

Implement tax‑aware investing after liquidity

Post‑sale portfolio construction can often improve after‑tax outcomes through coordinated strategies such as asset location, tax‑loss harvesting (including direct indexing where appropriate), municipal bond analysis, disciplined rebalancing, and integrated cash‑flow planning.

The Distinct Advantage of Cresset’s Multi‑Family Office in Exit Planning

Fiduciary business sale advisory

Cresset serves as a strategic partner and advocate throughout the transaction, bringing objectivity to a process often driven by competing interests.

Coordinating your expert team

Exit planning typically involves investment bankers, attorneys, CPAs, and consultants. Cresset can act as a central quarterback, helping to ensure coordination, clarity, and alignment.

Democratization of the family office

Our mission is to expand access to sophisticated solutions historically reserved for ultra‑wealthy families, bringing institutional‑grade capabilities to successful entrepreneurs.

Wealth transfer planning and trust services

We integrate estate and trust planning into the transaction timeline to support both tax efficiency and legacy goals.

CFO services and reporting

From liquidity modeling to post‑sale balance sheet management, our CFO services can provide clarity and control.

Peer‑to‑peer learning and ecosystem

Through curated events and networks, we connect founders with peers who have navigated similar transitions, fostering insight beyond financial analysis.

Your Journey with Cresset: Navigating Four Pivotal Phases of Business Exit Planning

Phase 1. Proactive foundation building: setting the stage for future liquidity

Years before a transaction, we focus on tax optimization, estate integration, and business readiness.

Phase 2. Strategic negotiation and advocacy: optimizing the sale in motion

As a deal takes shape, we provide modeling, scenario analysis, and coordination with advisors to enhance after‑tax outcomes.

Phase 3. Seamless execution and finalization: securing your earned outcome

We support cash‑flow planning, trust funding, charitable implementation, and reinvestment strategy as liquidity is realized.

Phase 4. Enduring legacy and wealth stewardship: life beyond the transaction

Post‑sale, we help align your capital with purpose—supporting family governance, philanthropy, and tax‑aware investing for generations.

Conclusion

Selling a business is far more than a financial transaction—it is a defining life event. The difference between a reactive approach and a comprehensive, proactive strategy can be measured in potentially millions of dollars of after‑tax value, as well as in the clarity and confidence you carry into your next chapter.

A successful exit requires integrated planning across tax, estate, investment, and legacy considerations. At Cresset, our multi‑family office model delivers coordinated and deeply personalized guidance, helping founders and business owners protect what they have built and steward it with intention.

Through our dedicated business exit planning services, we work alongside entrepreneurs at every stage of the journey, from early strategic preparation to transaction execution and post‑liquidity wealth stewardship. By bringing together fiduciary advice, tax‑aware investment management, estate planning integration, and family office capabilities, we help ensure that the outcome of your exit reflects not only the value of your business, but the vision you have for what comes next.